Clearly investors (and I, too) think that staffing firms can provide value beyond surge capacity during 'Rona. Labor issues in hospitals go beyond the Covid surges.

There are longstanding structural issues within healthcare staffing that new startups who raised recently like Incredible, Nomad, and Vivian Health (listen, I'm sorry if I didn't mention you here - I'm only human!!) are aiming to fix, namely:

These structural issues provide an interesting value prop for investors. Beyond the operating needs, here are some reasons why staffing firms are so enticing from a financial standpoint:

- They're scalable - public profit margins swelled despite unprecedented growth

- Staffing is highly fragmented and investors can deploy the roll-up playbook similarly to how Envision or USAP cornered local physician markets and jacked up prices in certain cases (I'm not saying that's what's gonna happen here, I'm just saying it's economically possible right?)

- Unlike services companies, staffing agencies have pricing power and there is little to no state regulation on pricing yet (just however much the hospital is willing to pay), something that the AHA has bemoaned

- Healthcare hiring was unaffected by the last recession. Volumes are still recovering from 2019 levels, and healthcare is generally resilient as seen by the September jobs report.

As a result, we've seen a ton of investment activity from private equity players and VC-backed startups. Staffing startups have raised at least $700 million according to Business Insider (valuations noted where available):

- Trusted Health raised $149 million

- IntelyCare raised $115 million at a $1.1B valuation

- ConnectRN raised $76 million

- Vivian Health raised $60 million, which apparently filled 15% of all travel nursing positions in 2021!!

- Nomad raised $105 million

- Incredible Health raised at a $1.65B valuation

- Clipboard Health raised $30 million at a $1.3B valuation

Along with startup activity, here are some other recent PE-backed investments (paywall - PE Hub) in the staffing space:

One Equity Partners acquired Prime Time Healthcare (consolidator, nursing and clinicians)

- HIG Capital acquired Barton & Associates (temporary staffing services)

- HCAP Partners invested in FleetNurse

- PE-backed Ingenovis Health acquired VISTA

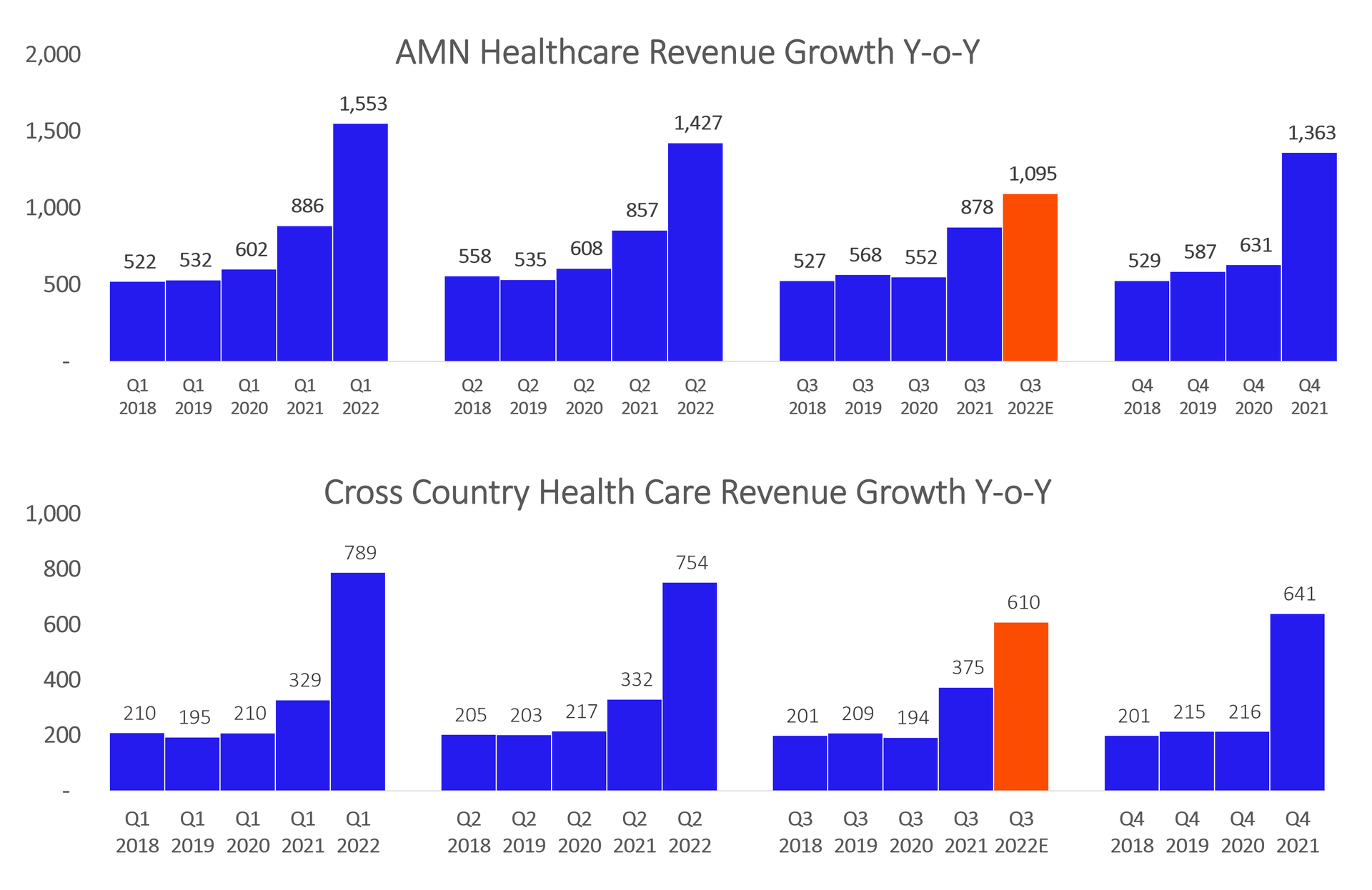

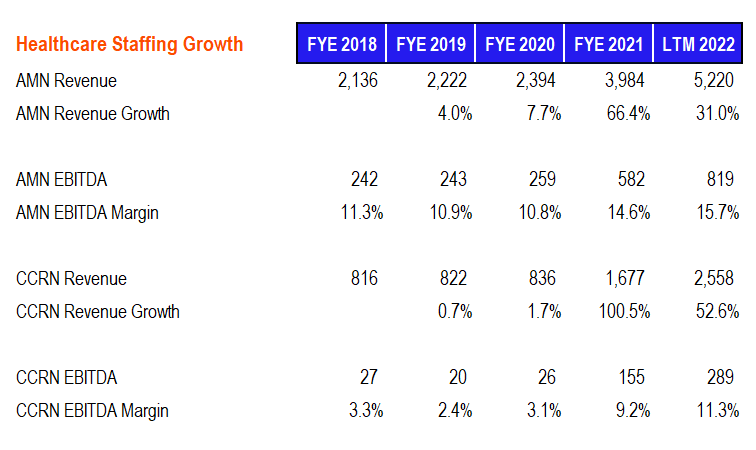

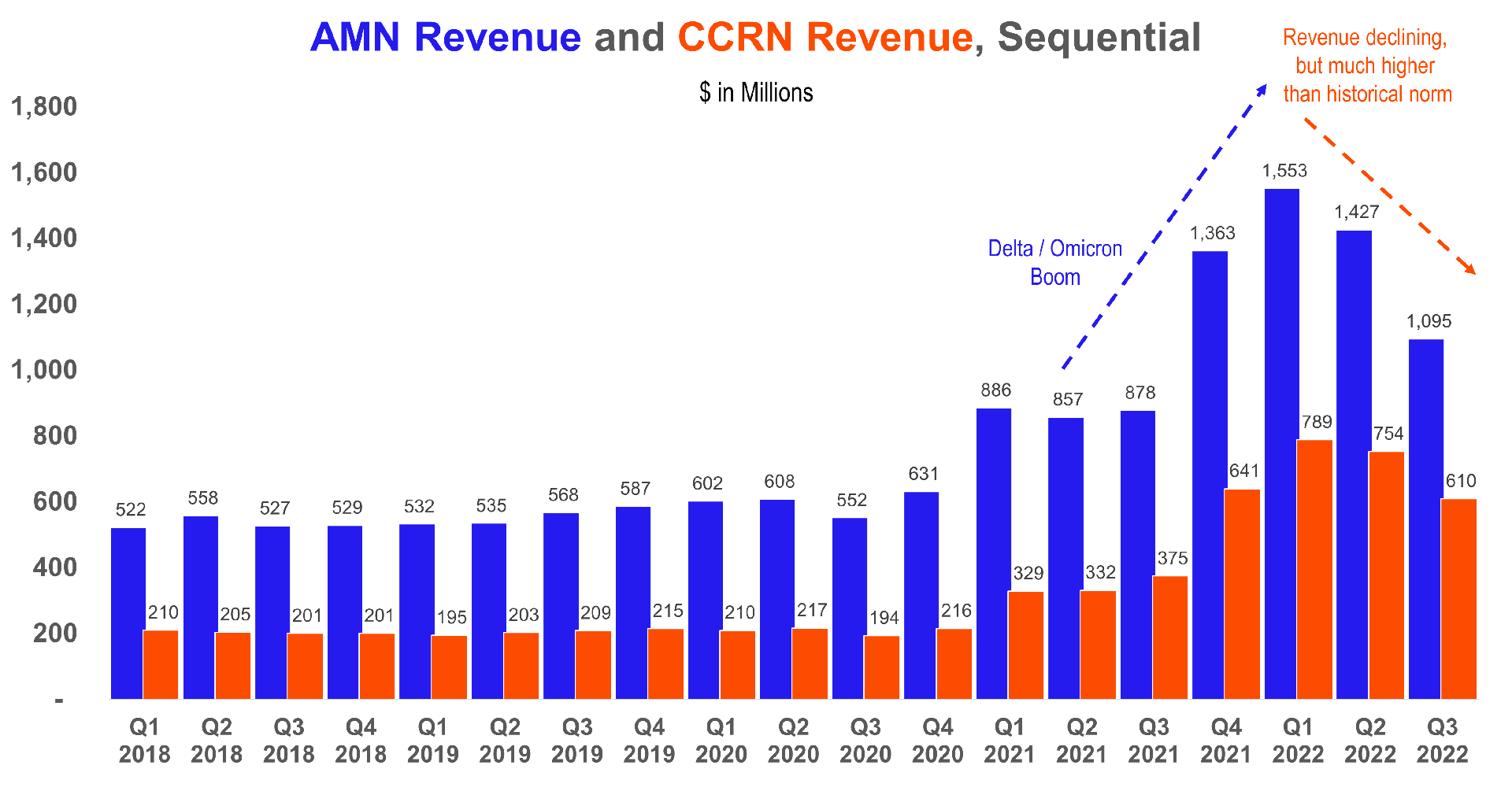

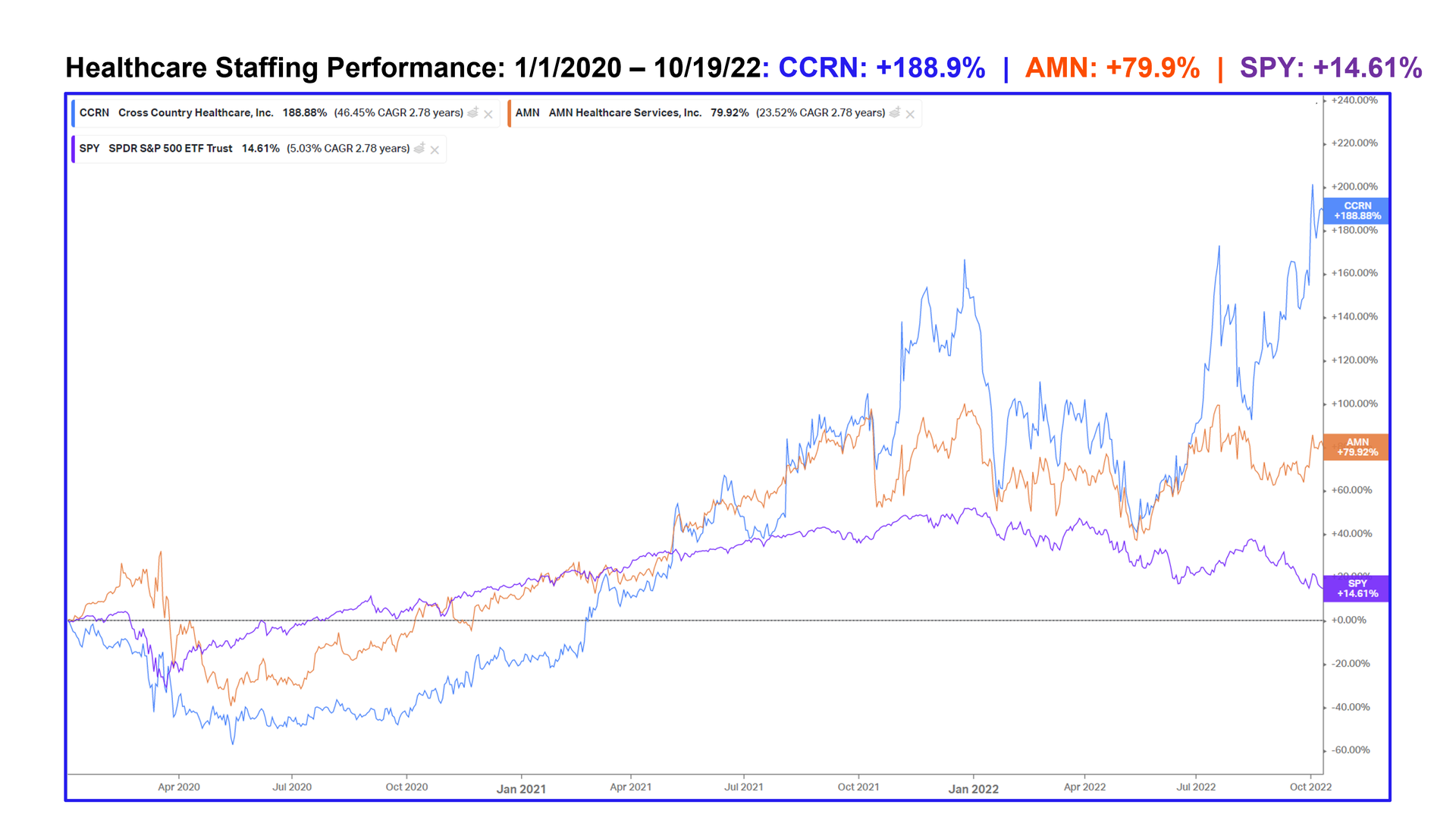

So as you can see, these companies have amassed pretty big valuations and hefty investments in a pretty short amount of time. AMN Healthcare's latest enterprise value sat at around $5.5B (1.3x NTM revenues; 8.6x NTM EBITDA) while CCRN's totaled $1.5B (0.7x NTM revenues; 7.3x NTM EBITDA).

Conclusion

Even though travel staffing effects decreased, staffing agencies are a much larger player in 2022 and will continue to be moving forward.

Healthcare staffing companies are fragmented and will continue to grow in prevalence as seen by the massive raises in 2022. But at the same time - how big is the TAM pie here?

Clinician shortages are not going anywhere, and staffing agencies are the best positioned to take advantage of that crunch.

There's a real opportunity for these firms to work with hospitals and optimize staffing during a time of real need for hospitals as labor is the number one issue at most provider organizations.

I'm willing to bet we'll see some price gouging happen among bad actors in this space, and regulations are bound to come.

The biggest factor in my mind: how will staffing firms ultimately affect patient care, if at all?

Thanks for reading - this was a fun one! Hit me with any and all thoughts related to healthcare staffing and the dynamics at play by replying to this e-mail or on Twitter.

No comments