Here's the most telling part to me…Bright's executive team has a ton of experience in health insurance. So what went wrong here? Here are some guesses:

Growth too fast, too soon: Bright struggled to get its operations under control amid too many market expansions. While the firm promised its investors scale and growth into new markets through acquiring members and providers, the firm couldn't manage that massive growth with existing infrastructure. As a result, it couldn't appropriately capture risk adjustment for its members.

Dumb administrative expenses: Similarly to the first bullet, Bright spent a ton on marketing and selling expenses during the special open enrollment period in 2021 and throughout its growth campaigns. And let's not talk about the exorbitant executive compensation package Bright decided to pay itself out despite its horrid operating results.

MA and Employer/Commercial market struggles: The individual market contains the lowest barrier to entry and is primarily where we saw Bright and Oscar compete with incumbents. Unfortunately, like I mentioned before, this market is hard to predict from a risk perspective. Bright didn't have the network to compete with incumbents in more lucrative, stickier markets. Bright's decision to compete on price in the IFP markets also led to more narrow networks, less patient choice, worse consumer experience, and higher out of network costs for its business.

Geographic Concentration: Bright held a large market presence in Florida and that concentration risk led to outsized medical costs, which were especially pronounced during the height of the pandemic with regional surges. Incumbents were more insulated from surges given their larger membership bases across diverse geographies and also offset by deferred care from elective procedures.

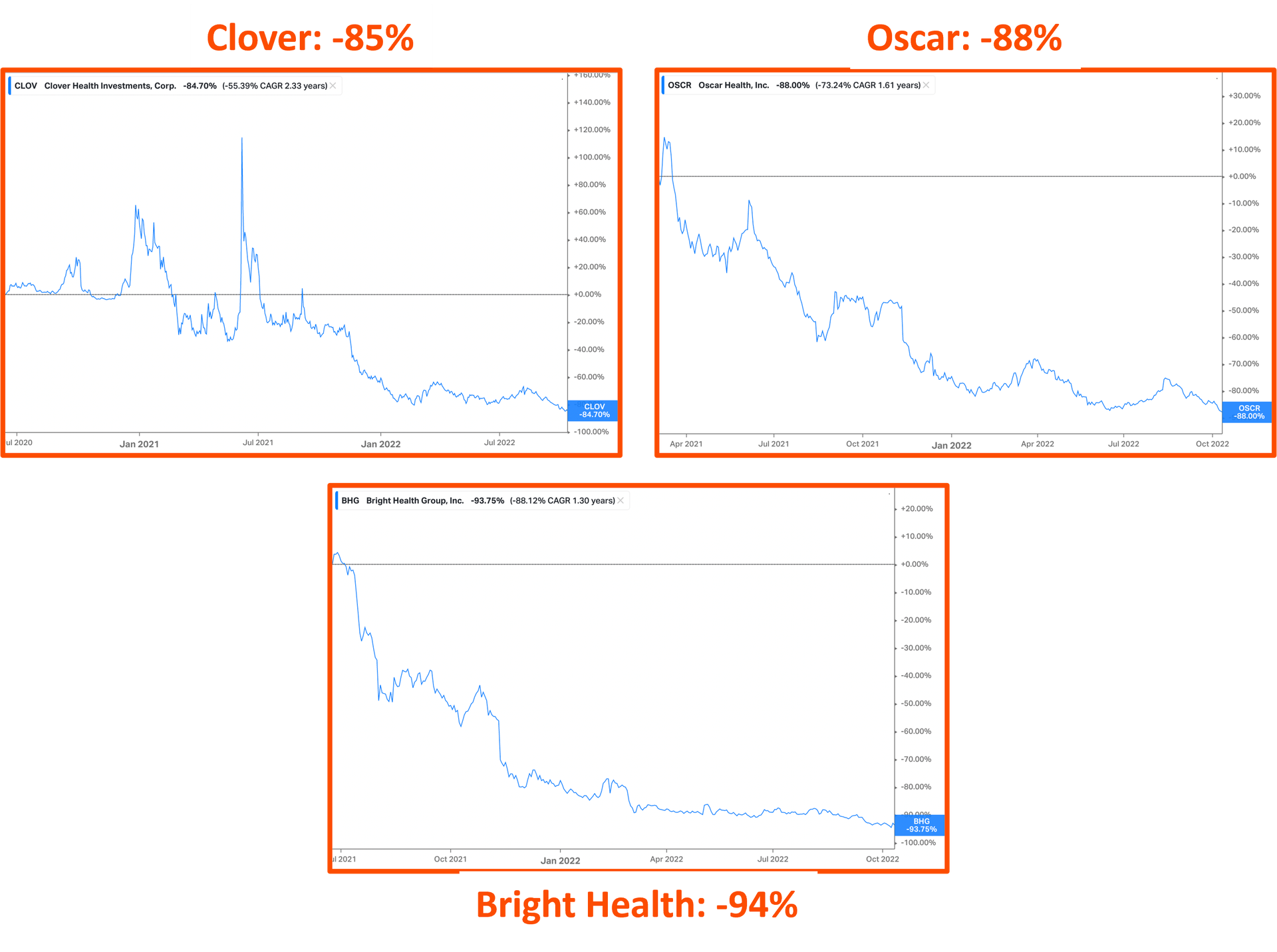

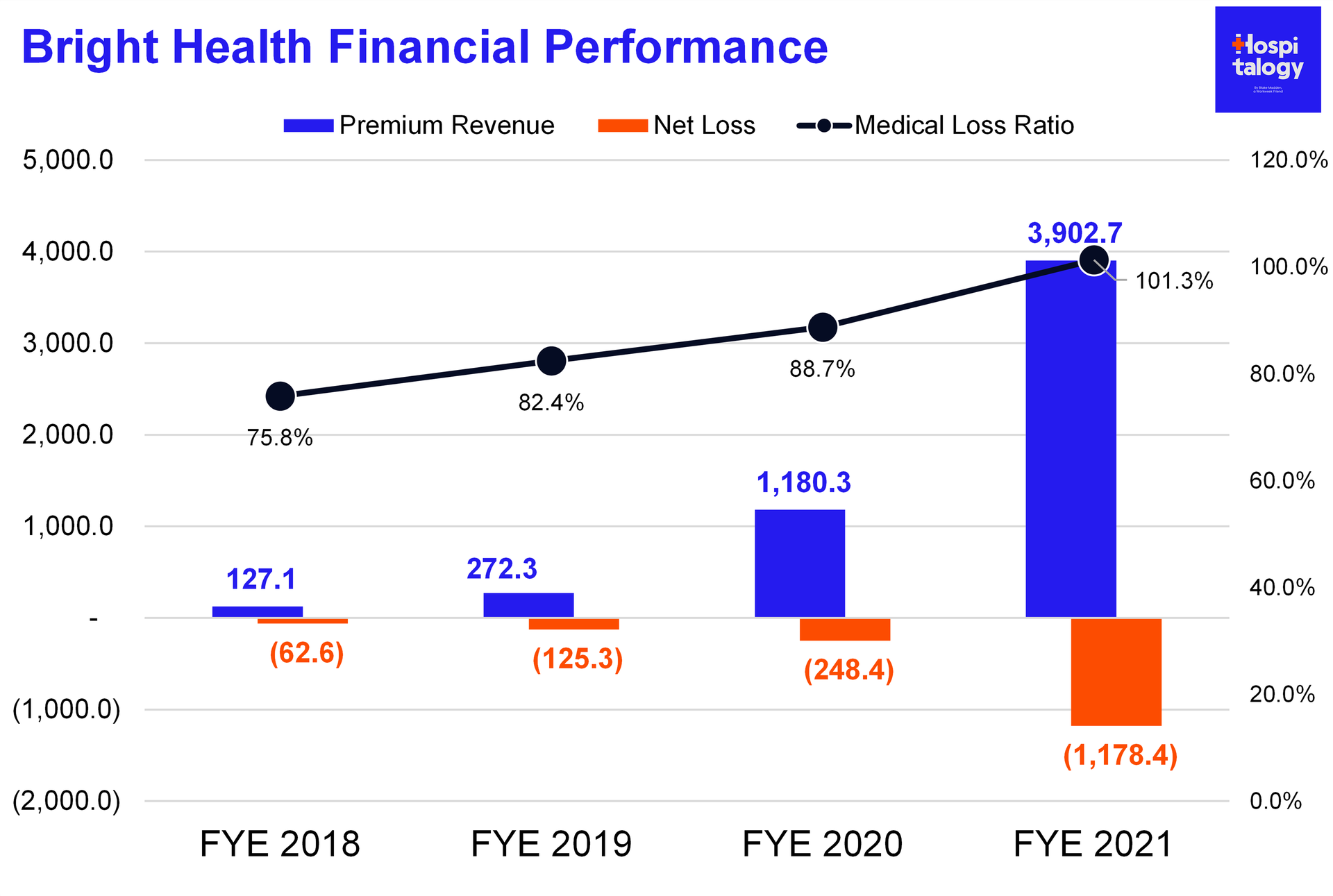

As a result of its poor business decisions, Bright Health stock saw a washout from $11B+ to under $1B. Whooooosh. What's that? The sound of investment dollars getting flushed out of Bright Health (mine included).

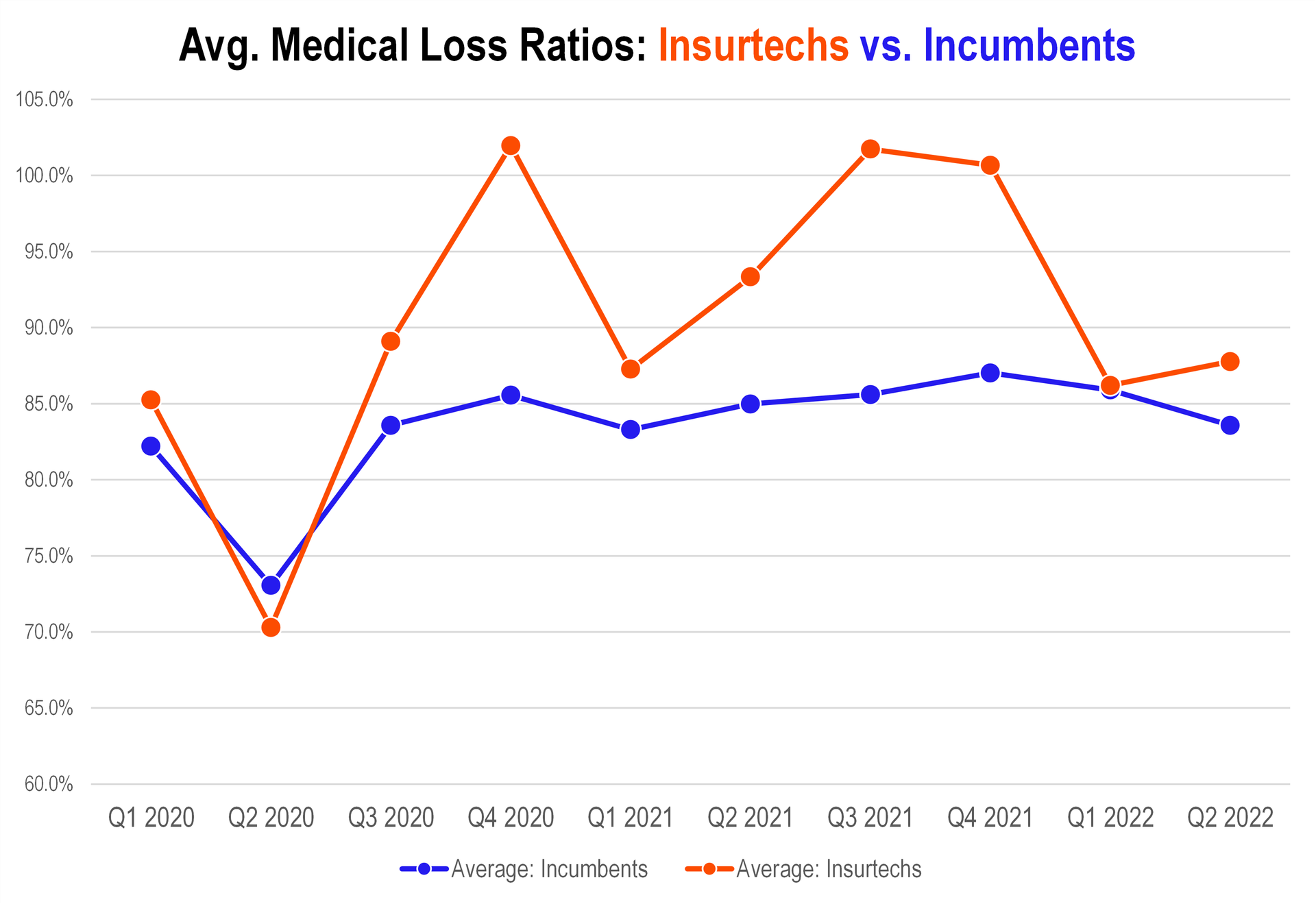

Mismatch between Insurtech investments and outcomes.

The healthcare - and health insurance - experience needs to improve. But so far, VC-backed upstarts have failed to make a dent because the odds are stacked toward incumbent insurance giants.

This write-up won't stop investment dollars from flowing into healthcare insurtechs. The TAM is too enticing, and the industry needs obvious improvement. A.I., data, and other tech-enabled offerings will eventually find ways to force incumbents to evolve their business models in order to stave off their VC-backed competitors.

That being said, any belief that a snazzy looking UI with some added tech haphazardly attached to an insurance product can outcompete the titans of an industry filled with execs who have been in the game for decades is naive at best.

For now, creating a tech-enabled operation in health insurance from scratch is extremely difficult. Not impossible, but hard. And investors need to be realistic about returns in this space. There's a fundamental mismatch between expected returns in healthcare insurtechs (including historical valuations) and insurance regulations that mandate fixed margins and low-single digit net income.

P.S. - plz stop valuing insurance & risk-based businesses on multiples of revenue.

Final Thoughts.

I'm not saying it's impossible for Bright, Clover, Oscar, Devoted, Alignment, and others to break up the health insurance industrial complex with a ton of regulatory capture, but maybe there's a better option.

Instead of focusing on building large-scale insurance products to compete directly with incumbents, perhaps are better paths to success for new entrants:

- Dare I say it…work with the United's and Humana's of the world to help them transform patient experience and create a better product from the inside out. Understand key, nuanced pain points for these organizations and build them.

- Build offerings that make them more $$$ (ahem…Signify and in-home evaluations)

- Develop smaller-scale MA plans (like Alignment) that focus on member experience, a key factor in quality payouts (MA star ratings).

- Finally, another interesting, potentially-emerging option for insurance startups…partner with health systems and providers to help them transition to risk-based models (physician enablement, ACOs, MA plans). Create new insurance products that will ultimately compete with insurers in the employer and self-insured markets. Easier said than done, I know lol.

Share your thoughts, half-baked theories, opinions, or disagreements with me and I might post a follow-up as to why the insurtechs have sucked so much over the past year!

No comments