Happy Thursday, We saw a big drop off in managed care names as a result of some utilization commentary from UnitedHealth Group, so I figured it was worth discussing current volume trends, and where things might be headed! |

Was this email forwarded to you? |

|

|

Healthcare is complicated. We all know it. And with the explosion and adoption of new value-based care programs, care coordination and team-based care is more important - but also more complex - than ever before. Dock Health makes chronic disease management seamless across all dimensions: - Better care coordination across PCPs, specialists, and caregivers;

- Proactive task management to facilitate patient engagement (reminders, medication adherence, and education);

- More efficient workflows for care teams dealing with multiple touchpoints; and

- More effective billing, auditing and documentation

Care delivery organizations face more hurdles than ever. Don't overcomplicate this decision too. Choose simple. Choose Dock Health, and their thoughtful, client-focused team, today. |

|

|

UTILIZATION TREND ANALYSIS |

- Shares in managed care players plummeted this week.

- The drop related to UnitedHealth Group's CFO commentary on higher than expected outpatient volumes in Q2.

- Survey data indicates that outpatient surgery demand is surging.

- Volume is returning to healthcare as labor shortages alleviate and unlock OR capacity.

- We are seeing a long-term, secular trend play out in the shift to outpatient services.

|

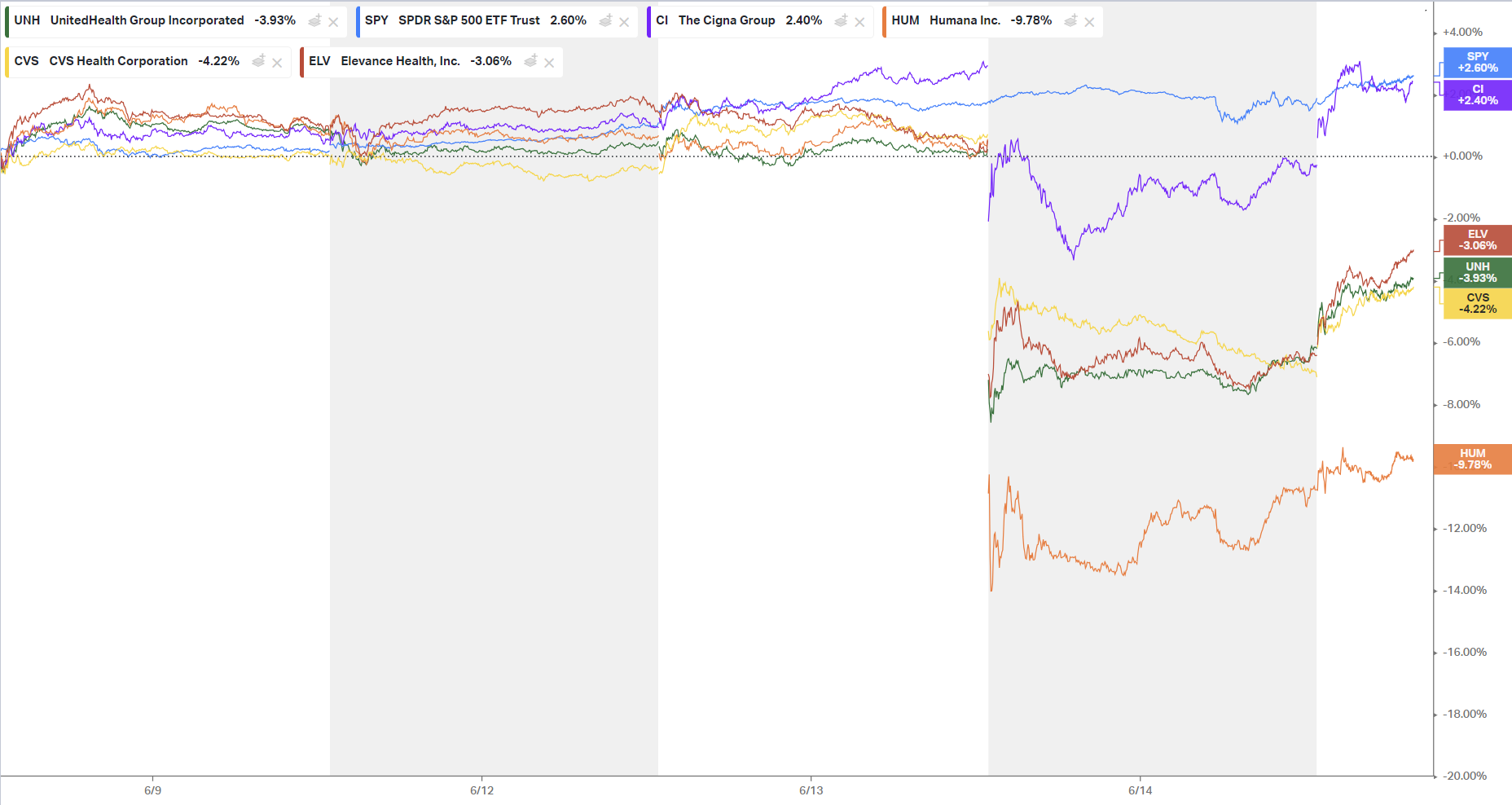

A Volume Paradigm Shift, or Small Blip? A friend texted me earlier this week, asking "dude - look at what's going on in managed care right now in the markets." I took a quick peek. Managed care names were selling off in droves, with Humana down as much as 12%, and since then recovering a bit: |

Originally I thought the selloff was related to this analysis discussing Medicare Advantage overpayments, but no - folks on Twitter quickly pointed me to the commentary at a conference made by UnitedHealth Group's CFO discussing abnormal, heightened volume demand on the horizon: - "…we saw higher levels inpatient continued pretty controlled. In fact, probably below 2022 levels…" = inpatient volumes are growing, but as expected.

- "but outpatient levels have continued to be an area that, we've really focused on most and where we see it really occurring." = UHG worried about outpatient utilization.

- So much so, that they're likely to see a spike in medical spend: "…you would expect Q2 medical care ratio to be somewhere in the in the zone of probably the upper bound or moderately above the upper bound of our full-year outlook…I would expect that the full-year would probably settle in the upper half of the existing range that we set up."

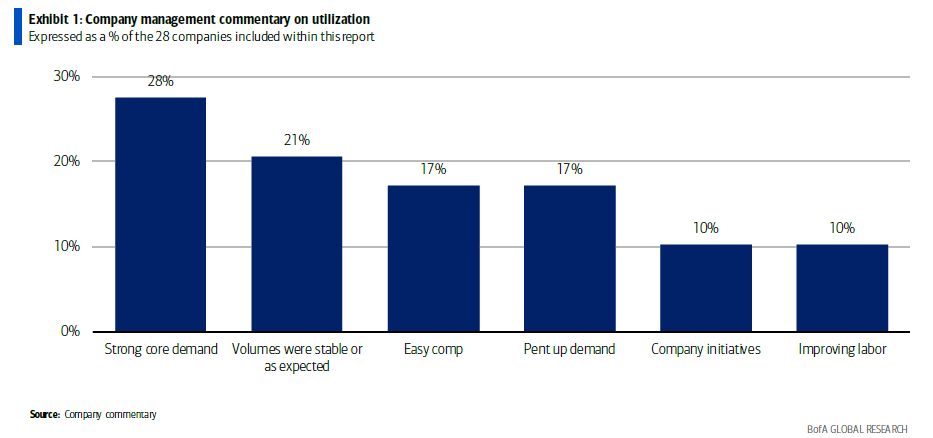

The commentary aligns with findings from major healthcare analyst publications and surveys on utilization - TD Cowen's nonprofit health system survey indicated continued, significant volume growth for hospitals in the second quarter. And so this news, perhaps combined with some investor sector rotation, resulted in a selloff of managed care names scared of a resurgence in volume (and perhaps some sector rotation). So - what's the bigger trend at play here? Utilization is coming back, and the outpatient book of business is surging for provider organizations. Is the volume trend sustainable? The question at hand now is whether the growth in outpatient volumes is a short-term release of backlogged surgeries - or, if a new paradigm is emerging in healthcare utilization with sustained, heightened surgical volumes unlocked as labor problems mitigate. To that end, Bank of America published a great, recent note covering utilization trends. 50% of the care delivery organizations surveyed signaled that strong volumes are here to stay - at least in 2023 - with 10% of respondents also noting an improving labor environment: |

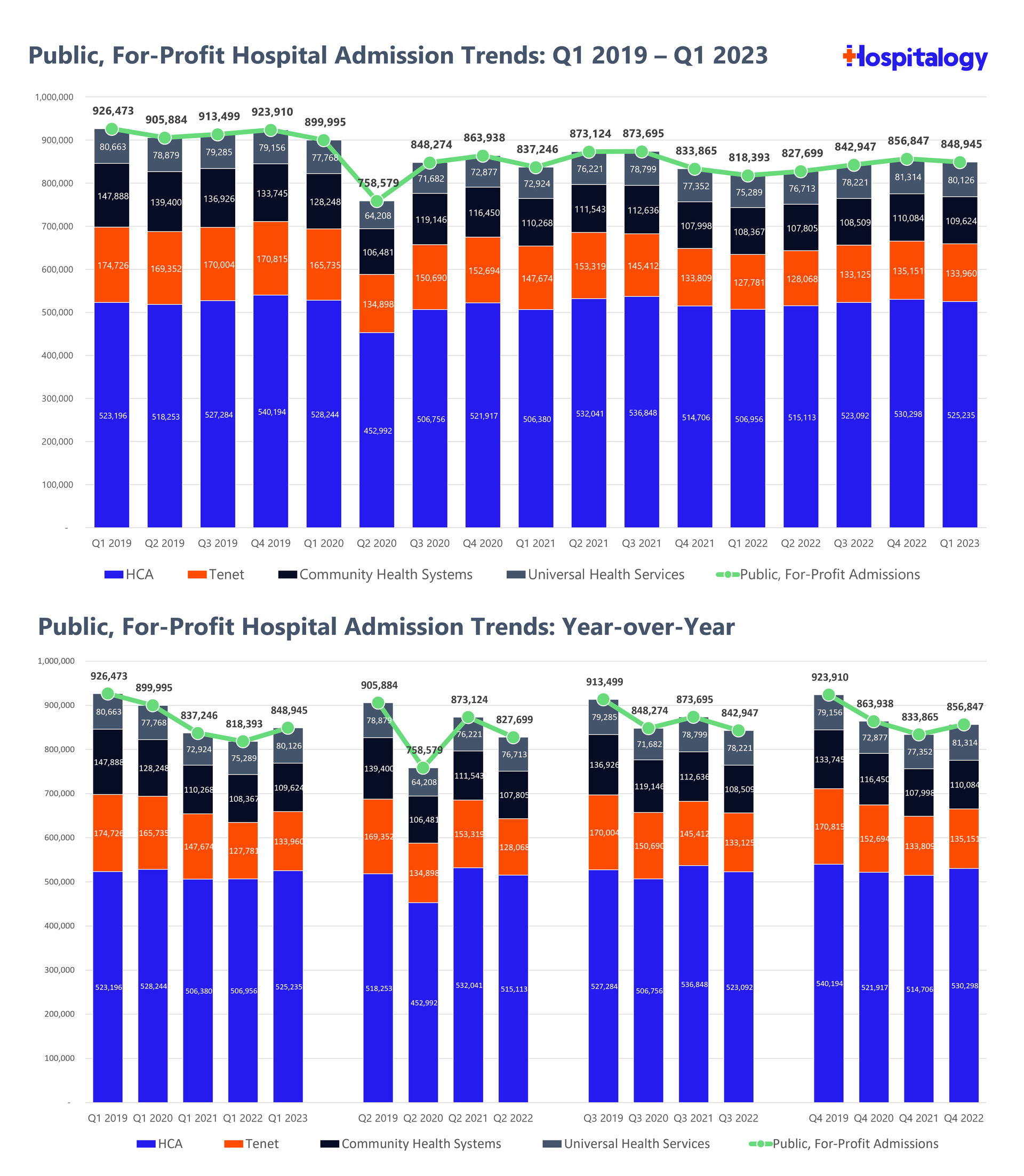

In its note, BofA concludes: "In general, Q1 feels like peak growth, but strong demand should continue." In my mind, volumes will continue to grow as provider organizations get their respective labor shortages in check - if ever. Meanwhile, inpatient growth has returned, but sits at, or below pre-pandemic levels. This is net positive for payors - in general, from a medical cost standpoint, they are much more concerned about inpatient utilization trends than outpatient growth: |

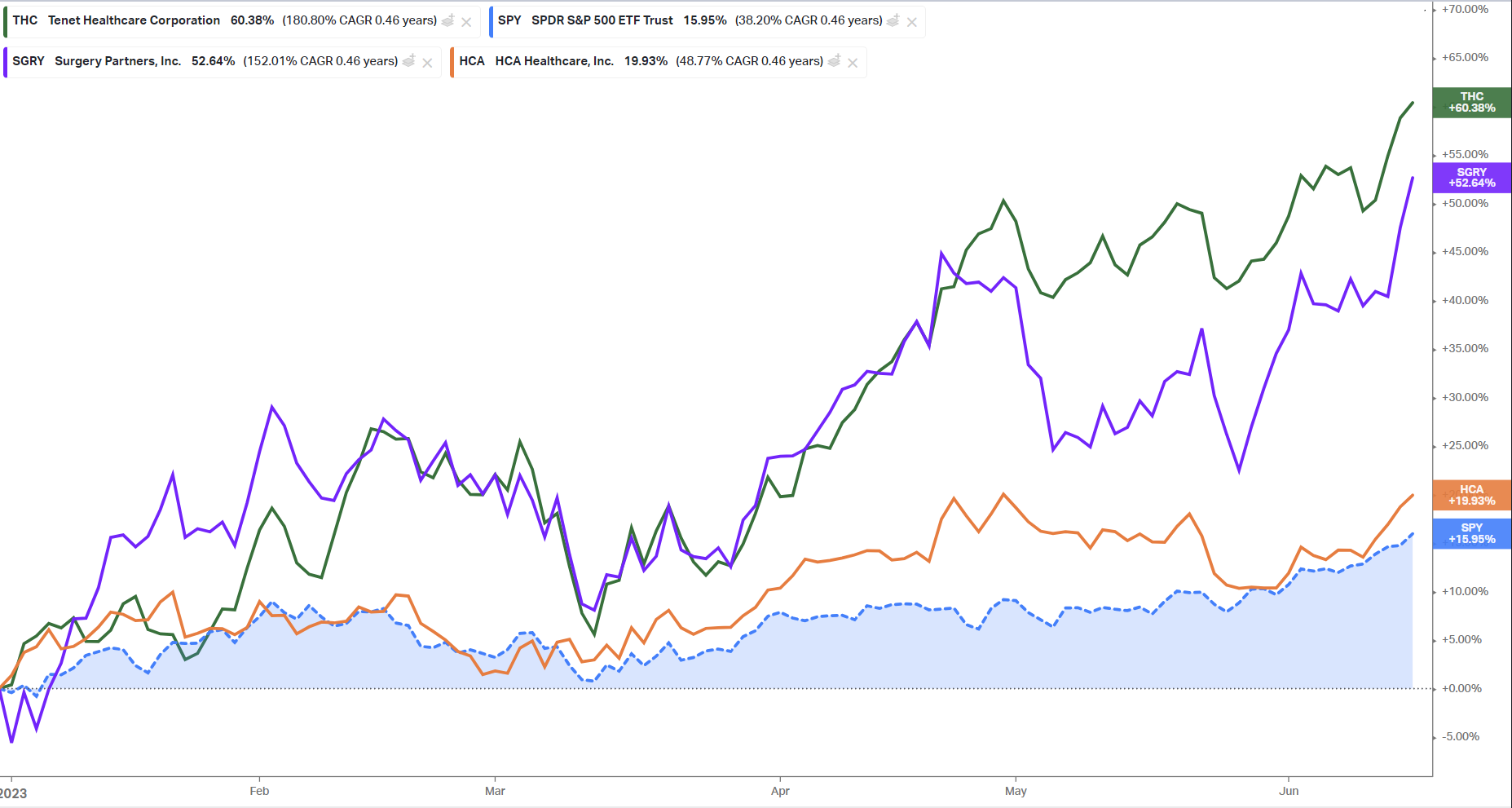

All of this to say that the selloff is probably overblown. A few blips on the medical cost ratio from higher than normal outpatient utilization isn't going to move the needle - yet. There are some headwinds on the horizon for payors, though - a dynamic I'll dive into in Part 2 next week. Who's positioned to win? The care delivery organizations with aligned physicians and the facilities to boot are poised to succeed long-term. Consequently, look for names like Surgery Partners and Tenet's USPI to enjoy nice volume growth while doubling down investment in orthopedic and cardiology service lines, two of the highest-margin, juggernaut specialties. |

Notice the June spike in these operators: |

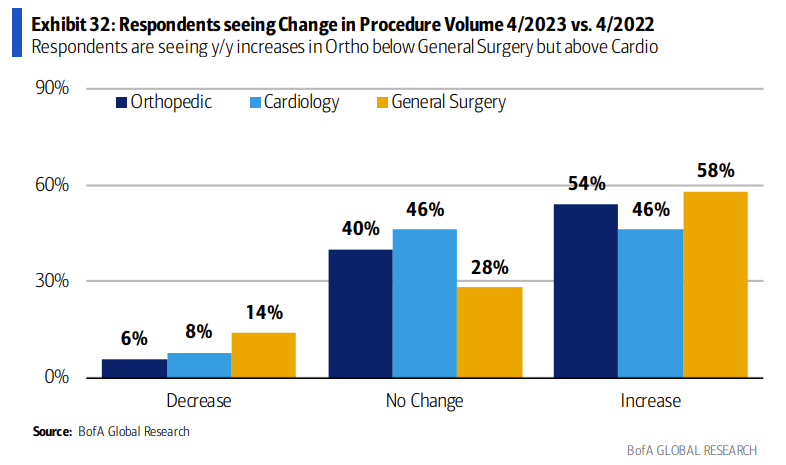

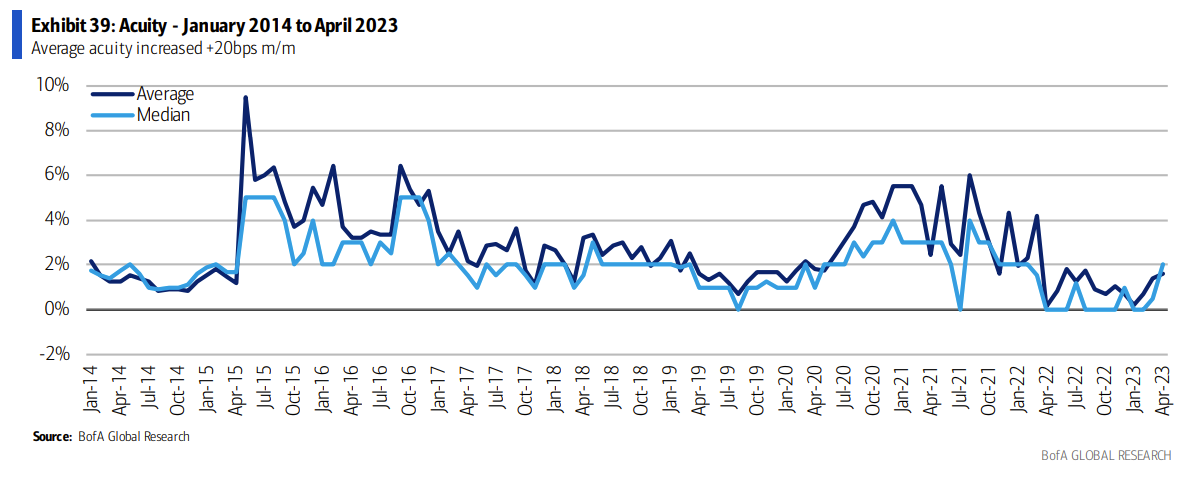

And as the outmigration continues and surgical innovation moves complex cases into outpatient settings, acuity will continue to rise in the those settings, benefiting those with the facilities and highly specialized physician alignment to meet that growing demand: |

The signal here is clear: those investing and operating in outpatient surgical growth will ride the secular tailwinds for the foreseeable future. Nonprofit health systems are taking note, too. From a recent Modernhealthcare article: - Other health systems are plotting their own expansions.

- Sacramento, California-based Sutter Health plans to add more than two dozen ambulatory care centers in the next four years, in addition to dozens of primary and multispecialty care sites.

- Henry Ford Health is investing $2.2 billion to expand its main campus in Detroit -- the largest investment in its 108-year history.

- AdventHealth's growth strategy includes expanding its outpatient operations, with plans to double its number of urgent care centers to more than 100, he said.

From a health system perspective, you have to ask yourself some tough questions. Where is utilization returning? To which markets? What service lines? Outpatient migration is driving the utilization train now. Inpatient beds are excessive and aren't going to be full. If you don't have that continuum of care from a system lens, things could prove difficult. Finally, the next battleground between payors and providers will emerge over outpatient utilization. We're already seeing that dynamic play out with UnitedHealth's most recent attempt to rev up prior authorizations for GI procedures. GI and endo groups now have to collect and submit documentation in support of future endoscopy procedures. I wouldn't be surprised to see more widespread ASC utilization management come to a head in the near future. In Part 2, I'm going to discuss heightened utilization trends and their effect on payors as well as downstream value-based care players, and a potential end to the Goldilocks Era if payor headwinds come to fruition. |

|

|

Over the past few months, we've launched a healthcare executive community called the Board Room to leaders in healthcare who want to stay ahead, be better informed, and network with others across healthcare silos. Now we're up to 30+ thoughtful healthcare professionals and the discussions have been amazing around pressing topics in healthcare - including what's actually going on with AI in healthcare, or emerging investment themes in value-based care. Stay ahead with monthly executive briefings, expand your network, and get an extra e-mail send on Sundays from me chock full of resources I don't share with the wider audience by joining the Board Room. For decision makers in healthcare, learn more about membership at the link below. |

|

|

- I hope everyone has a wonderful Father's Day. I'm spending it with my family playing the Texas Rangers Golf Course and then watching the U.S. Open! Respond with your pick to win.

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

| Get your brand in front of 26,000 executives and healthcare decision-makers. |

I'm building an exclusive community for top healthcare executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments