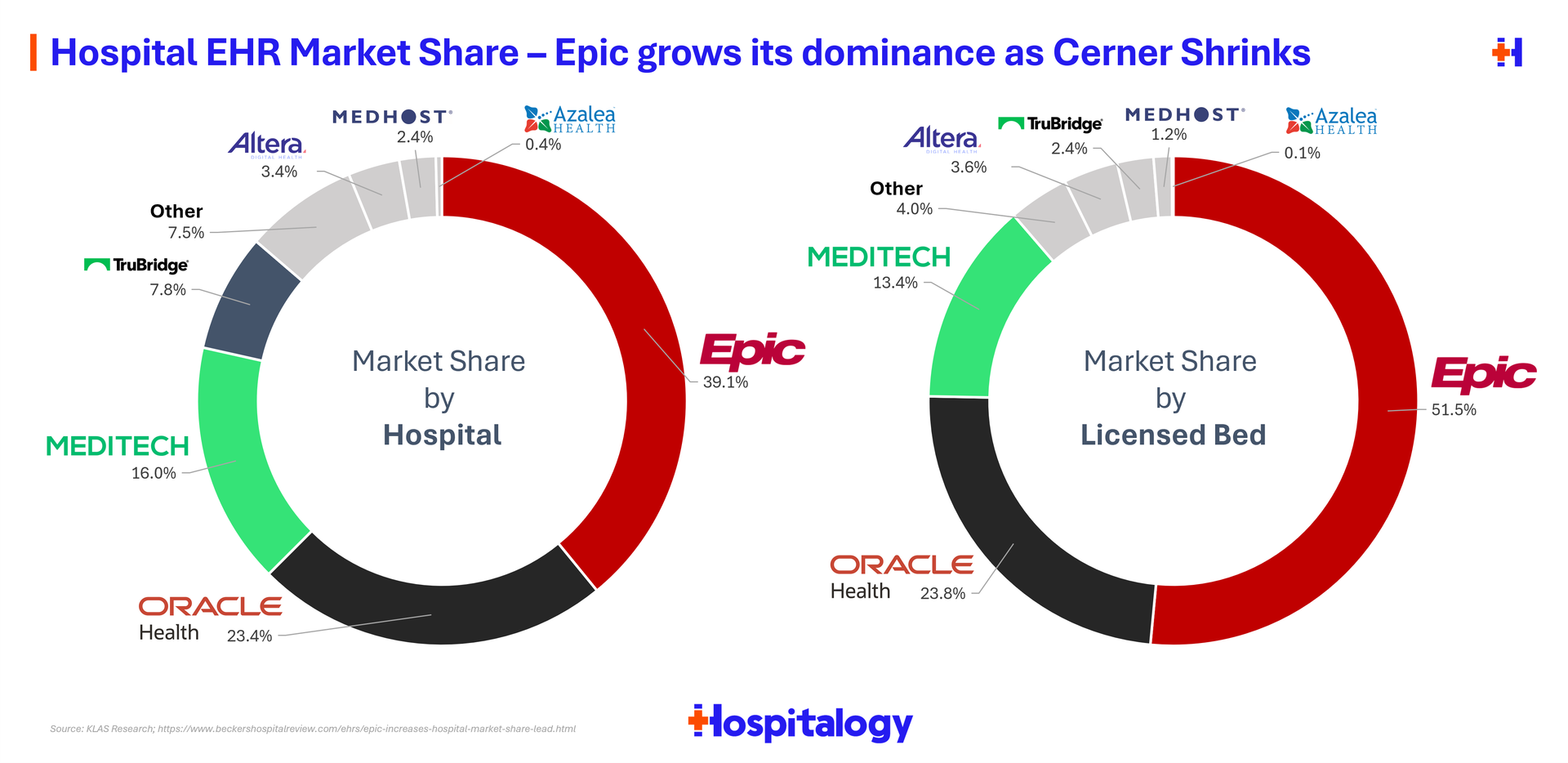

The FTC's suit against healthcare private equity player Welsh Carson was dismissed late last week over whether it held any liability in the FTC's case against U.S. Anesthesia Partners (USAP). Turns out, as a now-minority shareholder in USAP, it doesn't hold any liability:

Translation: A minority shareholder receiving distributions or holding interest in a company that may be in violation of antitrust isn't itself violating antitrust.

Despite the win for WCAS, the antitrust case against USAP is advancing given its rollup strategy to dominate the anesthesia market and subsequent actions to stifle competitors were considered illegal. Back in 2012, WCAS formed the anesthesia physician practice management company, and it was one of the first pioneering rollups conducted in healthcare.

WCAS correctly identified the anesthesia (and most physician services) market as fragmented and a financial opportunity. By consolidating a specialty in high demand and low availability, it could corner certain healthcare markets, acquire anesthesia practices, apply higher rates to acquired practices, and leverage its expanding footprint and dense market presence to negotiate higher prices for the physician service needed in just about every surgery under the sun.

Good business strategy? At the time, yes. Now, with high interest rates and inorganic growth concerns, the PE-backed PPM model is increasingly past its prime.

Takeaway: The USAP case is an ongoing poster child for the FTC's crackdown on private equity involvement in healthcare. Most notable to me, though, and something that shouldn't be lost on readers, is the fact that any player with a dense, dominant market share position will use that power to maintain its positioning and maximize its business potential, patients be damned - whether that's a PE-backed player, a health system, or a payor.

Of course, two wrongs don't make a right, but you need to understand any rational actor, especially one with an incentive to juice growth on a relatively short-term investment, is going to take advantage of any edge they have. In some cases, that edge may be too great and end up teetering toward illegal or harmful - which is what we may see ultimately play out with USAP. There are elements of decisions USAP made - like paying Envision to stay out of its market, or pursuing out of network pricing strategies - that should've never happened.

Broader industry practices aside, this result is a win for private equity from a liability standpoint. Case after case continues to maintain precedent that private equity parent companies are not liable for their portcos' behavior. Still, from a public perception point of view, private equity and players involved continue to get dragged through the mud - intentionally - by the FTC as patients and other healthcare participants hear about behind-the-scenes business tactics at play.

Until some form of accountability takes shape for excessive bad acting in healthcare, we will continue to see these stories play out across healthcare verticals. Some common sense reform is needed.

.png)

No comments