Happy Election day, Fam. I'm currently recovering from a 20 hour travel day with a one year old after some terrible Dallas weather, so today we're diving into an article I wrote for my community about a month ago on the evolving vertically integrated oncology landscape, with some big questions for value-based oncology care. A lot has happened in 2024 with players snatching up community oncology networks, and I thought it'd be interesting to dive into the current landscape and economics at play. If you have any thoughts on any of this I would love to hear them! This article was/is for the community, so it will stay published in this newsletter. It's live on the community HUB here. For Hospitalogists interested in joining the community, apply here! Those in strategy & ops roles at hospitals / health systems will get the most out of joining. |

Was this email forwarded to you? |

|

|

I don't have to tell you that technology is reshaping patient care. But here's something you might not know: WellSky is leading the charge in intelligent, coordinated care for patients, physicians, and healthcare organizations. They cover everything from care management to transitions, all with one goal: transforming the entire care journey to improve patient outcomes. Curious how this looks in practice? Meet Mr. Clark. After a serious fall, he's now receiving the precise care and services he needs to recover – watch the video to see how. |

|

|

Vertical Integration in Oncology |

The oncology market is undergoing a profound transformation, characterized by aggressive vertical integration, skyrocketing valuations, and a race to secure oncology practices.

This shift is reshaping the healthcare landscape, particularly in how cancer care is delivered and financed. At the heart of this change is the recognition of oncology's unique position in healthcare - a specialty where drug spend is massive and growing rapidly, creating opportunities for significant financial gains through strategic acquisitions and partnerships. |

Key Takeaways on Vertical Integration Trends in Oncology |

- Most oncologists (~70%) are employed by or aligned with health systems, and the bulk of oncology spend sits there.

- The oncology drug pipeline continues to be incredibly exciting and innovative yet…costly. Expenditures will rise 8-10% per year for the foreseeable future.

- There's a scarcity of community oncologists that drug distributors are trying to acquire as a vertically integrated asset, creating an intense land grab and bidding wars nationwide.

- Looming regulation like the Inflation Reduction Act, M&A scrutiny, and non-compete drama create large unknowns for operators in the space.

- Value-based oncology care, while promising, is not done in any meaningful way today in oncology care - if costs are rising by 10% per year, how do you appropriately contract against that, and how to 2 parties come to terms on cost reduction initiatives? Questions - but also promise - remain to see material adoption of VBC in the space.

|

The Unique Position of Oncology in Healthcare and Vertical Integration |

Oncology stands out as perhaps the only medical specialty where this level of vertical integration and financial engineering is possible, simply based on how many ancillary services and associated levers exist.

These unique characteristic makes oncology an attractive target for investors and strategic players, and consequently, capital is flooding the space.

At the same time, there's a perceived scarcity of oncologists. 70% of oncologists align or are employed by a health system, leaving the remaining share as red-hot acquisition targets, and leading to upside-down economics on deals: vertically integrated players are overpaying for oncology practices, and this creates a flood of downstream economic incentives to make up the difference.

Let's take a quick dive into the major oncology vertical integration space. |

The Great Oncology Land Grab Playing Out in 2024 |

In recent years, the oncology sector has witnessed what can only be described as a "land grab" for oncologists, and this phenomenon has only heated up in 2024 with several marquee deals. In 2024 the trend has accelerated by high-profile transactions like OneOncology's deal with TPG and Cencora (formerly AmerisourceBergen), the economics of which I covered here. The implications of this deal, particularly its 19x put/call multiple and setting a transaction price for platform-level deals, have reverberated throughout the industry, sparking a flurry of deals and dramatically inflating multiples. |

The pace of consolidation in oncology on the community side is staggering. While a majority of oncologists are employed by health systems, remaining independent practices have been targeted heavily by the big players. Demand for a scarce supply of community oncologists - despite the financial profile of the actual practice involved - has created a bidding war, and in most instances the large vertically integrated distributors are bidding against each other, worried their competitors will snatch these community oncologists away. The valuation effect alone is profound. In some cases, larger practices that were valued at 7x EBITDA in 2023 are now commanding multiples of 14x or higher in certain circumstances. From a recent WSJ article on this topic: - The competition among drug distributors is raising some eyebrows on Wall Street as distributors seem to be overspending to protect their turf. "First impression was the deal makes sense and par for the course," Baird analyst Eric Coldwell wrote of the McKesson Florida deal. After investigating further, he wrote, the firm was "growing less convinced about valuation." Stephanie Davis, an analyst at Barclays, wrote that the price reflected a "scarcity of high quality assets at scale," noting that McKesson's rivals were also initial bidders.

It is very interesting to note this phenomenon in healthcare, and we saw this with the clinic-based value-based care models as well: despite the economics and profitability prospects of the business, there are very few high quality assets at scale, which creates bidding wars for those that exist. As these assets vanish, distributors will move downstream to acquire even smaller practices as the land grab plays out. But who are the players involved? A quick overview next. |

Players Involved: Big 3 Distributors as the Major Oncology Vertical Players |

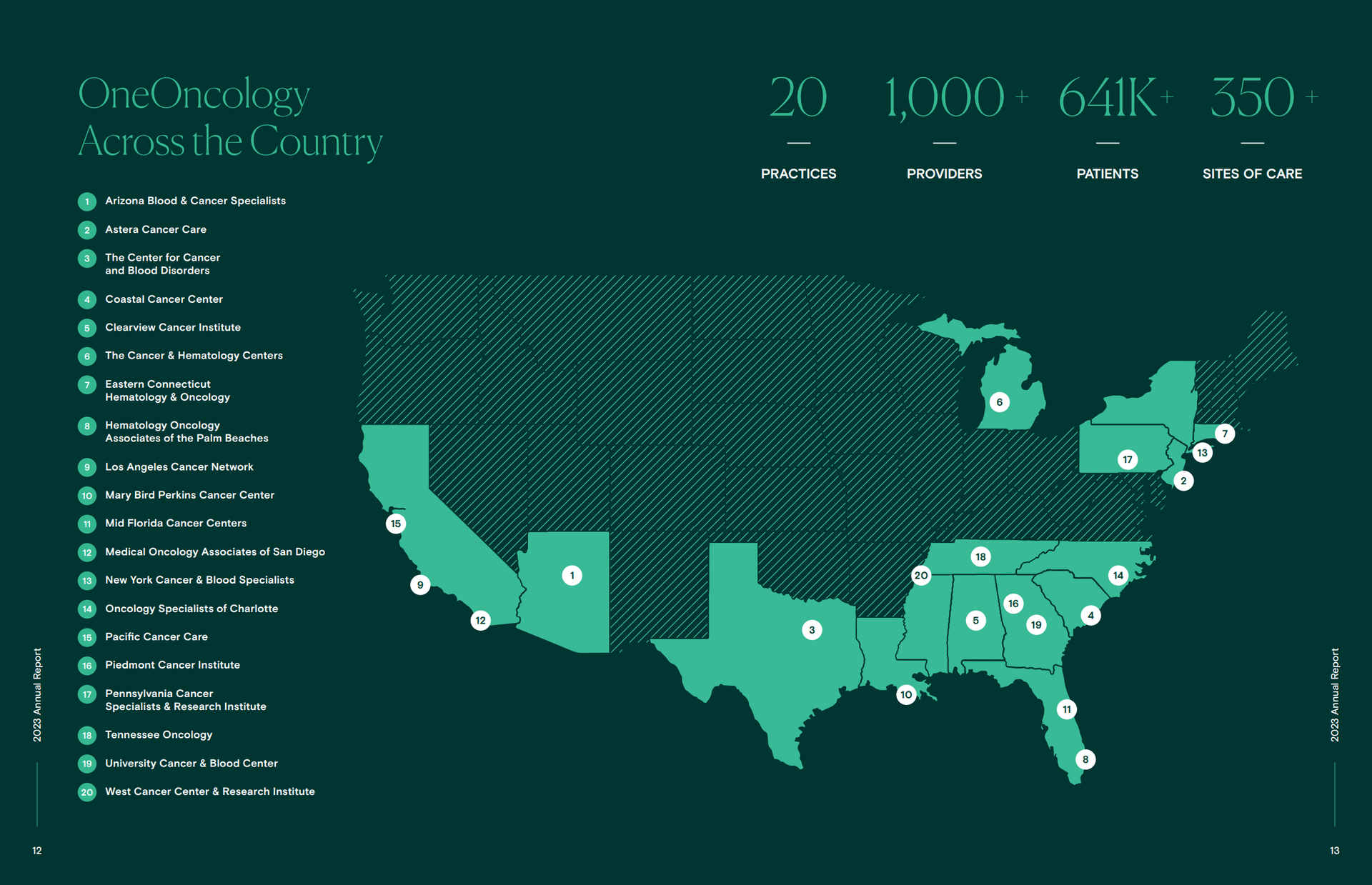

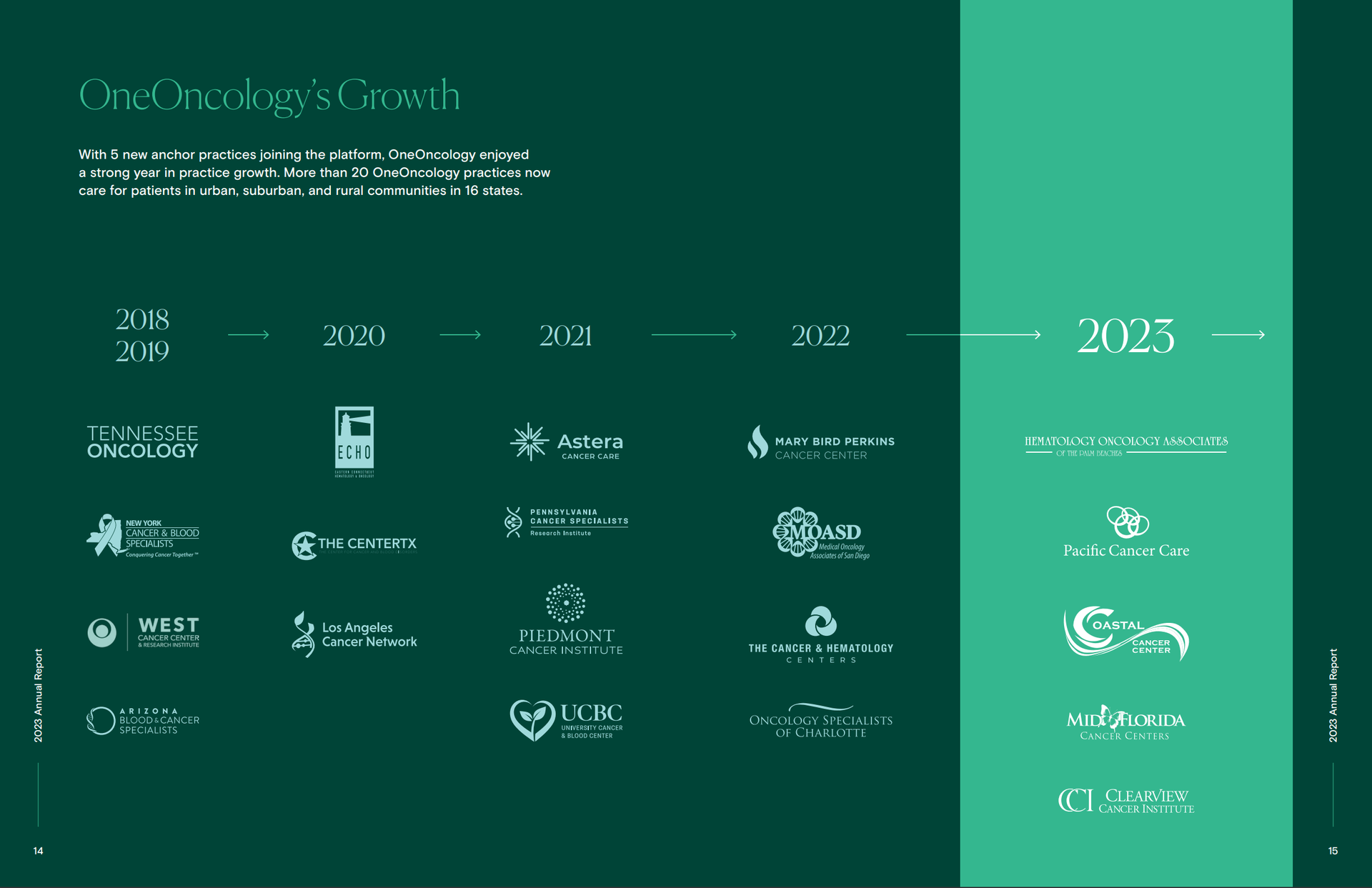

The oncology market is now dominated by a few key players, each aligned with major distributors: OneOncology is aligned with Cencora (AmerisourceBergen) and will be presumably be purchased by Cencora - currently owned by TPG - in the coming years. American Oncology Network also has a distribution deal with Cencora and we may see a deal here in the future. OneOncology as the flashiest asset in oncology MSO land holds 1,000 providers in 350 locations. Cencora currently holds a 35% stake in the enterprise. OneOncology in general is growing rapidly, and is expected to hit 50% or so growth year-over-year in 2024 after some notable acquisitions and a large acquisition in the urology space. |

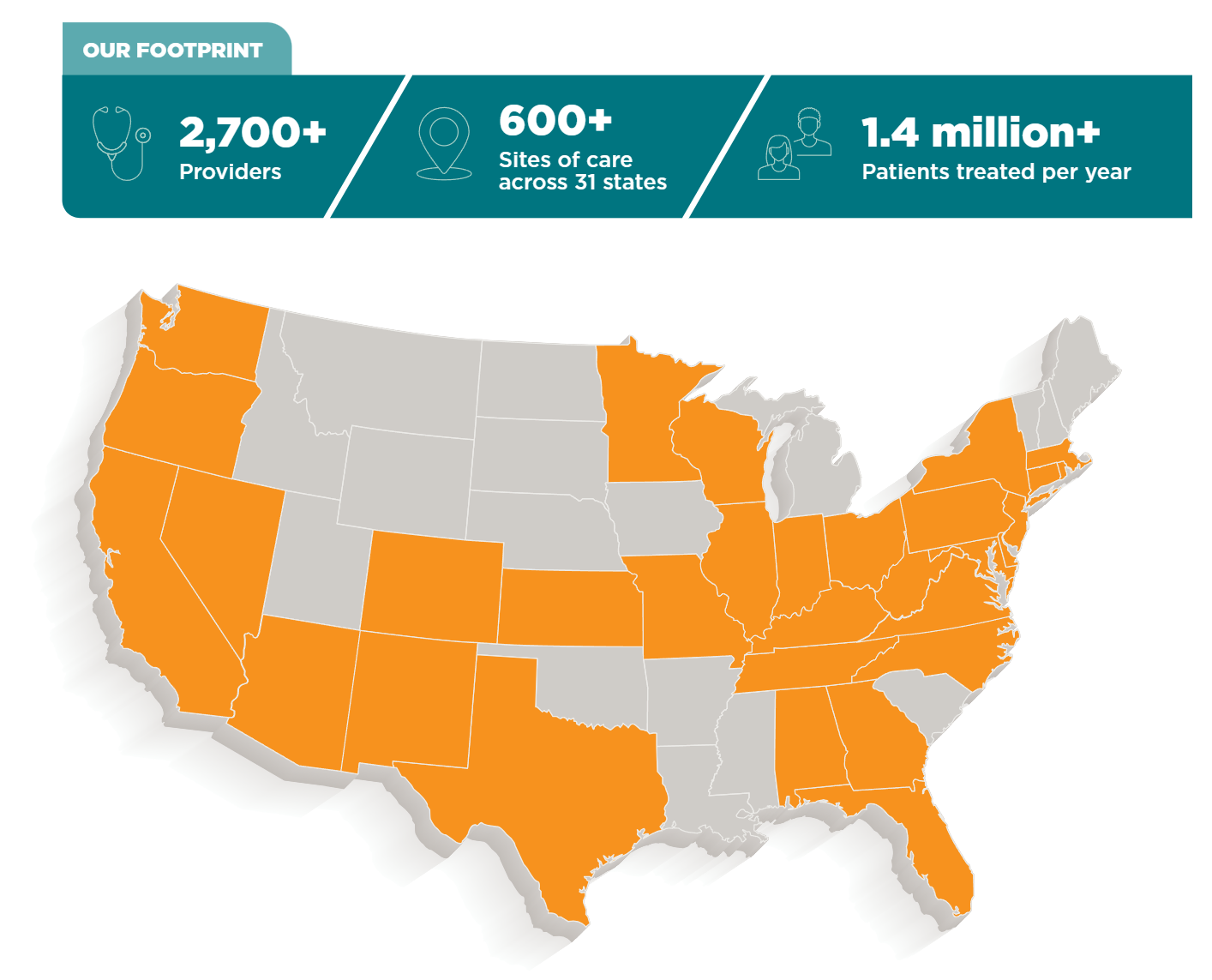

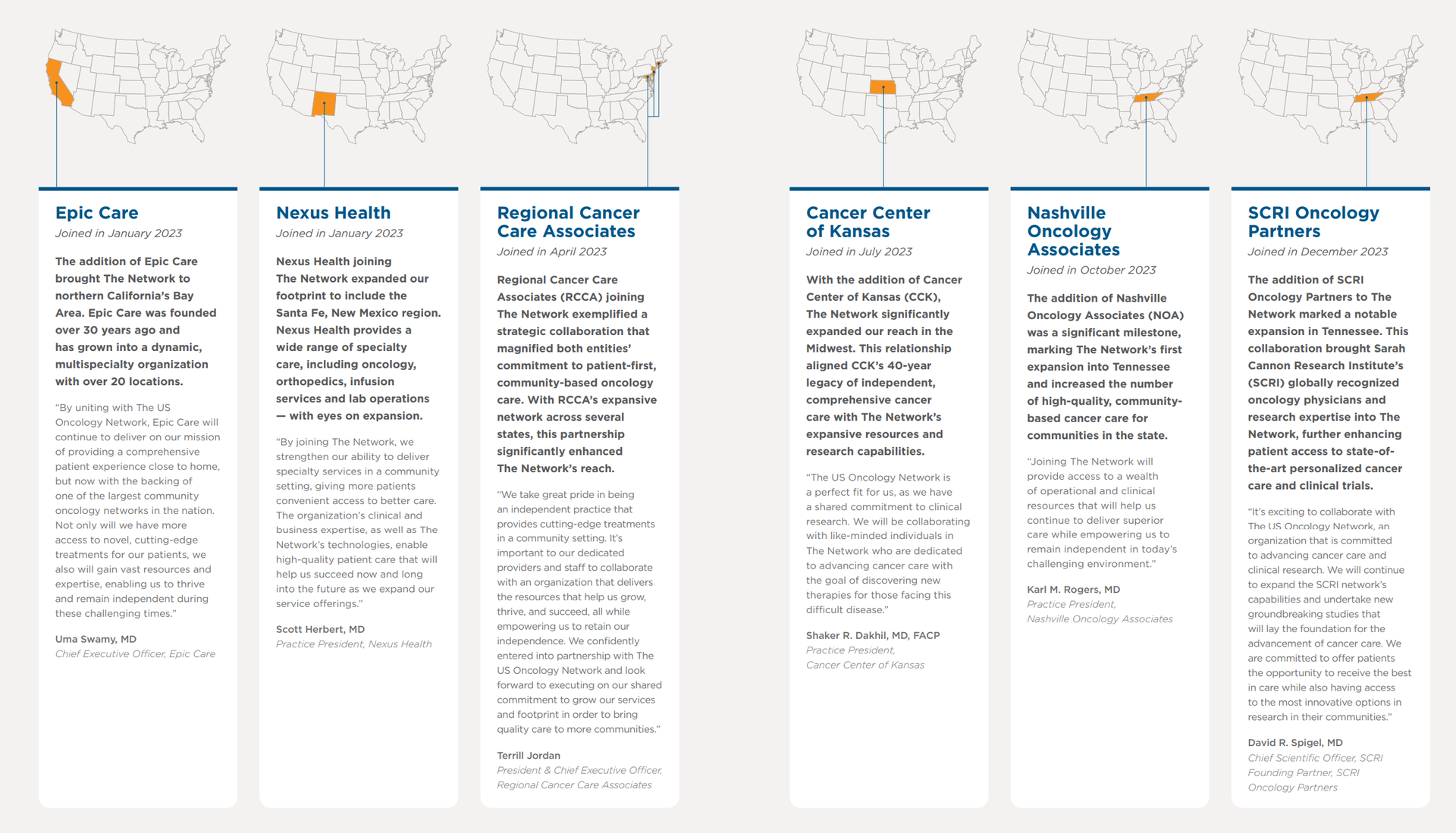

The US Oncology Network, acquired by McKesson in 2010 for $2.16B, is the 800 pound gorilla and created the first wave of vertically integrated oncology practices. USON is managed by McKesson and comprises over 3,000 independent providers across more than 700 locations. In 2023, it expanded by adding Epic Care (47 physicians across 21 locations) and Nexus Health (9 physicians). |

In 2024 USON landed a huge fish in Florida Cancer Specialists & Research Institute. McKesson acquired the 70% controlling interest for $2.49B in cash and from what I've gathered, while the practice is in more of a steady-state from a growth perspective, it's a huge land grab from McKesson to secure its place within a pot of huge drug spend. FCS is a practice with 250 physicians, 280 APPs, and 100 locations across Florida with every cancer care ancillary you can think of. Assume the entire practice is worth $3.6B based on the 70% purchase price. At an assumed EBITDA multiple of 20x, total EBITDA generated sits at around $178M. So while McKesson might have overpaid today for FCS, in the future with growing cancer prevalence and expected drug spend trends, it will more than make up for it long-term - assuming the physicians stick around. In general USON is the market leading practice and will continue to scoop up physicians left and right. |

Integrated Oncology Network: In September 2024, Cardinal Health announced its acquisition of ION for $1.1 billion. ION operates over 50 practice sites with more than 100 providers across 10 states. To me, and from what I understand, this was a 'keeping up with the Joneses' kind of move, because once most of the oncologists are scooped up, what are you left with? In the minds of those I spoke with, Cardinal Health bought a dumpster fire of an asset here and panicked, realizing it didn't have a scaled oncology MSO and it was losing ground to Cencora and McKesson quickly. So, it opened up its pocketbook. |

Other smaller or non-vertical players include The Oncology Institute, GenesisCare, Oncology Care Partners (backed by Welsh Carson Anderson & Stowe), City of Hope, the aforementioned American Oncology Network (which once was expected to go public via SPAC) |

Then you have the flashy group of value-based specialty enablement players including Thyme Care and Reimagine Care which help try to create better patient experiences and work with oncologists to provide resources and technology in order to unlock additional revenue streams by participating in risk and the Enhanced Oncology Model where applicable. |

Drivers of the Oncology Boom - it's all in the specialty drug spend |

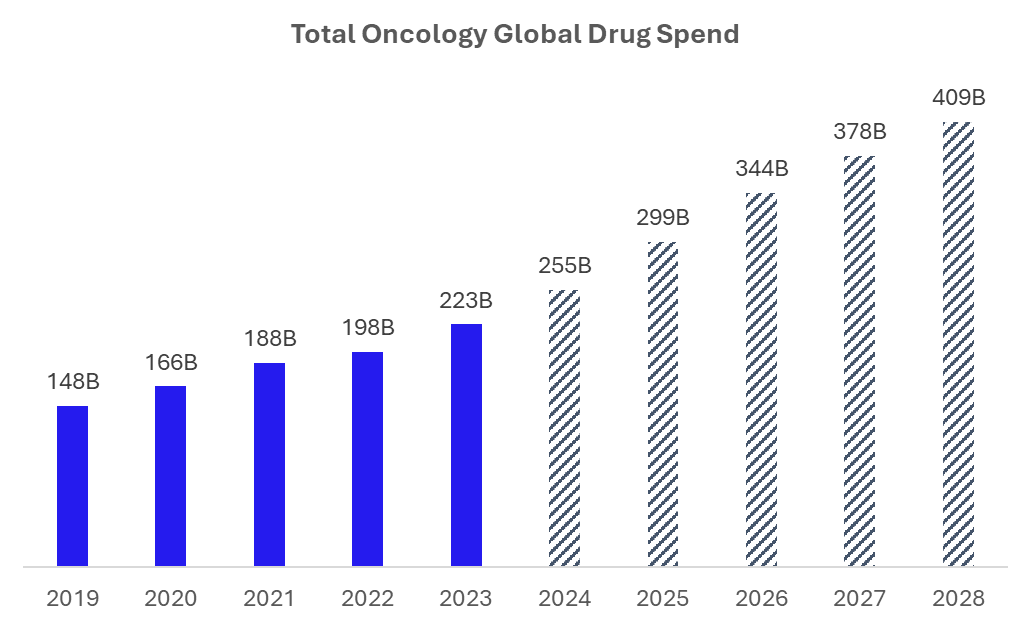

Source: IQVIA Several factors are fueling this unprecedented interest in oncology practices: Scarcity of Oncologists: There's a limited supply of oncologists, making established practices highly valuable especially amidst panic buying. Growing Cancer Drug Market: The market for specialty cancer drugs continues to expand robustly, with an average spend per oncologist of $10 million, growing at 8-10% annually to $409B by 2028 per recent estimates. That's a ton of money and a huge driving force in the industry. Vertical Integration Strategy: Distributors and Group Purchasing Organizations (GPOs) are realizing the strategic importance of securing direct access to physicians given the growing scarcity and state of hospital employment in the oncology specialty. Long-Term Contracts: Distributor / purchase deals in this space often involve 20-25 year contracts, protecting drug distribution market share and providing long-term stability as well as diversified revenue streams - locking in margins on both the distribution front (typically 2-3%) and also upside in the practices themselves. Not to be discounted is the effect of the Inflation Reduction Act on specialty drug demand and downstream impact. Now that senior out of pocket drug costs are capped, it's very possible we see another boom in demand for high cost drugs - and resulting increase in premium dollars. The impact of this legislation on drug pricing and negotiations remains a significant unknown. How does this program morph over time? What drugs and how much of the spend is negotiated? Important questions to consider as a key regulatory risk. |

The Economics of Oncology Practice Acquisition |

The financial mechanics behind these acquisitions are complex but lucrative. When a company like OneOncology acquires a practice, they're typically buying a 20% compensation scrape (meaning that partner physicians take a pay cut to be acquired, but receive a lump sum payment in kind).

As an example, a practice generating $25 million in earnings will have something like $250 million in drug spend depending on patient mix and acuity. Through vertical integration with a distributor, Cencora can double-dip into the practices earnings: (1) through making the practice more efficient (By leveraging their scale, MSOs like OneOncology can negotiate better rebates and rates, potentially growing a practice's earnings from $10 million to $12.5 million simply by applying their more favorable contracts after integrating the practice.), and (2) through drug spend margin.

The drug spend itself, while operating on thin margins of 2-3%, represents a massive volume, and drug spending for oncology - both by price and by volume - is expected to continue to ramp considerably over the coming 3-5 years as new drugs and therapy applications come to the market through various drug pipelines.

There are plenty of other ways to unlock value through these deals. For instance, an integrated oncology MSO can help facilitate clinical trials, or incubate new technology, or drive other efficiencies by having a scaled asset with significant purchasing power. |

Trends in Cancer Treatment |

The oncology drug pipeline continues to be a source of innovation and excitement, as drugs come out that can quite literally cure many disease states. Oncology is no exception. The evolution of cancer treatment has progressed from traditional chemotherapy to immunotherapy, and now to more targeted approaches: - Antibody Drug Conjugates (ADCs): These are emerging as alternatives to chemotherapy, offering more targeted treatment with potentially fewer side effects.

- Combination Therapies: The trend is moving towards combining ADCs with immunotherapies, resulting in more effective but also more expensive treatment regimens.

- Biospecifics: These are being developed for both liquid and solid tumors and may eventually replace some immunotherapies.

This continuous innovation in oncology treatments is a double-edged sword. While it promises better outcomes and care for patients, it also contributes to the rising costs of cancer treatment. Patients are living longer and staying on these expensive therapies for extended periods, driving up overall healthcare costs but also making oncology practices more valuable in the long term. The healthcare game we play is one wrought with balancing these kinds of factors. How much should an oncology drug cost? As we can see, the incentives it creates at scale causes behavior like we're seeing between distributors and physicians, and I feel as if it's flying under the radar. |

What About Value-Based Care? |

In my mind, vertical integration of distributors and oncologists flies directly in the face of value-based care in oncology. In a vertical model distributors have every incentive to drive drug spend up to collect their margin. Any form of value-based oncology care today is likely limited to certain specific episodic disease states and/or better forms of patient navigation / preventing hospitalizations for patients. Things like monitoring patient vitals and heart health over the course of a chemotherapy treatment make a lot of sense and is a value-add for patient quality of life. Adding to this financial incentive of rising drug costs, value-based care's implementation in oncology remains limited in scope. The complexity and high costs of cancer care make it challenging to design effective risk-sharing models ESPECIALLY given the fact that most of the costs lie in the drug expenditures. The money's in the drugs. At least, topline revenue is. And small percentages of big spend still adds up to quite a stack of cash. High-Cost Patients: In value-based arrangements, a single high-cost patient can significantly impact the financial performance of a practice or network - which gets very tricky for scaling oncology enablement players who might be more loose in taking on downside financial risk for oncology patients. - "Value-based care transformation in cancer requires more than just aligned financial incentives, it requires a deep understanding of where the opportunities for enhancement and cost-savings lie, an emphasis on reduction of acute care utilization, and an appreciation for novel solutions such as patient navigation that payers and practices may find difficult to fund and build in-house." from my chat with Thyme Care.

The other side of the equation I'll mention is if drug distributors and their oncology MSOs are incentivized or want to take on risk, and therefore transition their partner oncologists to risk-based models. Physicians in an oncology setting may prefer getting paid per patient, and the drug spend would still be there in theory. Time will tell as to the ultimate path for these decisions. |

The Future of Oncology Care - What's Next |

As the oncology landscape continues to evolve, several key questions emerge: Quality of Care: How will the consolidation and vertical integration of oncology practices affect the quality of patient care? While some integrated systems like Kaiser have shown improvements in quality, the long-term effects of widespread consolidation remain to be seen. Really what this boils down to is…is vertical integration in oncology simply financial engineering, or will we actually seeing better outcomes, efficiency gains, and innovative solutions over time? The same question goes for payors-providers in vertical integration. Finally, these ongoing issues put value-based care in between a rock and a hard place in oncology, despite the efforts to include things like drug spend in the latest enhanced oncology model. Patient Choice: As networks become more integrated and potentially more closed, how will this impact patient choice and access to care? Regulatory Scrutiny: As these deals grow in size and impact, will they attract more attention from antitrust regulators? The oncology market is at a crossroads, with vertical integration and consolidation reshaping the landscape at a breakneck pace. While these changes promise efficiencies and potentially improved care coordination, they also raise concerns about market concentration, patient choice, and the overall cost of cancer care. As the industry moves forward, balancing the drive for financial optimization with the fundamental goal of improving patient outcomes will be crucial. The next few years will be critical in determining whether this new, more integrated oncology care model can deliver on its promises of better, more efficient care, or whether it will require further refinement and regulation to truly serve the needs of cancer patients. |

Resources and further reading: |

|

|

As I've written about before, data breaches and cyberattacks in healthcare are escalating. Breaches now occur almost weekly, costing the industry an average of $10.1M per incident 😱 So, how can we prioritize safeguarding patient data amid these rising threats? The HITRUST CSF certification stands as the gold standard in cybersecurity assurance, demonstrating a commitment to protecting customers' sensitive data. Vanta and HITRUST have joined forces to offer a HITRUST Certification checklist, streamlining the certification process for organizations by outlining the essential step-by-step criteria for achieving this sought-after framework.

Download it today 👇

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 40,000 executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments