PARTNERED WITH  |

|

|

Hospitalogists, Another week down and it's already mid March. Q1 is nearly over. Isn't that crazy? Today we're diving into Part 2 on all things Hinge Health. If you missed Part 1, you can find this full essay now published on Hospitalogy.com - and here's the link. Thanks for those of you who replied with your thoughts. I have memorialized some of them below along with some open ended thoughts! Finally, be on the lookout for Kevin O'leary's write-up likely coming soon - he always puts great pen to paper on S-1s and I enjoy reading his perspective. Health Tech Nerds is the place to subscribe for that. Chrissy Farr's note was also a nice overview. If you're chronically online like me, then you have probably seen 500+ takes on Hinge. Just keep the receipts for me! |

Was this email forwarded to you? |

|

|

SPONSORED BY PHRMA PBMs should share savings on medicines with you. PBMs get rebates that can lower the cost of some medicines by 50% or more. But you often pay full price at the pharmacy. Medicine savings should go to patients, not middlemen. |

|

|

My Questions + Open-ended Thoughts on Hinge's S-1 What's in the tech? One of the biggest points of emphasis I personally have, and one thesis I have yet to see play out at scale, is that 'tech-enabled' = superior margins to traditional healthcare delivery counterparts. Maybe Hinge is the first time that the VC-driven thesis plays out. For all of our sakes - I hope so! Hinge mentions its AI-powered motion tracking tech, TrueMotion reduces human PT and care team hours by 95%. And here's the math backing into that, from a footnote on the bottom of page 134. I found the math absolutely fascinating: - We estimate the reduction in human care team hours enabled by our platform by assuming an average of 11 outpatient orthopedic patients are treated with in-person physical therapy per eight-hour day. Assuming in-person physical therapy is delivered eight hours a day, five days a week and 48 weeks a year, each physical therapist can deliver approximately 2,640 sessions per year.

- Our platform delivered approximately 25 million activity sessions in 2024, which were facilitated by 438 care team employees on staff for an average of approximately 57,750 activity sessions per year per care team employee.

From 2,640 sessions per year to 57,750 sessions per year! That's a 20x + boost in productivity if the activity sessions are apples to apples. Behavioral Health savings note is interesting. It's notable for Hinge to highlight the behavioral health benefit of their offering. In their case study section, Hinge notes a 50% reduction in depression among members. Since behavioral health massively exacerbates medical spend and utilization in populations, this datapoint is probably a nice 'bonus' for payors to see. |

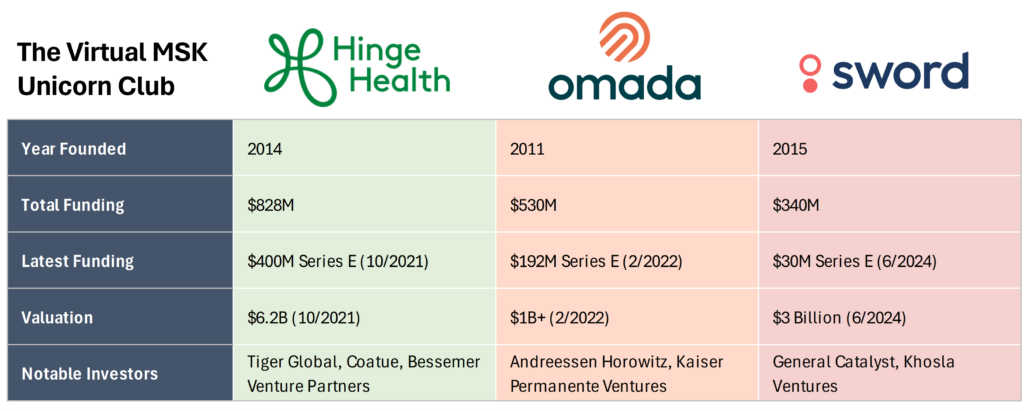

Does Virtual MSK …Work? I'd be remiss to mention the Peterson Health Technology Institute report on virtual MSK solutions, which tried to provide an objective vetting of the various companies in the space - Hinge obviously being one of them. Any potential qualms about methodologies beside, PHTI found that physical therapist-guided solutions (Hinge, Omada, Sword, Vori, RecoveryOne) "can be an effective alternative to in-person PT and have the potential to reduce healthcare spending." Stated differently, they are comparable to in-person PT. Which, if ultimately true, is huge for scalability and access to PT for the rest of us. |

All of the above being said, I have been met with some skepticism related to the comprehensive role / scope of virtual MSK care. Can it truly replace, or are there elements of cherry picking? As one subscriber commented, "are we poking inside the cage with a very long stick, or are we actually solving the PT access problem?" |

Hinge Health: Bull or Bear? Bull Case: - Employers, now more than ever, are looking for ways to reduce healthcare costs. We're seeing a larger appetite for employers to engage in more 'creative' ways to save money and reduce premium spend.

- I've heard the leadership team are absolute killers and it's hard to bet against driven, passionate people like that!

- According to NPS and customer data published, Hinge customers and end users are satisfied with the products and services offered. I've never used it so I can't speak to it personally.

- MSK is a massive, growing market - orthopedics is, and will continue to be, a top growing service line at hospitals and ASCs nationwide. Chronic pain from MSK is rampant in the U.S.

- AI-enabled care teams can supercharge physical therapists to be much more productive, proving out the tech-enabled services thesis and introducing automation into the care team model. Over time, agentic AI could, conceivably, create true SaaS models and companies like Hinge would be in prime position to capitalize on that trend.

- Contingency-based pricing - downside risk - is attractive for employers and payors, and there's plenty of frothiness / savings available in the commercial market given over-utilization of pain management services (injections, unnecessary surgeries).

- At its current financial trajectory, there is a road to profitability, and Hinge was profitable in Q4 with an 82% gross margin.

- Opportunity to move into additional segments and service lines as sophistication of platform / offering advances.

Bear Case: - VALUATION FAM. VALUATION. It's not worth $6.2B today - its last private valuation back in 2021. I liked Grant Hesser's perspective here - and consensus seems to have spoken for the current value maxing out at $3B (and even this is generous). It's unfortunate this point has less to do with Hinge's actual business and more to do with the investor motivations happening behind the scenes. If we do the smart thing here, Hinge should have a successful debut. But the market environment has deteriorated…timing around the IPO isn't great with current market conditions and recession fears. Wouldn't surprise me if Hinge pulls the IPO altogether to wait for a sunny day.

- Questions abound around whether virtual PT can truly replace in-person PT or holds a more niche offering. Further questions around whether employers and payors on virtual MSK solutions see one short-term cost savings pop but struggle to see long-term downstream savings materialize. It's also reasonable to question Hinge's clinical evidence and cost savings studies / analysis.

- Replicability / copycats. Is Hinge's product, technology, data moat, and overall offering superior / differentiated enough to provide it with a sustainable competitive edge, or will payors and other providers be able to copy it with ease? Will we see a race to the bottom over time as centers of excellence develop their own solutions?

- Long-term sustainability of profits - are we seeing a short-term juicing of the books to make things look better than they actually are? Does Hinge have a reliance on employers / workers comp for profitability, and how will movement into other segments affect profitability?

- Long-term effect of GLP-1s on utilization of MSK services and chronic conditions (very existential, I know)

Verdict: Would I Invest? Alright, so none of this is financial advice. Just take a quick peek at my portfolio to know you shouldn't listen to me. That being said, would I invest in Hinge Health given what I've seen today? I like the virtual MSK / 'AI care' space, and it's an area with plenty of opportunity for growth particularly as these companies potentially move into other segments. And on top of this thought, I'd like to invest in a new company taking a crack at the public markets. But for me, it's ALL valuation dependent. I'm guessing Hinge will try to over value itself. So I'll say a contingent no, but I'd like to reiterate this business is one of the better tech-enabled services firms we've seen economics-wise in hitting the public markets. If you're paying 15x trailing revenue for it though you're crazy. Just my opinion. I mean, it's also possible Hinge is just the 'Yahoo' of virtual MSK / AI care companies. |

Join my Hospitalogy Membership! If you're a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Join for free today. |

SPONSORED BY COMMURE Commure's Ambient AI is transforming how clinicians interact with patients.

Dr. Neel Palakurthy, for example, cut his charting time by 50%, reclaiming hours in the office and at home.

Better care, happier patients, and higher revenue have directly followed.

"With the EHR, you're so focused on getting this checklist of things done. The ability to look at a patient and dictate their history, rather than charting it and staring at the computer—there's a definite benefit to that." Want more time and happiness?

Consider this your green light. |

|

|

How bout them Longhorns? Is Rodney Terry about to scrape his way into the tournament? Either way, March Madness is here, and you know what that means, Hospitalogists. The Hospitalogy official March Madness bracket challenge is upon us. Join the fun here! I'll send the winner some Hospitalogy golf balls or something. |

|

| Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 40,900 executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments