PARTNERED WITH  |

|

|

Ladies and gentlemen, we have our latest digital health IPO after a long hiatus. It's Hinge Health, a tech-enabled provider of virtual musculoskeletal care serving self-insured employers and payors. I couldn't help myself and spent most of my day yesterday reading the S-1 and doing some rudimentary analysis. I'm sure others will add plenty of thoughts and nuance to this conversation, but I'd love to be stick my neck out here with some thoughts as I read through and did some financial work.

So, without further ado, here's the Hinge Health breakdown, Hospitalogy style. Part 1 is today, then Part 2 will be on Thursday. Both parts will be published together by the end of the week. Finally, don't forget about my happy hour today in Austin, for those of you around! Register here. Driftwood Downtown, 5pm sharp. |

Was this email forwarded to you? |

|

|

SPONSORED BY COMMURE Healthcare isn't broken due to a lack of technology—it's drowning in it. Forty logins. Endless admin tasks. A system so fragmented it's burning out the very people keeping it afloat.

A single AI-powered platform can help change that.

Leaders from HCA Healthcare, Jefferson Health, and Commure sat down to rethink how technology should work for clinicians, not against them.

No more patchwork fixes; just a smarter, integrated way forward. AI-powered platforms are rebuilding the system with a unified, scalable approach that lightens the admin load and elevates care delivery. See AI-powered healthcare in action.

|

|

|

Hinge Health S-1 Deep Dive: Part 1 |

Note that in this overview I'm not diving into / questioning the evidence Hinge or any virtual MSK company provides for its cost savings / ROI value prop. I'm taking these claims at face value. |

The TL;DR on Hinge Health |

AI introduces a massive opportunity to solve the access and cost problem in physical therapy services related to MSK Care and beyond. - The MSK market is massive and pain management is a huge black box rampant with literal witch doctors who just inject your back with God-knows-what.

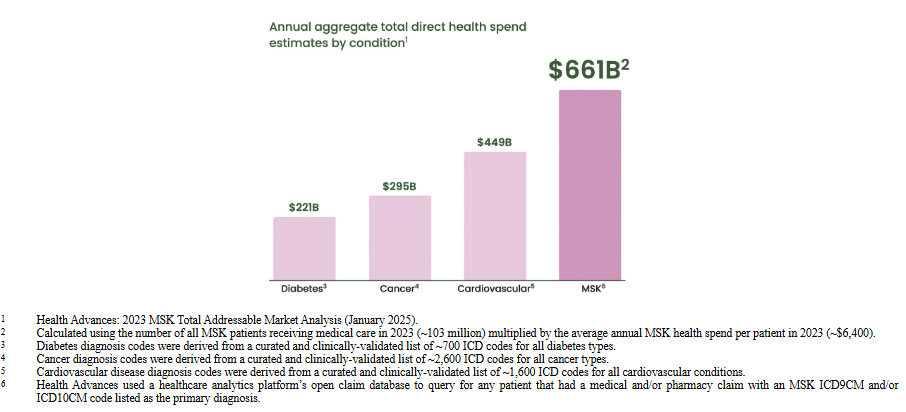

- MSK Market Size: $661B in MSK spend overall. $624B in 'indirect' costs, so $1.3T total. 40% of adults suffer from an MSK disorder as of 2021. PT is $70B of MSK spend and growing.

- Preventive and proactive services, AKA in-person physical therapy, isn't convenient and costs a decent amount out of pocket under traditional insurance models.

- Virtual MSK has emerged as a potential fix to this pain management problem.

- Hinge is a virtual MSK company. It provides AI-enabled, virtual MSK services to employers and payors, offering 24/7 services to their members for zero out of pocket costs and saving them money on the back end through decreased utilization of downstream services.

- Virtual PT claims to offer similar to better clinical outcomes, as patients adhere to personalized programs better and are equally or more satisfied.

- Hinge claims to have reduced human hours associated with traditional PT by 95%, or 20x more efficient/productive than in-person clinical PT - seemingly proving out the tech-enabled services thesis.

Hinge Health S-1 Link Here You should also read the letter from the CEO and Co-Founder, Dan Perez, starting on Page 129. Kinda buried but whatever.

(Side note: we really should all be exercising but I digress) |

This is AI!! Look at it!! The future!! Behold!! |

Intro to Hinge and Virtual MSK Here's the Hinge Health thesis: - Pain sucks. Lots of people have pain.

- Starting with musculoskeletal conditions, we can use software and AI combined with care teams to deliver a drastically better physical therapy experience, at scale, at a cheaper cost. Better PT = less pain, better outcomes.

- We'll prove our model saves money, then contract with employers and payors to help them save money, making money in the process.

- We'll expand into other conditions and services over time to help more people and make more money.

|

The TAM and the Problem: The Musculoskeletal (MSK) space has received an unbelievable amount of investment across healthcare, and for good reason. In general MSK is a rampant cost and access issue in the U.S. - people are in pain and want to fix that pain, quickly. Elderly falls lead to 3.6 million emergency room visits per year and cost over $80B. My grandma fell and broke her hip. My other grandma fell and was hospitalized for several days. Both received PT and rehab services. I should know!! |

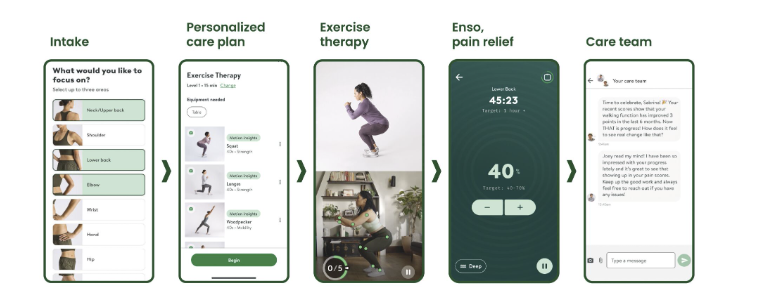

Pain management is a massive pain point (ha!) and MSK is one of the largest specialties in the U.S. Treating musculoskeletal (MSK) conditions, especially chronic ones, is costly and inefficient - often even unnecessary or preventable for many patients dealing with constant pain. Having broken my tibia and fibula as a senior in high school, I can personally speak to how so much pain over time affects an individual. It's heartbreaking and debilitating. Soul sapping. But despite all of the pain and surgeries prevalent in the U.S., preventive and proactive care has fallen behind. Physical therapists do a damn fine job. But the experience could improve. For instance, in-person physical therapy (PT) is hard to access given clinician availability, patient time / childcare coordination, and need to travel to a physical clinic location. It can also be expensive. And we want people to receive PT, just like we want people seeing their PCP. When patients adhere to PT more consistently and see through programs to completion, follow-up surgeries or complications typically reduce dramatically. Outcomes improve. Livelihoods are restored. So one answer to our MSK pain problem is to…deliver therapy patients actually stick to, in a convenient and cost-efficient manner. And this challenge is what Hinge - and other virtual / AI care companies - have set out to solve. Hinge's Value Prop. Hinge wants to deliver high quality physical therapy for MSK conditions at scale. They claim to have done just that, asserting their model automates 95% of care delivery through leveraging technology like virtual care and artificial intelligence. Based on external reports and internally conducted Hinge studies, the Hinge model provides similar clinical outcomes to in-person PT. AI-enabled virtual care also saves their customers, employers and payors, money - on average, $2.4k or so. To address the out of pocket cost problem, Hinge doesn't charge any out of pocket costs to members. A single app delivers personalized care plans to members and connects patients with PTs or other care team personnel 24/7. |

Hinge's Customers and TAM. Hinge sells an annual subscription to its customers, and those customers only pay for members who engage with Hinge programming. In 2024, 3.4% of Hinge's member base engaged with Hinge. This dynamic makes Hinge's annual business predictable given advance bookings and deferred revenue, assuming Hinge can properly engage members. Hinge works mostly with self-insured employers, fully insured payors, MA, Medicare, Medicaid, and international markets. Currently Hinge works with 2,250 clients with access to 20 million contracted lives (not all of which are eligible or engage in Hinge services), comprising 42% of Fortune 500 companies (err…so 210 companies? Can't we just say that next time guys?) Hinge claims its current covered lives represents 5% of its TAM, so that implies a covered lives TAM of ~400M folks unless my algebra skills are softening. - Self insured TAM: $10B

- Fully-insured, MA, federal insurance plans TAM: $8B (this segment is an area Hinge is actively looking to diversify its revenue into)

- Medicare and Medicaid: $9B

- International market: undefined opportunity in the S-1

So Hinge and others in the space are reimagining physical therapy, and increasing the scalability of PTs to improve access while reducing MSK utilization. Reducing utilization saves customers money and makes Hinge money. The redefined experience - for all stakeholders - looks something like this:

- "I have to go get PT in person," → "I can access PT whenever I want, 24/7."

- "PT costs a ton," → "PT is free for me."

- "I have to get another surgery for my back," → "I stuck with my PT program and feel much better without surgery."

- "My employees are missing work and it's costing me double - once for their absence, and once in my pocketbook," → "My employees are less likely to be in pain, miss work for surgeries or PT, and I'm saving money."

- "I struggle to get through my daily caseload of patients" → "I have a care team and technology to help me scale my services beyond what I thought was possible."

Does Hinge's model - virtual MSK - work and provide appropriate clinical outcomes? Hinge says yes: - Substantial outcomes: The research related to our programs spans 19 peer-reviewed research articles and studies and outcomes analyses. In 2020, we published a 10,000 member cohort study evaluating the efficacy of our platform for participants with chronic knee and back pain. Participants reported a 68% average improvement in pain and a 58% reduction in depression and anxiety after 12 weeks.

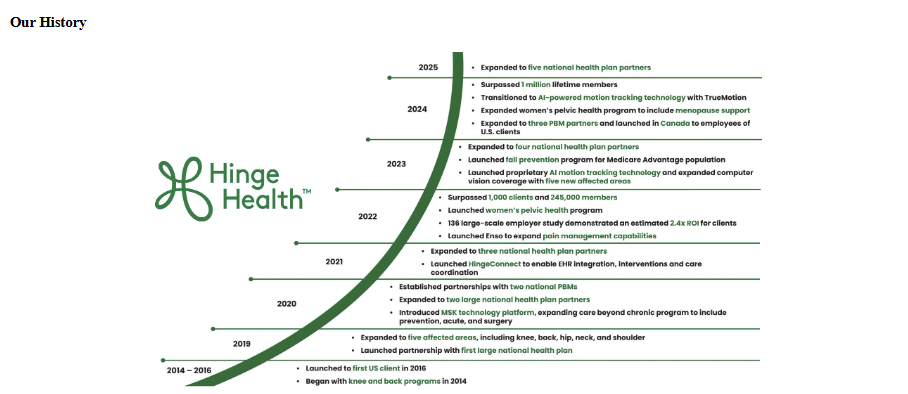

Other notable parts of the Hinge platform include its HingeConnect care coordination, data analytics, and patient personalization and stratification / risk platform to identify potential users and members with high needs, along with TrueMotion, which is Hinge's AI-powered motion tracking technology, and finally Enso, which is Hinge's FDA-approved wearable device. All are synergistic and add value to the Hinge Health offering. - Our proprietary AI-driven database, HingeConnect, helps us identify and target the cost-driving individuals by leveraging a vast array of data, including demographics, comorbidities, exercise forms, and pain scores, as well as EHR data with daily claims feeds across over 750,000 providers

Brief Overview of Hinge's Programs. The full list and description of these programs is on page 149, but here's a brief summary: - Chronic: A comprehensive program for long-term musculoskeletal conditions, offering AI-powered exercise therapy, robust education, and multidisciplinary care team support across multiple body areas.

- Women's Pelvic Health: specialized component of the chronic program focused on common pelvic disorders during pregnancy, postpartum, and menopause

- Acute: short-term program addressing one-time or acute musculoskeletal injuries, providing tailored exercise therapy and care team support

- Surgery / High Risk Member: identify and support members at high risk for surgery, offering education and interventions to help reduce unnecessary procedures

- Pre/post Surgery: guiding members before and after surgery with targeted exercise therapy, education, and recovery support

- Fall prevention: for adults 65 and older that combines exercise, education, and care team guidance to reduce the risk of falling. Launched in 2023

- General prevention: no-cost wellness program offering exercise routines and lifestyle education for members without pressing MSK issues

- Global / International: launched in 2024. Worldwide, hardware-free MSK care program using AI-driven exercise tracking and localized content, aiming to reach more members at a lower cost without dedicated care team support

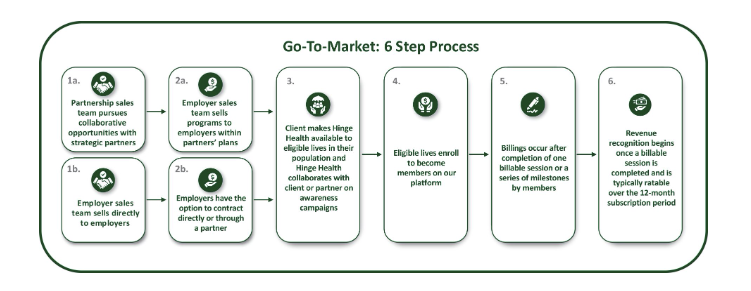

Go to Market and Revenue / Pricing Model. |

Hinge's pricing model and offering to employers is attractive too, leading to shorter sales cycles - 5 months, and up to 12 months for larger enterprise customers. As mentioned customers pay for engaged members - not all covered lives, and virtual MSK in general has moved to a contingency, at-risk pricing model on a portion of Hinge's fees - akin to 'downside' risk. This approach works to close the deal faster, but also could work against Hinge: - The majority of our clients enter into contracts with us through our relationships with health plans. Most of our agreements with health plans are three-year contracts; however, health plans can generally unilaterally terminate their relationship with us pursuant to the terms of their agreements with us or can seek to renegotiate their agreements prior to the end of the contract term. Additionally, our client contracts often include a performance guarantee, which may include engagement thresholds, member reported outcomes, and client return on investment, and, if we are unable to achieve these performance guarantees on a consistent basis, our business, results of operations, and financial condition could be materially adversely affected.

Importantly, because Hinge typically bills through a customer's health plan, Hinge's costs are embedded into the employer's medical spend and NOT a separate wellness / discretionary budget. This billing dynamic alone makes Hinge's relationship stickier and leads to easier collection of payment (assuming the payor cooperates). The dynamic also speeds up the implementation process with a new customer after entering into a new contract. Simple implementations and getting paid on time are key. - In 2023, the vast majority of our contracts were completed via our partners, negating the need for many clients to contract directly with us since many clients can leverage existing contracts through our partners. This is a significant strategic advantage for us as it enables implementation and launch of our platform as quickly as a few weeks after entering into a contract. As a result, most implementations are completed in a 40–100 day period.

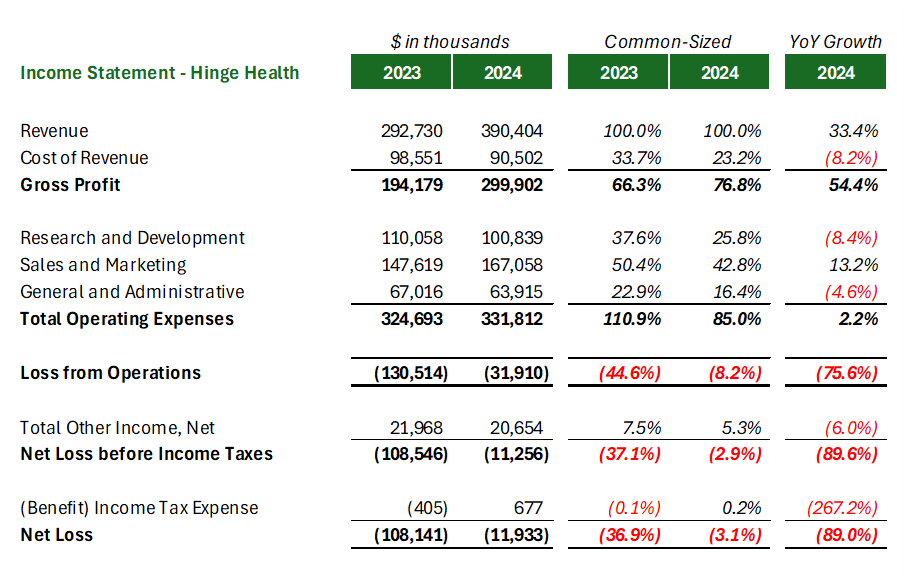

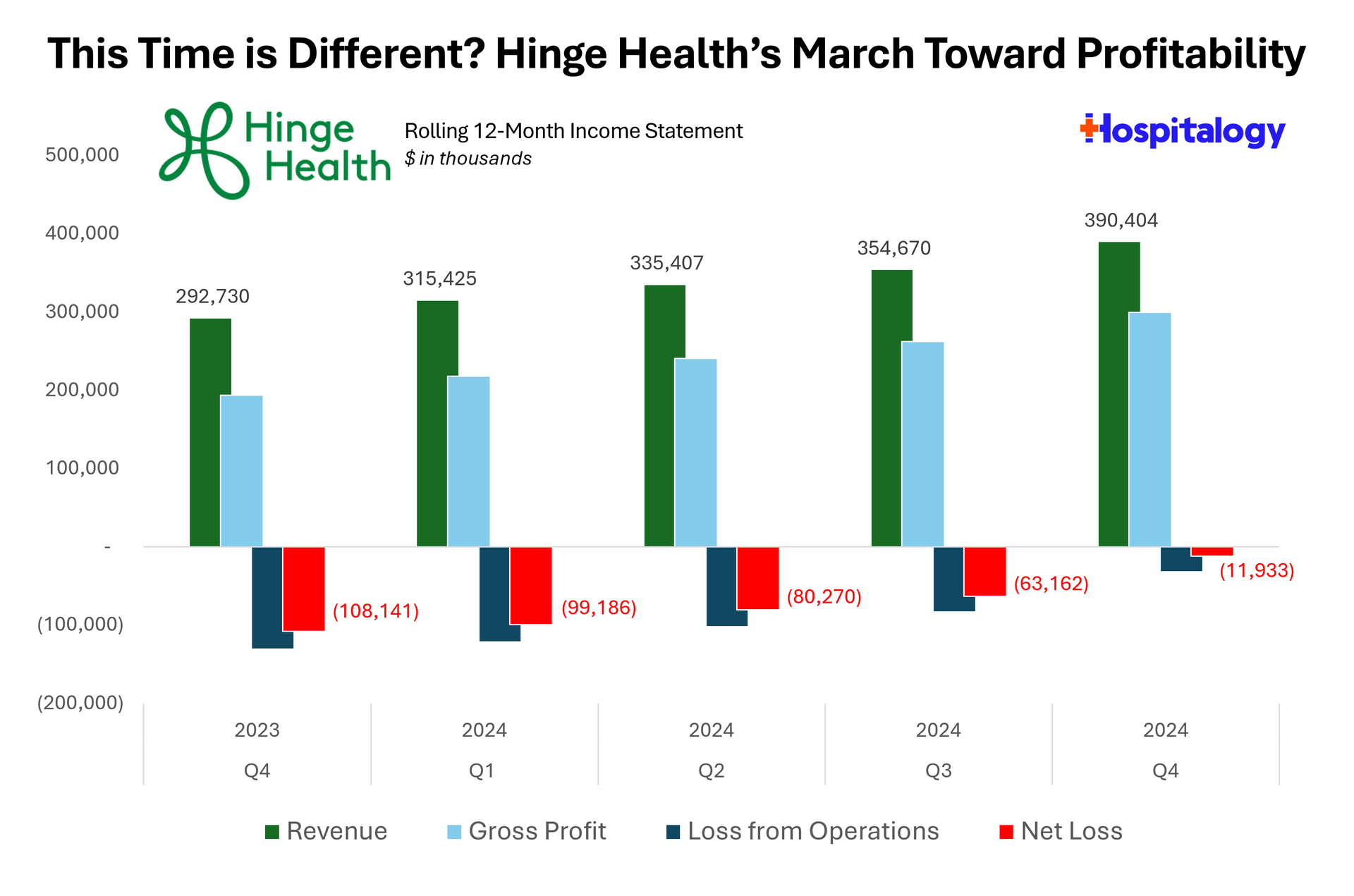

Hinge Health S-1: Financial and Operations Breakdown We can't forget Hinge Health (Hinge) was last valued at $6.2B (granted - back in 2021 when money was free). Valuation is an important factor in all of this and determines Hinge's ultimate invest ability. But also…over $1B raised to date (Hinge has $500M+ on the balance sheet in Cash + equivalents). Keep that in mind as you review these financials. So what does a '$6.2B' health tech company look like? (Note: probably not a $6.2B company for much longer - can't imagine public investors stomaching a 16x trailing multiple in the current market bloodbath conditions) Annual Income Statement. In 2024, Hinge generated $390M in revenue and hit gross margins of 77%. Year over year, Hinge grew revenues by over 33% while improving gross margin, operating margin, and net loss significantly. It's trending toward profitability in the foreseeable future - a believable story investors can probably get behind: |

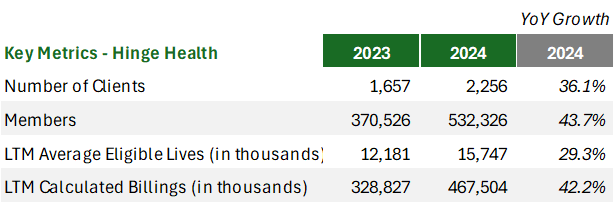

At face value, Hinge's financials are solid when comparing 2023 and 2024, the two years provided in the analysis. Odd they didn't include periods prior to 2023 but we have to work with what we get! Along with net revenue, Hinge wants you to understand another key metric: $468M in calculated billings, which they state is a better way to understand the health of the business given some seasonality and accounting issues around revenue recognition and annual bookings. Calculated billings grew by over 40%, above the 33% revenue figure. Operating Metrics and Footprint. Hinge didn't offer much in terms of operating metrics, but what they did share was impressive. Along with 1,437 total employees at year end, Hinge saw a 36% increase in clients, 44% increase in membership (note: 532k members out of 20 million covered lives - is that good, health tech analysts?): |

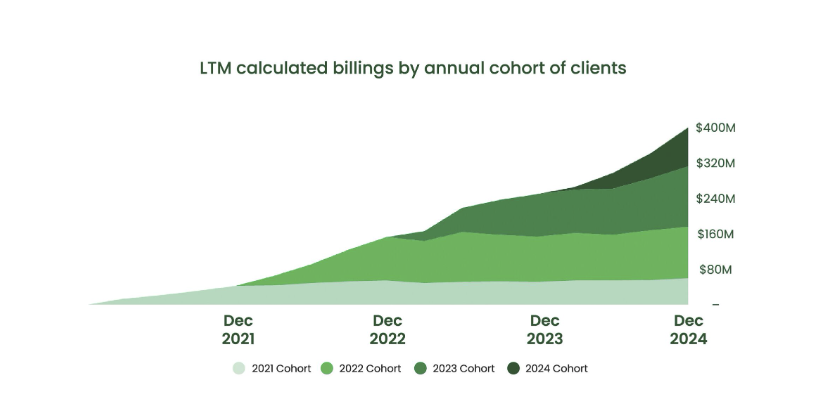

Hinge's overall footprint is solid for the business it is, not the capital it's raised. They work with 50+ payor and PBM partners, all 5 national health plans, and are relatively insulated from customer concentration risk. Hinge lists this concentration as a risk but I'm not so sure. What do you guys think? Health Care Services Corp comprised 17% of Hinge's revenue in 2024 while Elevance was 14% and Aetna hit 11.6%. Still, it's noted several times throughout the S-1 that these contracts are not exclusive and while they're signed for 3 year terms, the payor can terminate them for convenience at any time with notice. That's a pretty notable caveat. Here's a nice look at Hinge's billings by yearly cohort: |

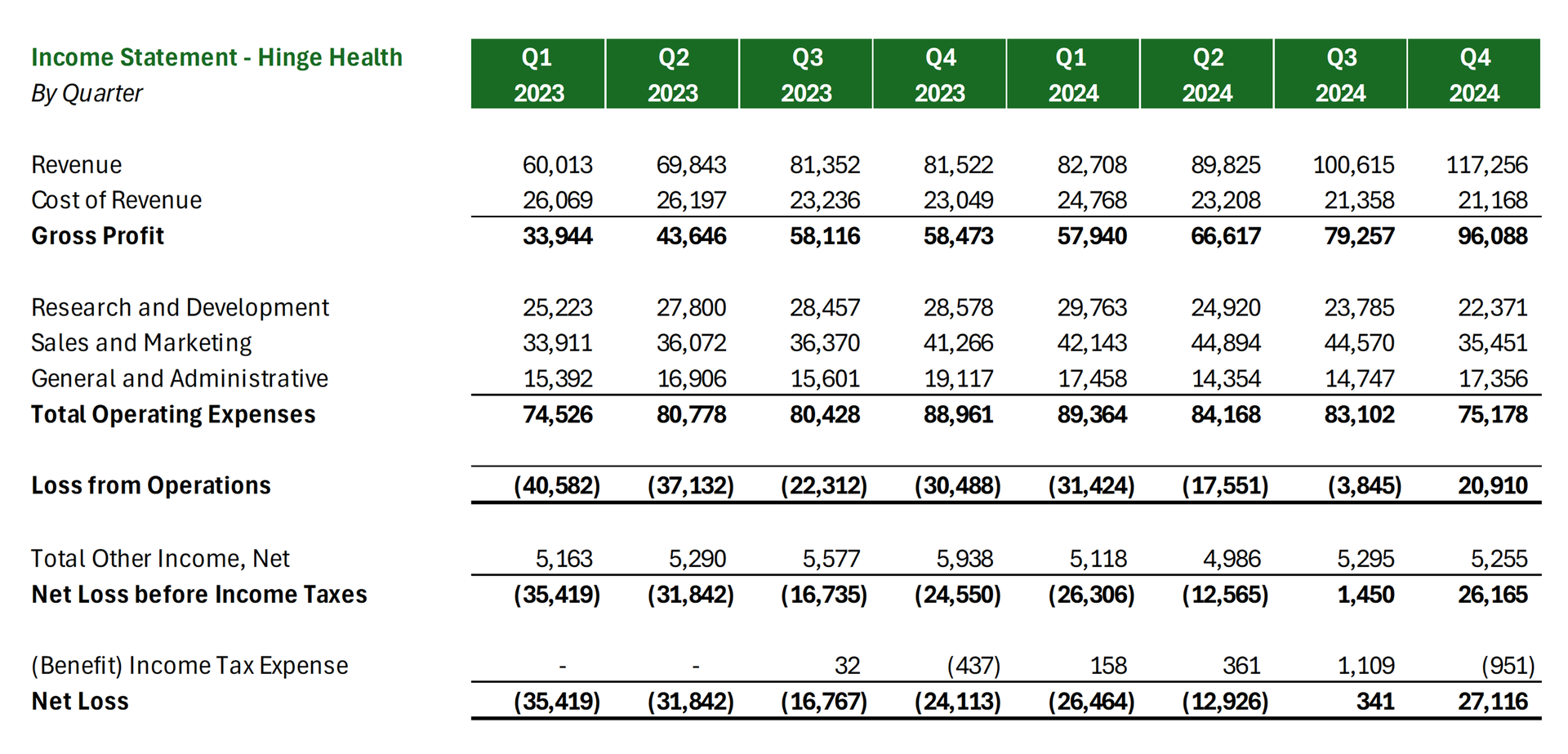

Quarterly Income Statement Analysis. Hinge also provided us with 8 quarters of data (the aforementioned 2 years). Here's a few different ways I sliced the data, first looking at a sequential income statement: |

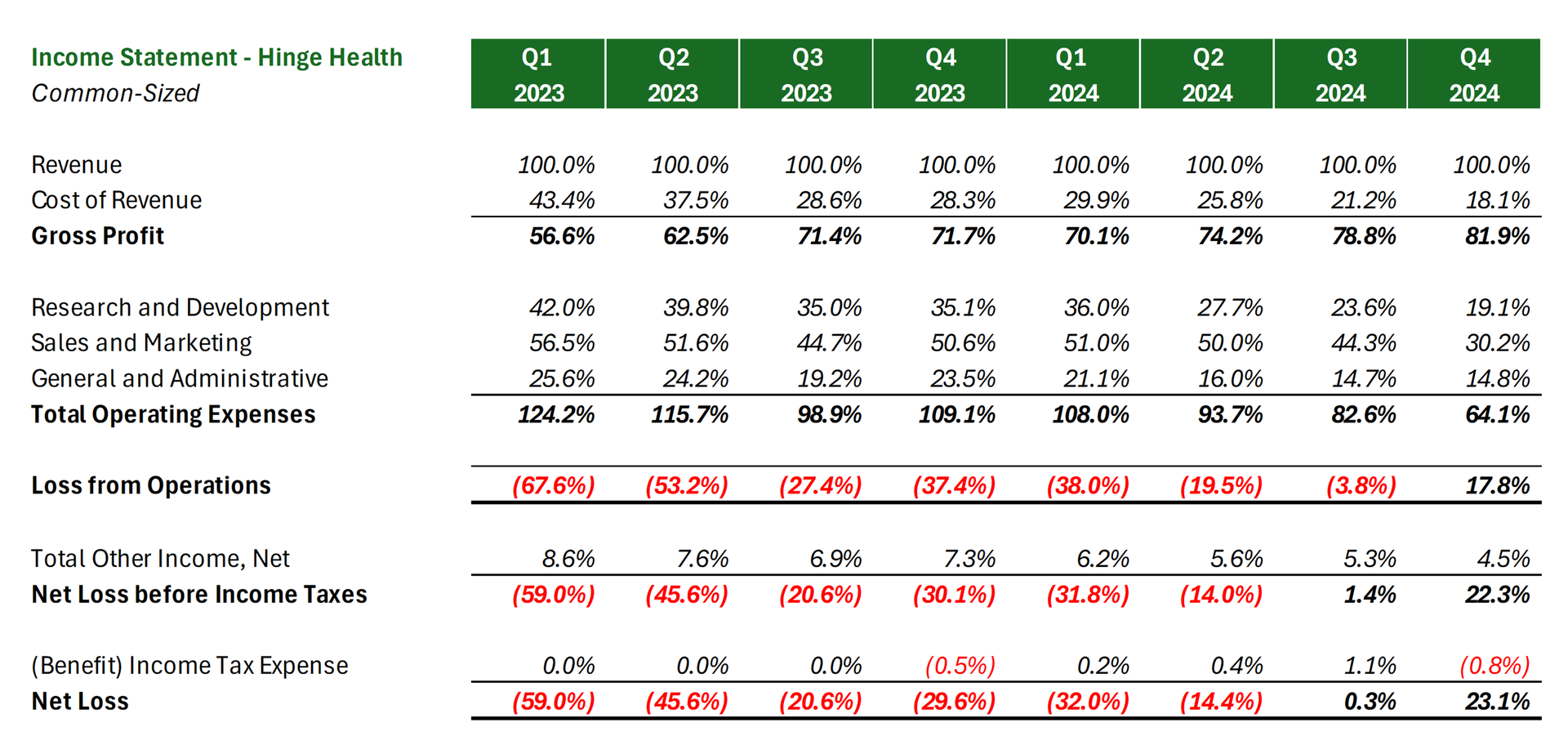

Here's that same view, but common-sized (everything expressed as a percentage of total net revenue). Here you can pretty clearly see the trend toward profitability but also what levers Hinge pulled to reach it - namely, cutting sales & marketing spend, R&D then some COGS. Still, a good point made on X was around Hinge's level of sales & marketing spend (50%+ in many quarters) relative to its overall revenue growth. Is that level of spend efficient / sustainable?: |

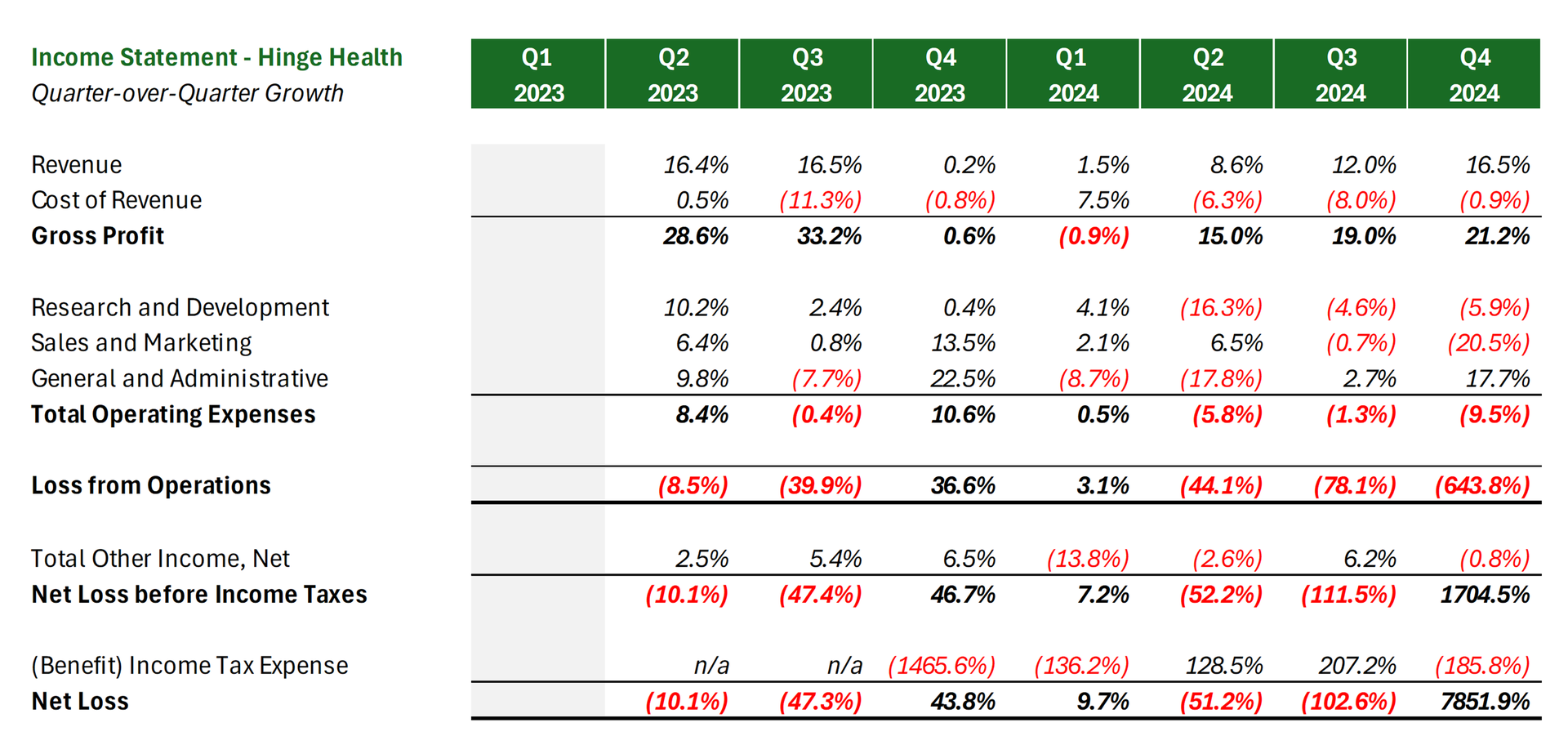

Here are growth rates quarter-over-quarter. From Q2 '24 to Q4 '24, Hinge grew revenues 15%+: |

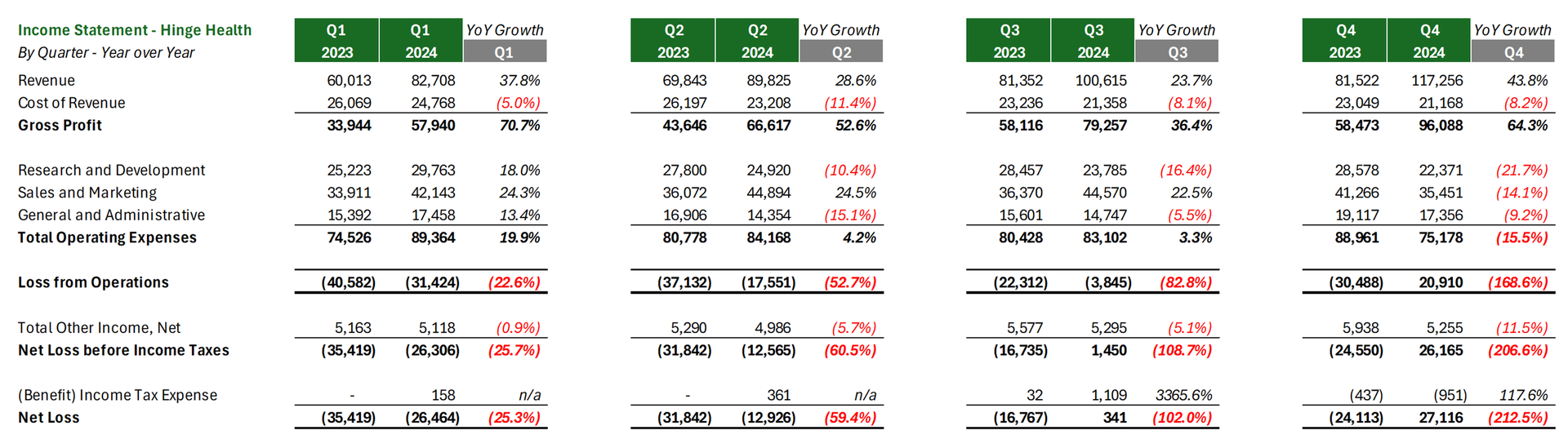

And finally, here's the year-over-year view. Probably the best one to look at change over time when observing comparable periods. Look at all that red in Q4 on the expense side, prepping for this IPO!! That's some serious expense lever pulling to essentially get Hinge to breakeven: |

On the cash flow front, Hinge generated $49M in operating cash flow and holds over $466M in cash and marketable securities. So…the financials are…in a pretty good spot fam. And I mean, this is health tech we're talking about too.

Here's a better visual of that improving profitability trend. Look at that step-wise function up and to the right when you analyze the 12-month rolling income statement (i.e., adding and subtracting one quarter at a time): |

My only problem - and what I imagine will be THE problem when it comes to IPO and near-term success is…valuation. What will public markets value Hinge at? What level will Hinge try to price its IPO at? Let's at least TRY to be reasonable. This is the end of part 1. Part 2 will dive into some more commentary, odds and ends, and bull/bear case. But let me know what your impression of Hinge is compared to its peers, the space in general, and what you've read from me. I'm VERY curious. Til next time! |

|

|

SPONSORED BY NABLA In case you missed it, Nabla just dropped Nabla Dictation, redefining AI assistance for clinicians.

Why choose between Dictate, Command, or Ambient AI when you can have all three? Nabla's vision: an AI that listens, understands, and acts like a silent, intuitive partner in your workflow.

Engineered for speed and simplicity, Nabla Dictation really does fit into any workflow, across 55+ specialties. It pairs with all EHRs and any microphone, too.

Clinicians deserve the GOAT of dictation and Nabla just delivered. 🐐

|

|

|

Random personal anecdotes and musings from me |

See you in Austin at Driftwood! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 42,000 executives and healthcare decision-makers. |

I'm building an exclusive community for VPs, Directors, and above working at health systems in corporate strategy / finance |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments