Happy Tuesday, Hospitalogists! Today's newsletter is a comprehensive overview of hospital Q4 and 2024 earnings season - what they're thinking about, parallels and key themes from earnings calls, comparisons of how they performed in 2024, and 2025 outlook. Finally, for any folks in Austin or at SXSW: don't forget about my happy hour coming up this Tuesday in Austin with Lance Armstrong, Ben Freeberg, and more healthcare folks! All are welcome - register here. Feel free to bring healthcare friends. |

Was this email forwarded to you? |

|

|

Hospital Q4 Earnings Season Breakdown |

The most important news from the week |

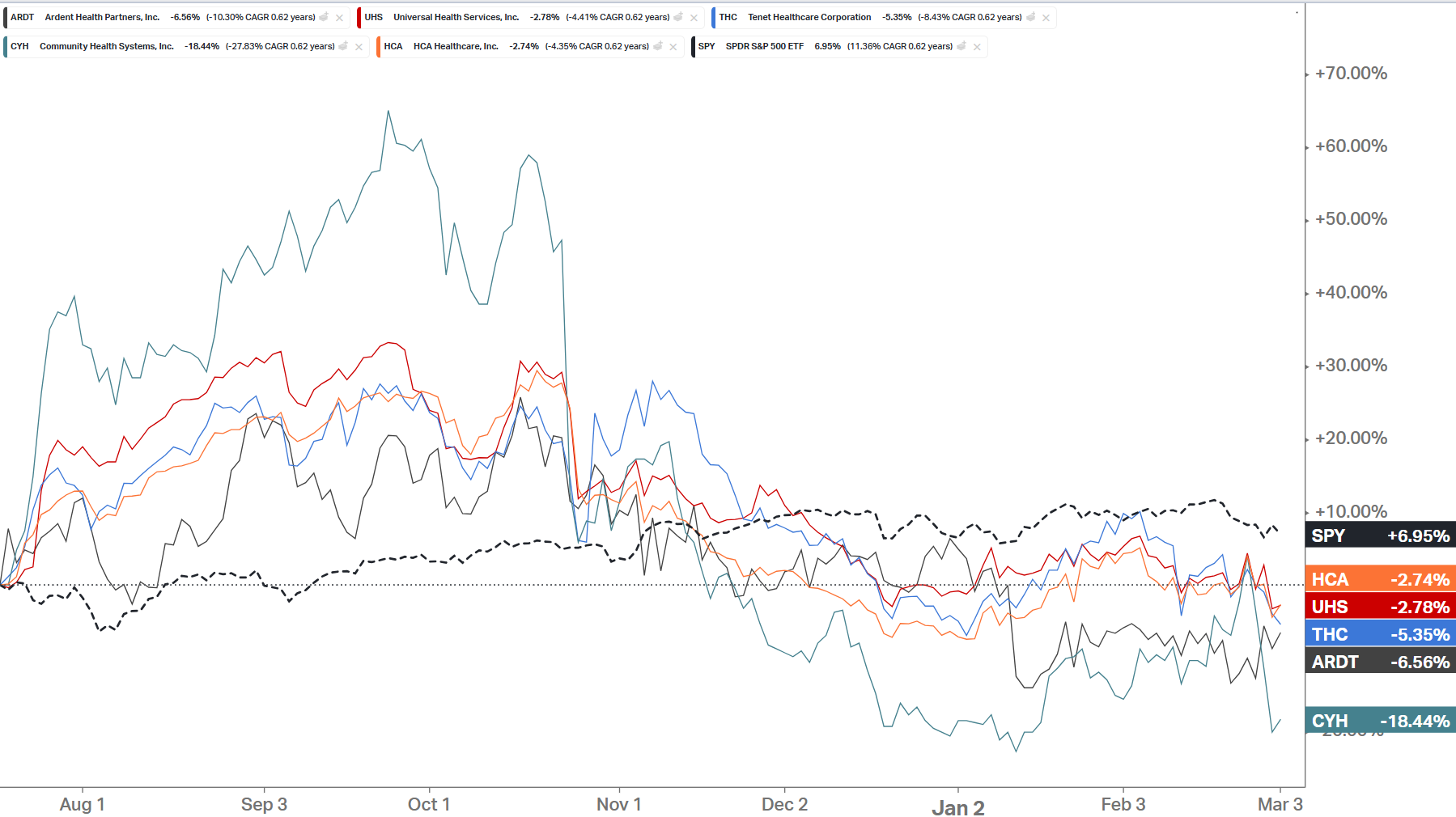

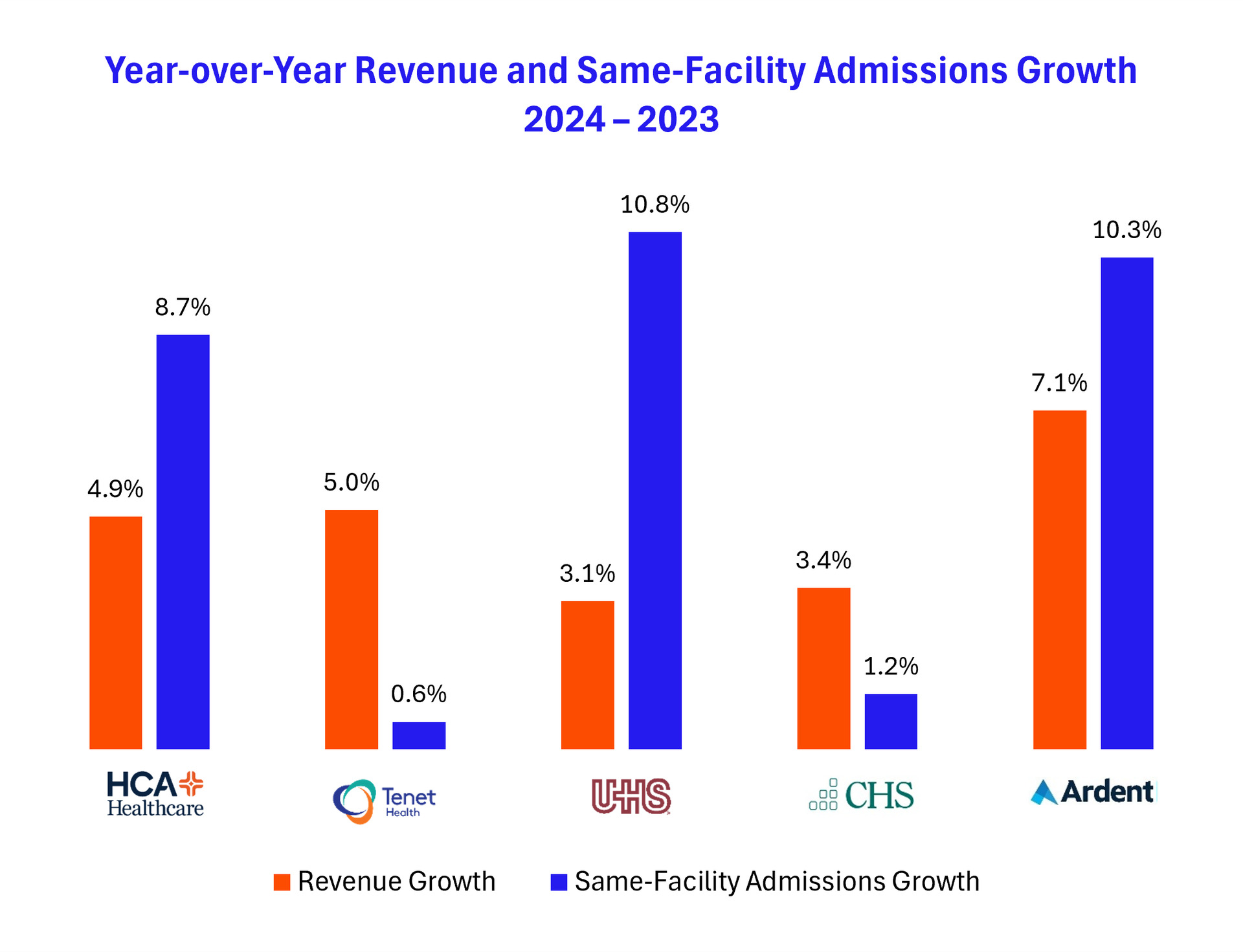

TL;DR - Public Hospital Operator Themes from Q4 Earnings Season |

Volume & Utilization: All five reported stable-to-strong acute care inpatient admission growth (2- 4% range). Outpatient expansions, particularly ASC volumes, are a unifying theme, with Tenet's USPI leading in specialty ASC expansions as health systems look to build out ambulatory footprints. Revenue & Payor Mix: Each benefited from commercial rate bumps (3–5%). Exchange enrollment continued pushing up commercial-like volumes, but caution remains on the policy front. Medicaid DPP or supplemental revenues created one-time lifts for each operator. Side note - is it payor or payer?? I've always used payor...so sue me. Expenses & Margin: Labor cost moderation helped all five expand or maintain margins. Physician fee inflation remains a watch item for CHS, Ardent, HCA. UHS had a notable malpractice reserve spike, while Tenet is seeing a big margin tailwind from its focus on ASCs. Capital Allocation: CHS, Tenet each sold multiple hospitals; CHS plans more divestitures in 2025. HCA plans to invest heavily in ORGANIC bed expansions; Tenet will invest into USPI growth - ~$300M. Guidance: Steady 2025 growth in volumes, revenue, and EBITDA across the board, with some inherent uncertainties around DPP approvals, potential site-neutral legislation, and exchange subsidy continuity. It's clear we're past peak hospital valuation which hit a high point in October. Keep in mind valuations are always forward looking: |

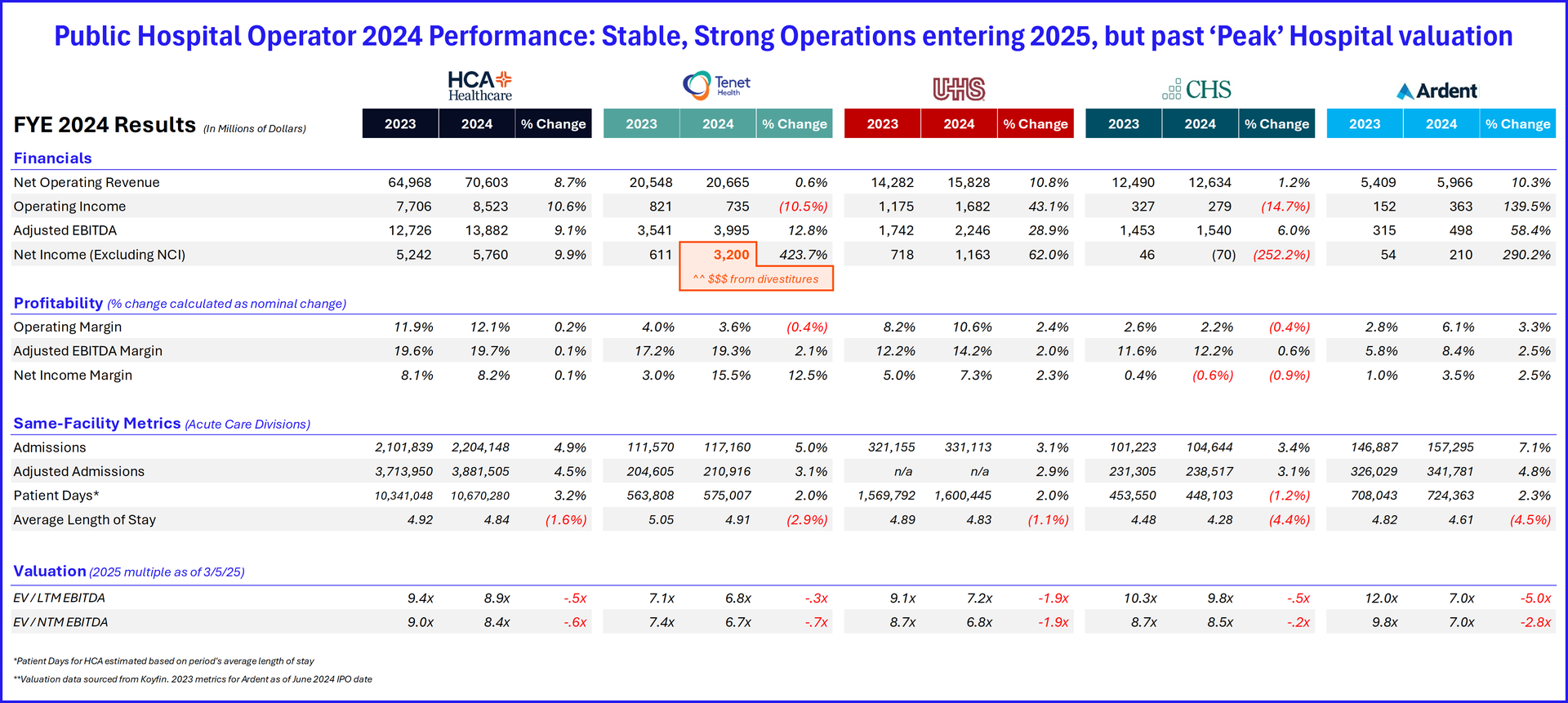

Key 2024 Comparative Results Across the board we saw strong performance for HCA, Tenet, UHS, and Ardent. CHS continues to trudge along behind the pack. Declining length of stay, strong same-store admissions, strong acuity, and rising exchange volumes in 2024 bolstered financial performance and contributed to nice recovery for most operators. |

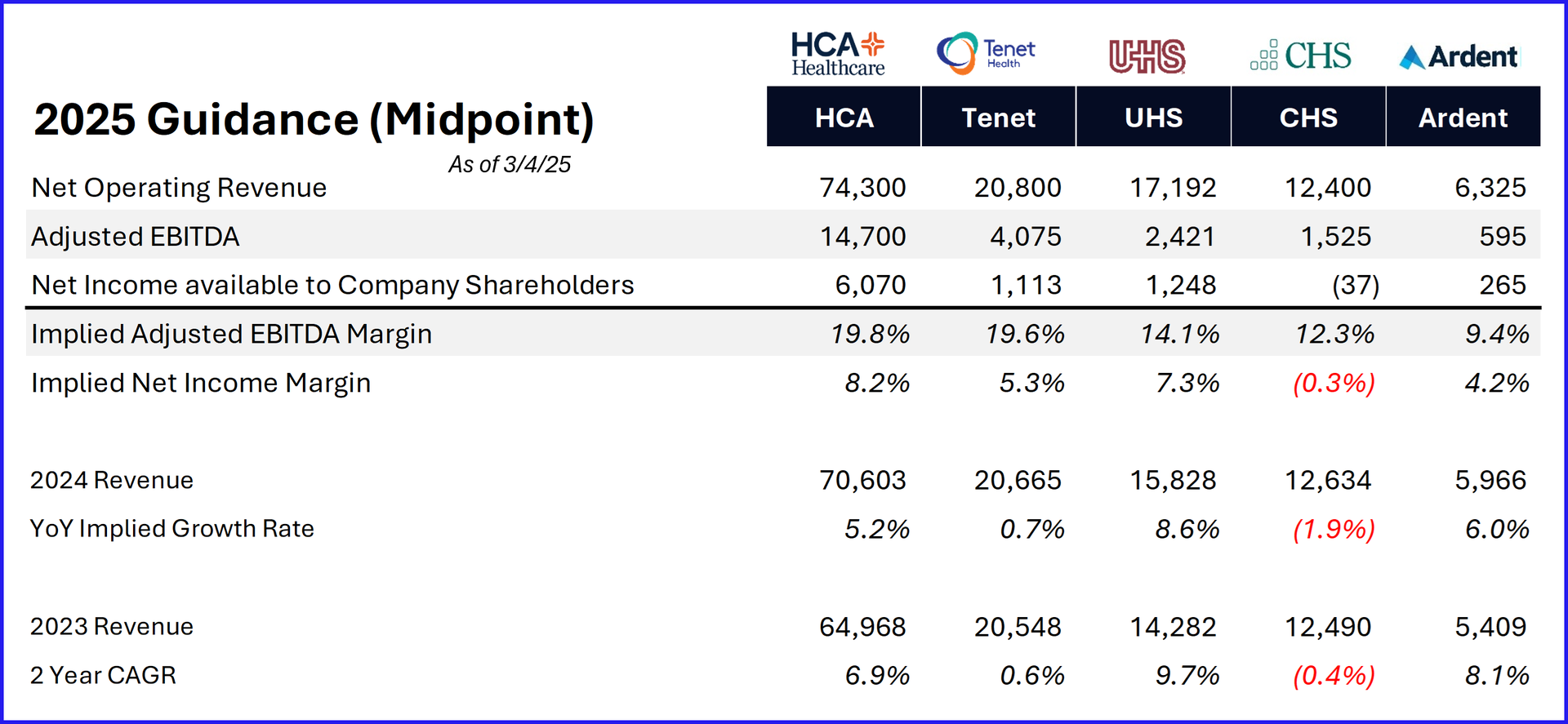

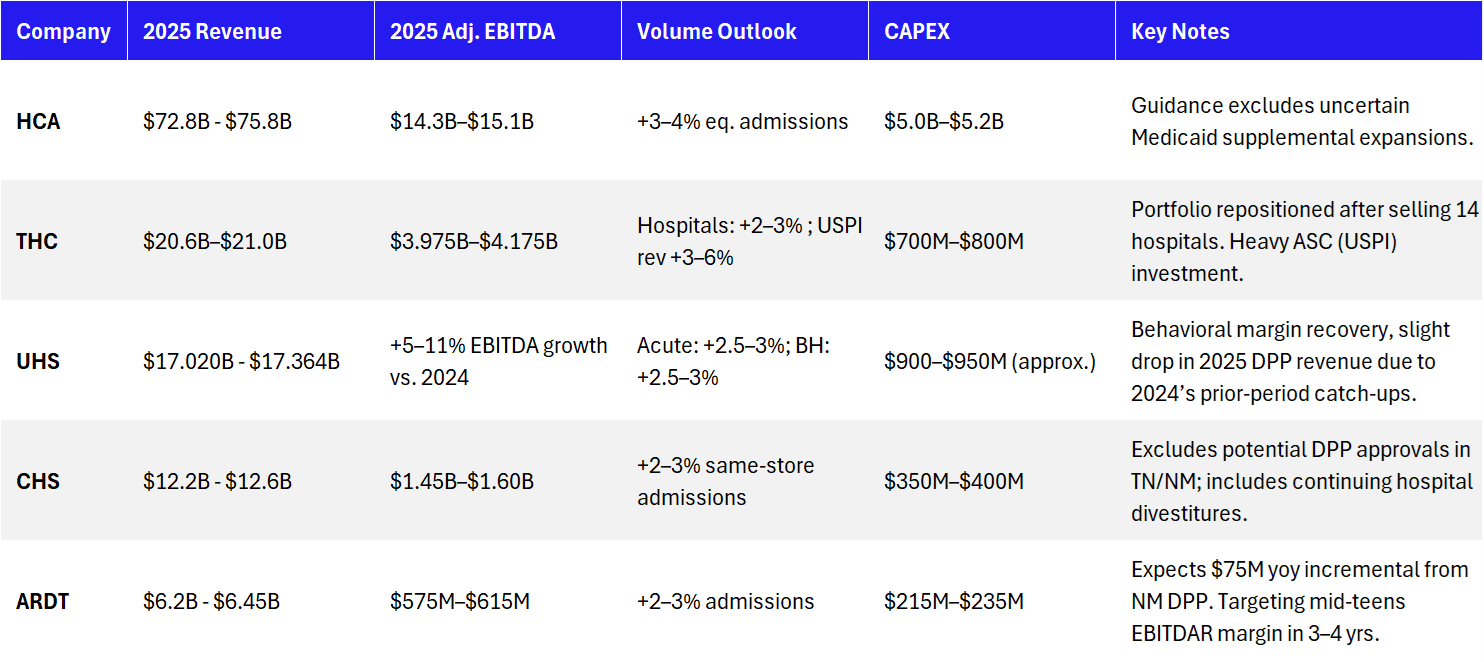

2025 Hospital Operators: Guidance Highlights |

Major Trends Across Public Hospital Operators Volume & Utilization - Broadly Positive Inpatient Demand: Most operators reported growth in same-store admissions (ranging ~2–4%+). Elective procedures and higher-acuity surgical volumes (e.g., orthopedics, neurosurgery, cardiology) drove much of the incremental demand.

- Ambulatory & Outpatient Expansion: Every company highlighted strong or growing ASC volume. Ardent, CHS, Tenet, and HCA emphasized ambulatory expansions, while UHS likewise noted robust volumes in acute hospitals plus steady behavioral health admissions.

- Acuity & Mix: Several operators (Tenet, CHS, HCA) mentioned rising patient acuity or shifts toward higher-margin surgical lines. However, some noted mild softness in outpatient surgeries among lower-paying segments (e.g., Medicaid/uninsured).

Revenue Growth & Payer Mix - Mid-Single-Digit to Low-Double-Digit Growth: Revenue growth was generally in the 5–10% range, aided by rate increases, improving commercial mix, and in some cases state Medicaid supplemental payments.

|

- Commercial Rate Increases: Typical negotiated rate bumps ran ~3–5%. Higher inflation pressures over the past 18 months have led payers to offer slightly higher-than-historical increases.

- Medicaid Supplemental Programs: CHS, Ardent, Tenet, and HCA each recognized notable incremental revenue from various Directed Payment Programs (DPPs); UHS likewise benefits from state-specific programs. Many 2024 numbers included retroactive or catch-up payments. Looking ahead, these remain a swing factor in 2025 guidance.

- Exchange Volumes: HCA, Tenet, and others have seen material growth in exchange admissions/revenue. Of course, concerns exist about 2026 and beyond if enhanced subsidies expire. Concerns also exist around Medicaid cuts. Lots of policy uncertainty that are net negative to hospitals with the new administration (340B, Medicaid, supplemental payment dollars, future of ACA subsidies)

Expenses & Margin - Generally Improving Labor Costs: All five reported a drop in premium (contract) labor spend from 2022–2023 peaks. Wage inflation is "stabilizing," though still above pre-pandemic norms. In general contract labor is at a low point post-Covid among major public operators.

- Adjusted EBITDA Margin: Most showed margin improvement year over year. Tenet and Ardent reported some of the largest expansions (helped by divestitures and fast-growing ambulatory segments), CHS improved modestly, HCA held steady (+10 bps full year), UHS likewise saw expansions in both acute and behavioral.

- Physician Fees: Some (CHS, Ardent, HCA) noted continuing upward pressure on hospital-based physician fees in areas like anesthesia, radiology, or ER coverage—but at a moderating pace. Still a concern in today's environment. Physician pay will continue to be a focal point

- Keep an eye on medical supplies cost with tariffs: Definitely potential here to see an uptick stemming from tariffs. Hospital operators today don't seem too concerned and appear to have mitigation strategies in place for their procurement.

Capital Allocation - ASC & Outpatient Investments: Tenet (via USPI) remains the largest ASC operator; Ardent, CHS, HCA all investing in de novo outpatient sites, urgent care, and/or ASC expansions.

- Deleveraging & Divestitures: As I've mentioned before on Hospitalogy, and even among many nonprofit health systems, 2024 was a year of portfolio realignment. Both CHS and Tenet sold multiple hospitals in 2024; proceeds used to reduce debt. Ardent improved leverage to ~2.9×. CHS has plans for additional asset sales in 2025. UHS's leverage remains comfortably below 3×; HCA uses robust free cash flow for share buybacks and expansions.

- Share Repurchases: Tenet and HCA are especially active (both in the $5–6B range in 2024). UHS also prioritizes buybacks (~$600M). CHS and Ardent have limited or no share repurchase activity, focusing on debt reduction.

Outlook & Guidance (2025) - Steady Volume Growth: Most project 2–3% (or slightly higher) inpatient admissions growth, along with continued expansions in ASC/outpatient.

- Revenue & EBITDA: Operators generally guide for mid-single to high-single-digit revenue growth, with incremental margin improvement from labor cost control and higher commercial rates. Many are excluding unapproved Medicaid DPP dollars from guidance, so actual results could exceed.

- Policy & Regulatory Watch: Potential site-neutral payment reforms, renewed or delayed Medicaid DPP approvals, and exchange subsidy uncertainties are common themes. No major immediate policy changes are fully baked in.

Analyst Q&A - what are analysts thinking about? - Top Questions: (1) the sustainability and magnitude of Medicaid DPP payments; (2) labor cost trajectory (contract labor, physician subsidies); (3) capital allocation priorities (ASCs vs. share buybacks vs. M&A); (4) volume guidance and service line mix shifts; (5) any impact from site-neutral proposals or future exchange subsidy changes.

That's it for this one! Read the online version for a more robust breakdown by operator. |

|

|

SPONSORED BY SMARTERDX The human eye can only catch so much. SmarterPrebill from SmarterDx was born out of a problem two physician-data scientists saw firsthand: Second-level chart reviews are essential, but sifting through ~30K data points per chart made catching every missing or incorrect diagnosis impossible.

That's where SmarterPrebill comes in: It unleashes 2,200+ proprietary algorithms on 100% of charts to highlight revenue, quality, and compliance opportunities.

The result? Fewer billing mistakes, better care, and major revenue growth—with a 5:1 ROI from Day 1. That's an average of $2M annually in new revenue per 10K patient discharges, and no upfront costs. Ready to rethink chart reviews? Learn more. |

|

|

Random personal anecdotes and musings from me |

A friend of mine Casey recently launched his own fine art portfolio and is trying to break into the artist scene - he's actually incredibly talented. But you know how the whole starving artist thing goes, ya know? Anyway, if you're local to Dallas or if you're looking for some really cool artwork ranging from famous golf holes to skylines, please give his work a look! Here's the link to his website, and sign up for his newsletter while you're at it. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. Don't forget about the SXSW happy hour next week. Join my Hospitalogy Membership! If you're a VP or Director working in strategy or corporate development at a hospital, health system or provider organization, you will get a lot of value out of my community as I purpose-build the content, fireside chats, and conversations for this group. Join for free today. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 41,300 executives and healthcare decision-makers. |

I'm building an exclusive community for healthcare corporate development and strategy professionals. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments