PARTNERED WITH  |

|

|

Happy Tuesday, Hospitalogists! You should find today's send concise, yet information dense. But more importantly...who ya got at Royal Portrush this weekend? Let's dive in. |

Was this email forwarded to you? |

|

|

SPONSORED BY NAVINA With the latest news out of CMS, it's no secret health systems are under mounting pressure. Juggling financial constraints between labor and reimbursement squeezes; Shifting VBC regulations with expanded audits; and Rising administrative demands on clinical teams. In 2025, health systems NEED an AI strategy, and having AI partners who actually work as partners for your organization is a huge priority for all care delivery organizations. It's time to put AI to work where it truly drives impact: reducing the burden on care teams, improving outcomes, and strengthening financial performance.

On July 17 at 12 PM ET, join Navina and Bright Spots in Healthcare for a live webinar exploring how high-performing health systems are leveraging AI - talking about actual, tangible takeaways for using AI in value-based care. Hear from leaders at Atlantic Health System, Intermountain Health, and more as they share real-world strategies to streamline workflows, support coordinated care, and boost ROI on VBC programs.

|

|

|

A slew of healthcare resources to make your strategy team look good |

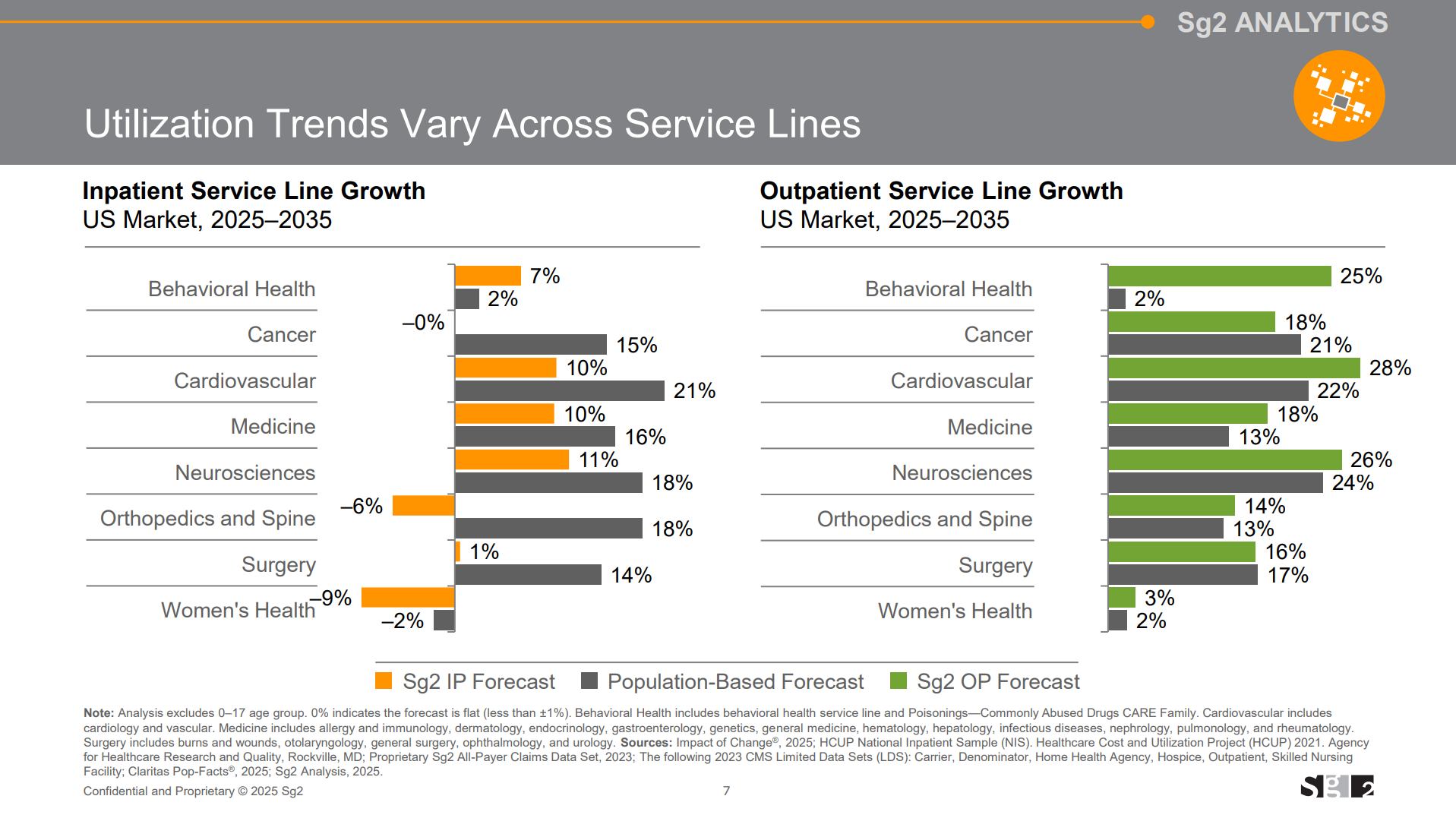

I've seen a spattering of presentations, research reports, and benchmarking data hitting my feed that you might find useful in your day to day. Let's dive in with some quick highlights from each: Vizient's 10-year utilization projections for anticipated shifts in site of care delivery. Over the next 10 years the firm expects the following shifts in utilization:

- Outpatient and oncology volumes to grow by 18% respectively with a 20% bump in outpatient surgeries;

- CV, oncology, neuro, and behavioral will be the main specialty volume drivers over the coming decades as ortho continues a solid, yet decelerating trajectory;

- Inpatient to grow by 5% and including an expected headwind in GLP-1s on diabetes volumes;

- 31% growth in post-acute care (home health, SNF, IRF, LTACH, IPF, behavioral, PT, home care, etc.) with an expected emphasis on the growth of home health

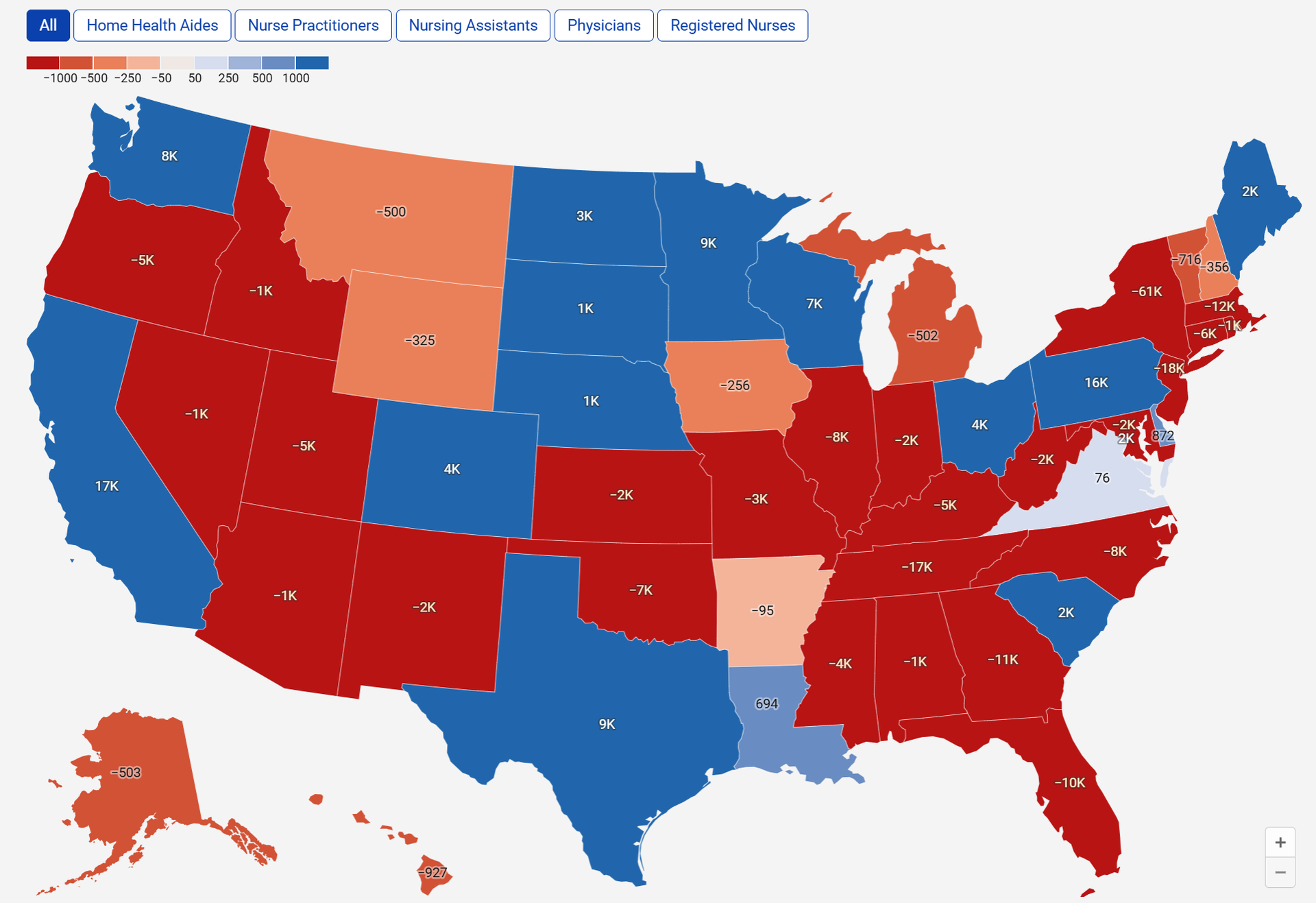

Mercer's Future of the Labor Force annual overview including state-by-state projections of surpluses and deficits for the major healthcare labor force participants |

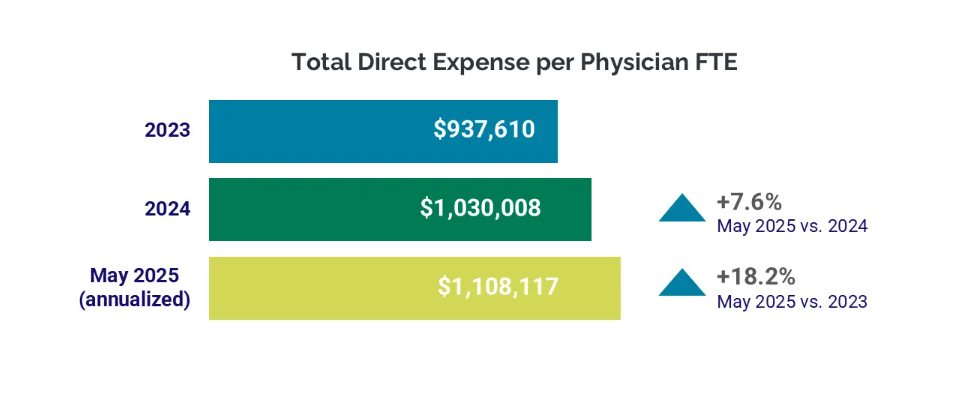

Ziegler's Part 5 of its digital health and AI series - an incredible cross-sector overview of current happenings across healthcare and AI. Though it looks like the PDF needs to be printed on landscape on certain pages - at least for me, the graphics are cut off. Still, great research report to dive into to get caught up to speed covering innovation across the industry. Weaver's newly published Health Care Valuation Knowledge Center covering executive summary level valuation implications for ongoing healthcare M&A and other happenings along with key reimbursement and regulatory changes. The latest hospital utilization and operating margin benchmarks from Strata included notable analysis on physician comp, subsidy, and productivity: - The level of investment required to support physician practice operations continued to climb nationwide, driven by growing expenses. In May (annualized), the median investment per physician full-time equivalent (FTE) was $332,512. This marked a 4.7% increase compared to 2024 and a 19.2% increase compared to 2023.

- Rising expenses contributed to higher investment levels. The median total expense per physician FTE was $1.1 million for May annualized, a 7.6% increase compared to 2024 and an 18.2% increase from 2023.

- Physician [professional] revenues continued to grow in May, with the annualized median NPSR per physician full-time equivalent (FTE) reaching $767,067. This represents a 5.6% increase compared to 2024 and a 17.8% increase compared to 2023.

- Physician productivity also improved…wRVUs per FTE for the month were 6,237.64 — up 4.5% YOY and 11.7% compared to 2023.

|

Sullivan Cotter released its 2025 physician compensation and workforce productivity surveys for those of you with access to that information. MGMA also released its survey data in early June. |

By the way, if you're in enterprise strategy, corpdev, finance, or operations functions for health systems, I drop resources like these over in my community's content library all the time. Check it out by applying here. |

|

|

THE WEEKLY EXECUTIVE SUMMARY |

Notable moves, policies, and strategies |

CMS proposed some interesting things to physician reimbursement, including a crackdown on skin substitute payments, bumping the conversion factor up by 3.83%, and tacking on a mandatory payment model - the Ambulatory Specialty Model - for Medicare beneficiaries with heart failure and low back pain, slated to begin in 2027 if finalized. The TL;DR on all of this is that CMS is looking to leverage data and current trends in healthcare in an attempt to establish more accurate payment methodologies in the future. - Also noteworthy in the proposal was some language around site of service payment differentials (site neutral payments), the evolution of physician practices, and making certain COVID era reforms permanent:

- CMS is proposing to reduce payment differentials for physicians across settings of care by leveraging hospital data to calculate more accurate payment rates for certain services and better accounting for increased efficiencies in procedures and tests.

- we are proposing significant updates to our PE methodology to better reflect current clinical practice. Specifically, we are proposing to recognize greater indirect costs for practitioners in office-based settings compared to facility settings. The original allocation methodologies assumed physicians maintained separate practice locations even if they furnished some care in hospitals. Since the methodologies were established decades ago, there has been a steady decline in the number of physicians working in private practice, with a corresponding rise in physician employment by hospitals and health systems. Therefore, we believe that the allocation of indirect costs for PE RVUs in the facility setting at the same rate as the non-facility setting may no longer reflect contemporary clinical practice.

- We are also proposing to utilize data from auditable, routinely updated hospital data (i.e., from the Medicare Outpatient Prospective Payment System (OPPS)) to set relative rates and inform our costs assumptions for some technical services paid under PFS. For CY 2026, we are proposing to use this data in setting rates for radiation treatment services, and for some remote monitoring services. This approach promotes price transparency across settings, offers more predictable rate setting outcomes, and limits the influence of limited survey data.

- To ensure that Medicare recognizes innovations in medical care, CMS is also proposing…to simplify the process for making services available by telehealth. CMS is also proposing to broaden its payment policies for digital mental health treatment devices to make more options available to patients.

CMS also released its OPPS proposed rule for 2026. Highlights include a 2.4% pay bump (including ASCs) and a phase-out of the inpatient-only list, giving physicians more agency about site of service and which will serve to speed up outpatient migration. The Ohio AG conditionally approved the sale of Summa Health to HATCo with a few extra contingencies attached to the deal. I wonder if Jeff Barge is happy with the result. I can appreciate the activism for the community. Humana became the first insurer to integrate health plan information within Epic MyChart. Speaking of Humana, its CenterWell subsidiary bought The Villages Health out of bankruptcy - after the firm found Medicare billing discrepancies - in a 'stalking horse' bid structure (new term for me, finance aficionados). Humana adds ~55k patients through the deal. UnitedHealth stays in the limelight as journalists and lawmakers give the organization fits in 2025. The NY Times is hard at work covering the healthcare behemoth's PR damage control gone awry. Then Bloomberg noted that UHG divested some of its assets trying to spin this up as some provocative reporting when really it seems like business as usual for an org of this size. I'll let you be the judge. Nabla and Navina, two leading AI-powered clinical platforms, announced a strategic partnership to integrate and combine Navina's clinician copilot with Nabla's in-visit ambient documentation, reconciling historical patient records with live patient dialogue. It's a very notable partnership between two Hospitalogy sponsors (!!) and a consolidation / alignment trend you should expect to continue to see play out as AI-enabled players expand their capabilities into more holistic offerings. Ultra neat. Fabric announced a telehealth partnership with Rush University System for Health. Rush Connect will leverage Fabric's AI assistant and virtual care platform to deliver 'faster and easier patient access to care while giving clinical teams the tools to expand capacity, enhance efficiency, and deliver high-quality care.' |

|

|

Collaborations, launches, and other tidbits to keep on your radar. AI generated summaries. |

- Samsung buys Xealth to expand connected care.

- Amazon restructures healthcare into six pillars.

- Lumeris partners Google Cloud to scale AI primary care.

- Twenty states sue HHS over Medicaid data sharing.

- Aledade names Lalith Vadlamannati CTO.

- Advocate & WellSpan report gains from virtual nursing.

- Carrot unveils Sprints metabolic-fertility program.

- VA plans 30 000-person staff cut by FY 2025.

- Sharp HealthCare axes 315 jobs and trims exec pay.

- Cadence launches AI Proactive Care Engine for Medicare.

- VisiQuate acquires Etyon to boost AI RCM.

- Suki integrates ambient AI notes into MEDITECH.

- New York allows RNs to follow PA protocols.

- AdventHealth rolls out ambient voice tech to ease notes.

- CMS sets $128.90 pay for Eko SENSORA.

- AJMC study finds mature ACO hospitals improving.

- Study shows clinical notes can flag physician fatigue.

- Twenty-two AGs reaffirm EMTALA abortion duty.

- Minnesota nurses plan July 8 ULP strike.

- Novo Nordisk partners WeightWatchers to sell Wegovy at $299.

- Generative AI gains traction across healthcare.

- PHTI to evaluate virtual GI-care solutions.

- Wheel debuts Amazon-powered med fulfillment.

- ASCO teams with Google on AI guidelines assistant.

- Cost Plus & 9amHealth team to cut obesity-drug costs.

- Aligned Marketplace joins Arbital for value-based primary care.

- Lark Health launches AI GLP-1 PA platform.

- Omada Health reports stronger GLP-1 adherence, weight loss.

- Parkview starts Upvia Health management services.

- Humana pilots ambient AI to ease clinician burden.

- Onvida Health adopts Longitude Rx specialty pharmacy model.

|

|

|

My favorite reads & resources from the week |

*This read is brought to you by one of my brand partners who help make this newsletter possible! |

|

| Random personal anecdotes and musings from me |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 44,000+ executives and healthcare decision-makers. |

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments