PARTNERED WITH  |

|

|

Happy Tuesday Hospitalogists!

Following up Tenet, as is customary practice for Hospitalogists, I now bring you HCA's Q2 followed up by a comparative analysis of all four comparable publicly traded hospital operators on Thursday.

Let's dive in! Also - if you could shoot this to a colleague or friend to subscribe - please support me by doing so! |

Was this email forwarded to you? |

|

|

SPONSORED BY CEDAR The coverage crisis is coming — and it's closer than you think. Starting in late 2025, Medicaid and ACA cuts tied to the One Big Beautiful Bill are expected to leave millions uninsured, and add $434B+ in uncompensated care costs over the next decade. Waiting to act isn't an option. A new policy brief from Cedar lays out what's ahead and what finance leaders can do now to mitigate impact. Backed by billions of patient data points and more than a decade of industry partnerships, the brief outlines: What healthcare leaders need to know now about the OBBB Ways to get ahead of Medicaid and ACA reforms How to implement intelligent financial navigation to protect your mission and margin Download your free copy today for concrete strategies to guide your team through these policy changes.

|

|

|

The most important news from the week |

HCA's Q2 2025: Business as Usual in a Strong, Stable Hospital Operating Environment |

(p.s. - how do you like the new one-pager format?) |

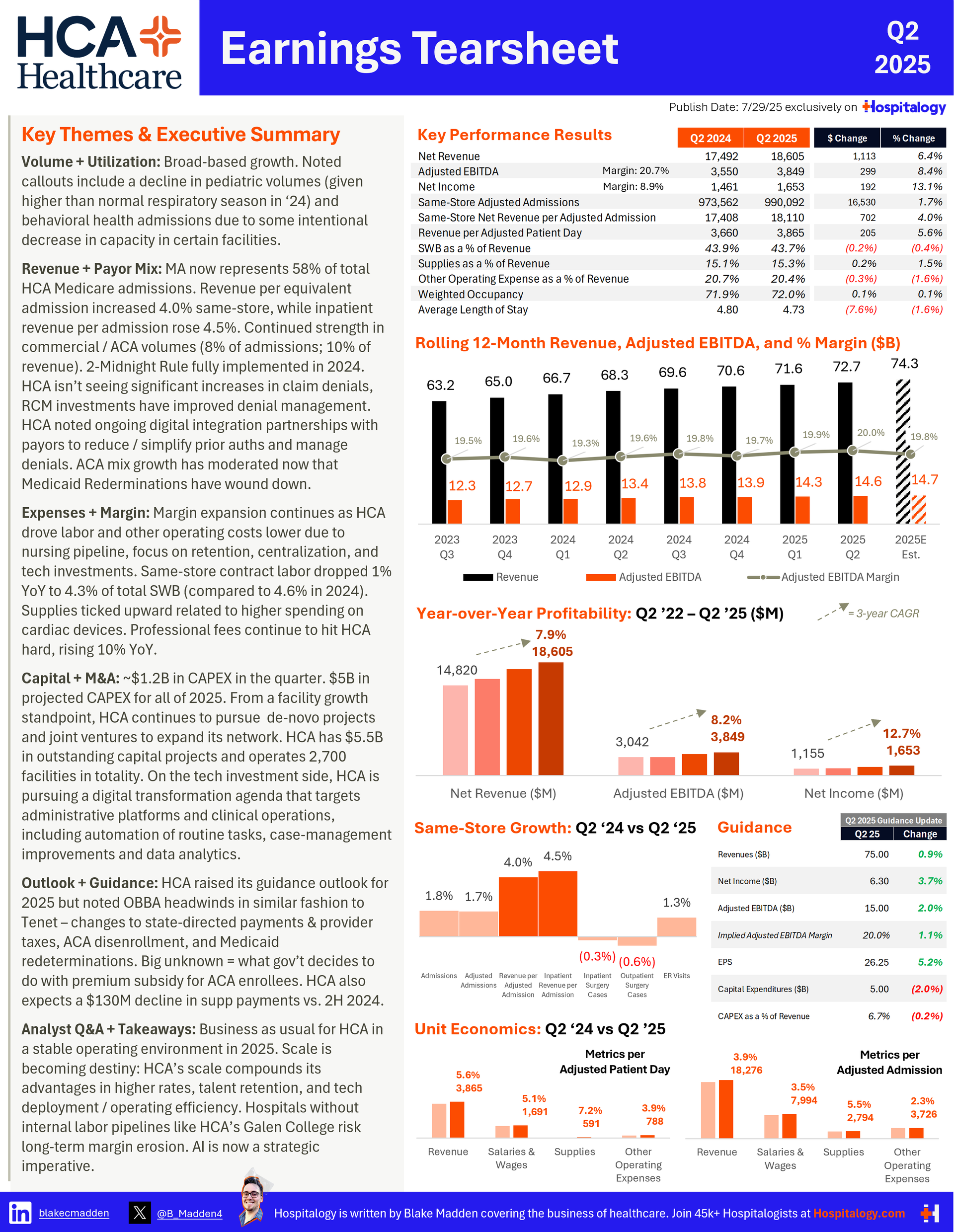

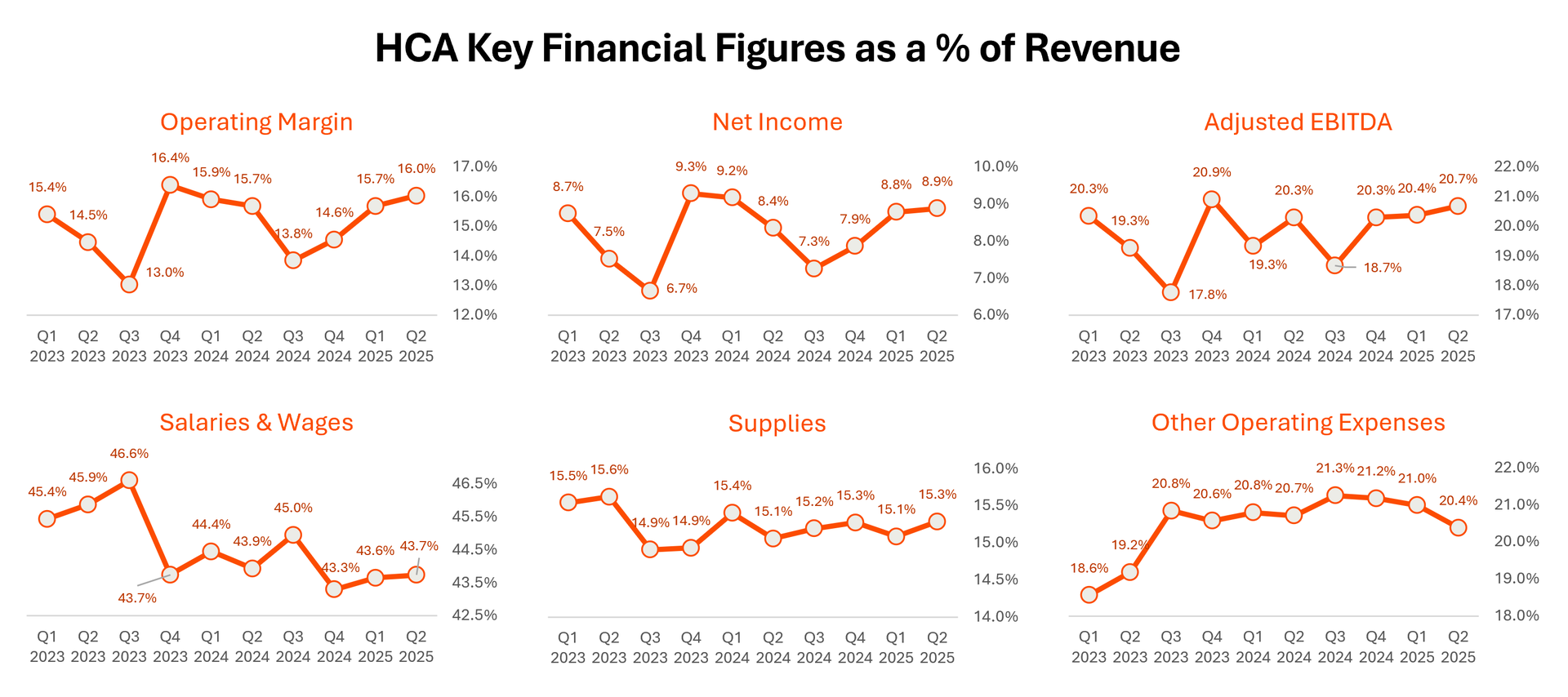

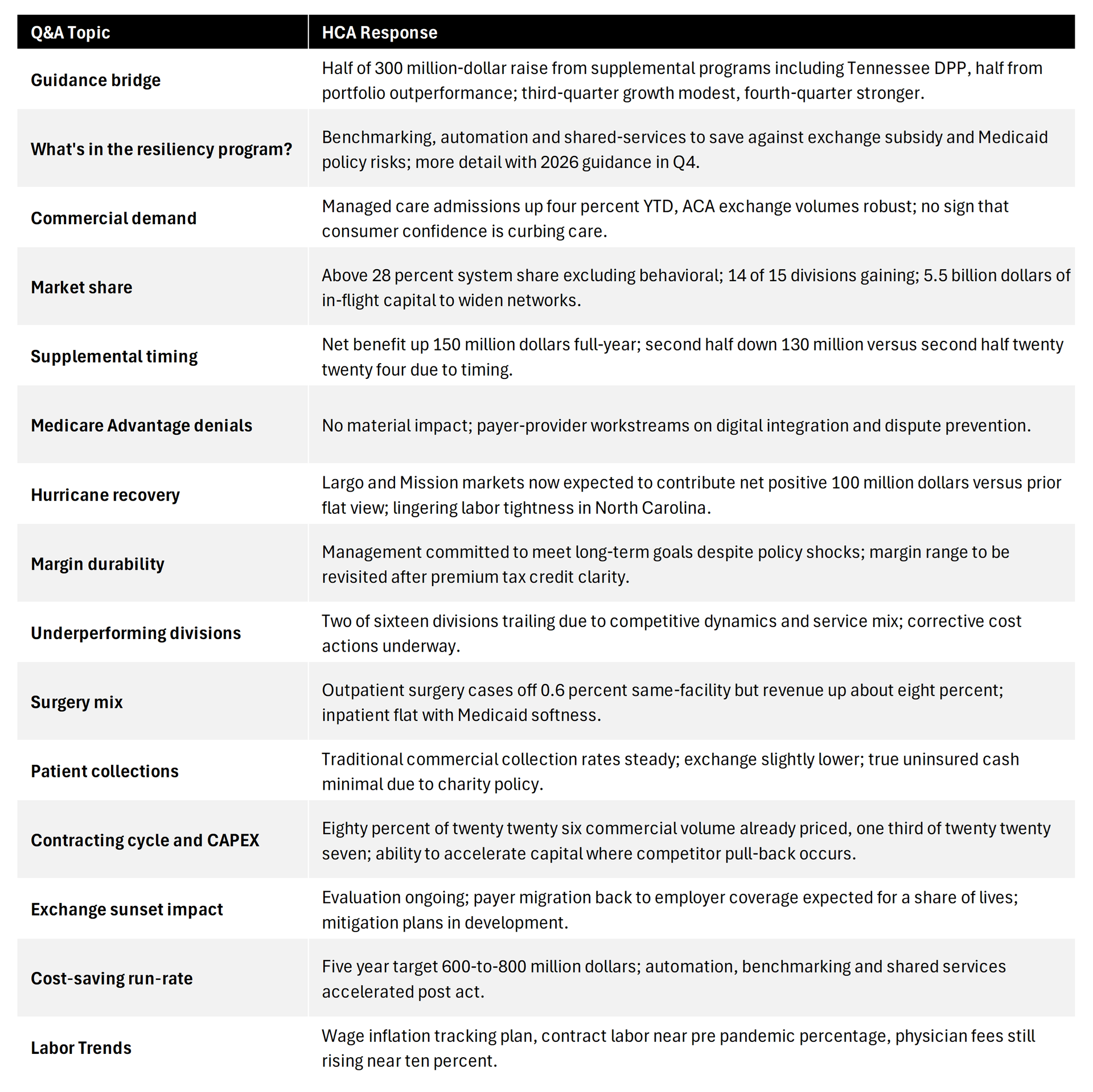

Similarly to Tenet, HCA continues to set itself apart from the rest of the hospital pack and is benefitting from a strong, stable hospital operating environment in 2025. In fact if you went through HCA's recent earnings reports and searched for the words "strong" or "stable" you'd probably find it more than a handful of times. Based on HCA's strong demand backdrop within its growing existing markets, HCA raised guidance during this quarter in-step with Tenet, and they've seen 16 consecutive quarters of volume growth. Here are the key issues to lock in on for hospitals during Q2: - One Big Beautiful Bill implications: Supplemental payment program cuts, ACA enrollee wind-down, work requirements…all will lead to worsening payor mix for hospitals nationwide and major uncertainty for healthcare executives headed into 2026. That being said, HCA did mention a lower impact on non-expansion states, where 60% of HCA Medicaid volume & revenue sits. What is HCA doing to mitigate any potential losses from ACA payor mix deterioration? We're not sure quite yet - management was pretty vague on the call, noting a 'financial resiliency program' they'll update us on in Q4

- Our resiliency efforts…address both benchmarking our corporate departments and shared service organizations against best practices and finding operational improvement opportunities. We are deep in the middle of our field-based resiliency efforts, many of which we commented on before from length of stay and improvement opportunities with our case management operations through significant opportunities around both our automation and our digital transformation agenda. And our labor and supply-related resiliency plans are also very developed and mature. We will give more updates on that, Ann, when we get to the fourth quarter call.

- Labor dynamics: HCA and Tenet continue to set themselves apart on the labor front - near or at all-time lows on a percentage of revenue basis. Which begs the question - is this ruthless efficiency, or are we cutting corners? Or…are we upcoding on the revenue side, or simply…extremely efficient. You guys tell me.

- Utilization environment: Volumes continue to be strong for HCA - in particular noting strong growth in cardiology, obstetrics, and neonatal services highlights HCA's focus on high-margin, specialized service lines that also serve to increase acuity and therefore reimbursement per unit of volume.

|

I do believe in the near term that our finance resiliency program should offset the exchange provisions in the act. In the longer term, as it relates to the act specifically, with both the delayed start and the phased-in nature of these provider tax and state-directed payment reimbursement reforms, along with the potential for the approval of the submitted supplemental payment applications, we believe HCA will be able to generally manage these impacts with our resiliency efforts without material impact to our long-term guidance. Specific to EPTCs, at this point, we do not know what the outcome will be. As noted, we are working to develop our resiliency programs to offset as much as possible any adverse impact should they expire. |

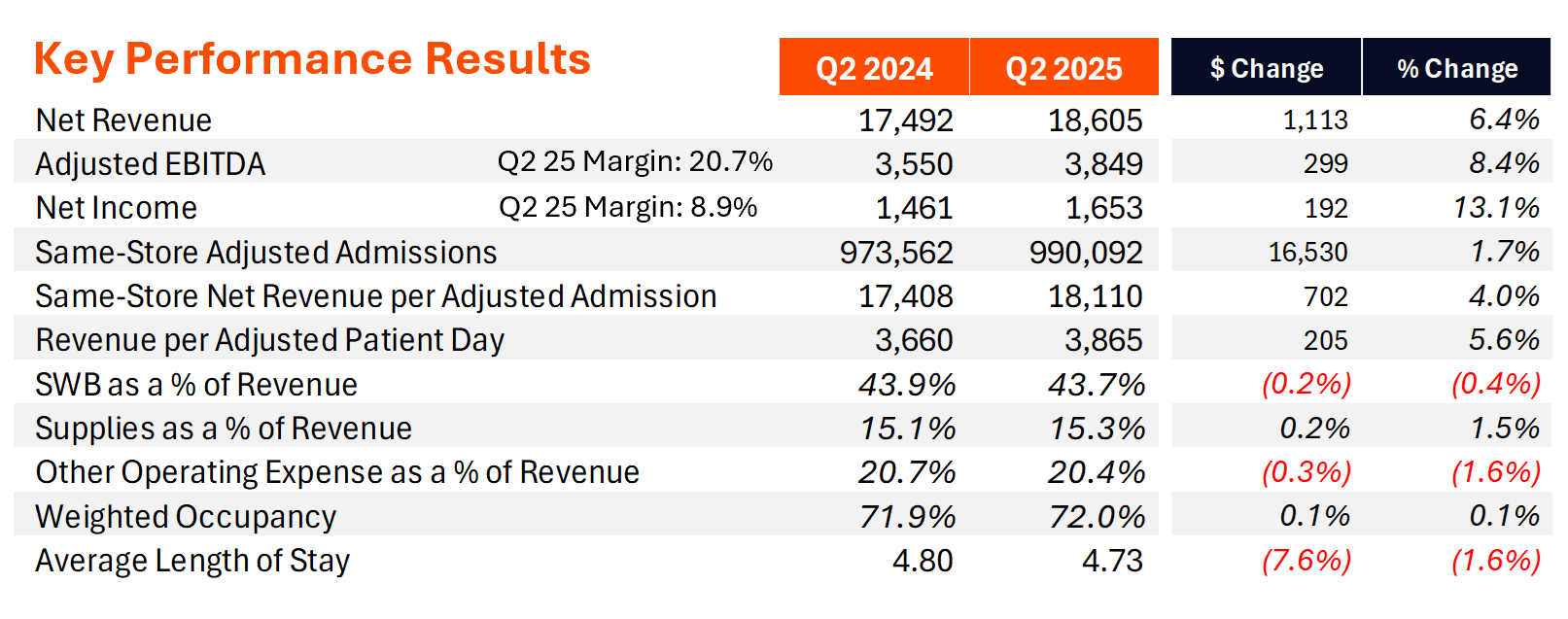

Despite some volume deceleration in the quarter, HCA noted sixteen consecutive quarters of overall growth and its diversified portfolio with 14 out of 15 divisions experiencing adjusted admissions growth: - Managed care adjusted admissions grew 4% (including decelerating growth in exchanges)

- From first quarter to second quarter of '24, our exchange equivalent admissions increased 14%. This year, from first quarter to second quarter of '25, they're up about 3%.

- Medicare grew 3% YTD slightly impacted by the 2-Midnight Rule sunsetting, while Medicaid was slightly down (1.2%) and self-pay slightly up (+1.5% - all below HCA expectations, notably)

- Notable service line volume growth included cardiac procedures (+5%), obstetrics (+3%), neonatal care (+13%) while pediatrics and behavioral volumes shrank.

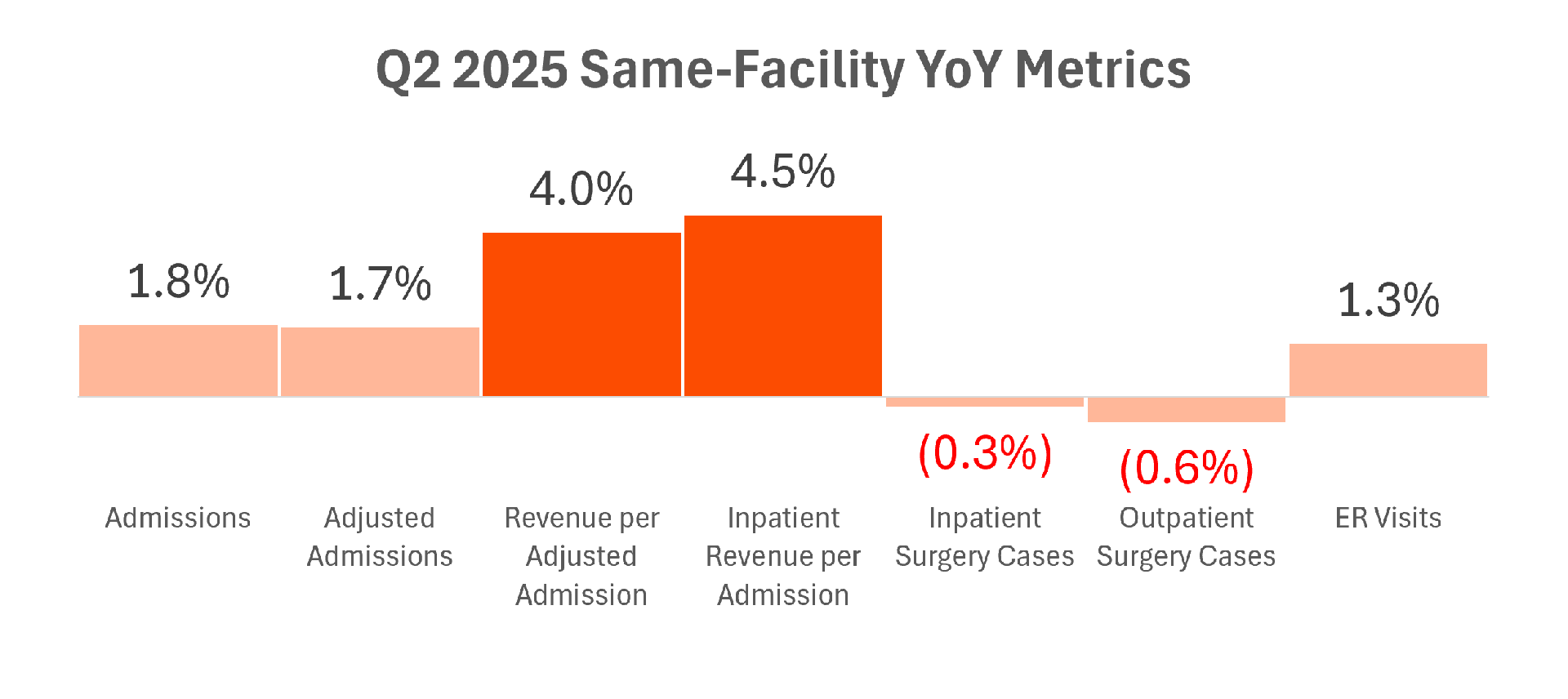

- Medicare Advantage volumes now comprise 58% of total Medicare admissions, though no impact seen on the denials front for HCA, and they noted work on the RCM side to optimize management of denials.

- On the surgery side, you can see the same trend playing out as in previous quarters - it's down mostly because of Medicaid redeterminations and self-pay declines in volume. HCA still sings the same tune as far as net revenue per case - total revenue is up "7.5%, 8%, 8.5%" in the outpatient surgery book of business.

- On the inpatient side, HCA is trending north of 70% occupancy - up to 73% or 74% YTD.

Still, volume came in below HCA's expectations (2.3% YTD adjusted admissions growth and 1.7% same-facility in the quarter). HCA attributed that softness to Medicaid redeterminations and self-pay / charity volumes. Meanwhile, as noted Medicare growth expectations also came in lower than expected. Interesting to call out the difference between HCA's volume and utilization expectations versus some payor commentary on the other end of the spectrum. |

HCA saw strong revenue per adjusted admission and IP revenue per admission figures on a same-store basis. Given the strong payor mix, HCA enjoyed topline revenue growth of 6.4%. HCA also saw a $100M beneficial increase stemming from prior period reconciliation payments and accruals timings and management also mentioned the new Tennessee directed payment program approved in late June (a positive development). - ACA volumes comprised 8% of admissions and 10% of overall net revenue.

- HCA continues to see mid single digit rate escalators on the rate side and hasn't seen an impact to collectability or higher accounts receivables as a result of rising patient costs.

- Kevin Fischbeck from BofA had a sharp question related to ACA payor mix, essentially asking whether it's reasonable to assume that ACA admissions would trend back to 2019 levels. HCA more or less dodged the response though it's in line with what most are thinking would happen in light of subsidy expiration.

|

Adjusted EBITDA continues to expand - growing another 8.4% year-over-year in Q2 2025 up to 20.7% from 20.4% a year ago. Look at the trend in salaries & wages - 43.7% of revenue in the quarter is well below what most health systems are putting out. HCA also mentioned professional fees inflation of 10% year over year while supplies saw an uptick stemming from higher spending on cardiac devices in the quarter.

After years of contract labor shrinkage, HCA called out North Carolina labor market tightening leading to an increase in contract labor in that particular market. Whether this is a sign of things to come or a short term blip (or if the public fiasco related to the Mission acquisition has resulted in recruitment challenges) remains to be seen - but HCA noted it's in 'pretty good shape' from a labor market perspective. Today, HCA's contract labor as a percentage of salaries sits at a low 4.3% - right where it was pre-pandemic. |

HCA has held a strong balance sheet and historically low debt leverage for several quarters now. They haven't spent any capital on large scale M&A in preference for a de-novo approach in existing markets to build out density and continue to capture incremental market share. - HCA spent $1.2B on CAPEX in the quarter, or about 6.4% of total revenue in Q2

Also very notable, Mike Marks, HCA's CFO, made a comment about the OBBA's provision to make 100% bonus depreciation permanent retroactive back to inauguration day, which will benefit HCA and others undergoing capital projects and M&A from a tax perspective and is a low key big benefit to capital-intensive businesses and I imagine those engaging in M&A HCA highlighted a multiyear digital transformation that leverages automation in revenue cycle, case management and workforce scheduling. Artificial intelligence pilots in care coordination and sepsis prediction are scaling system‑wide. Payor partnerships now include joint administrative simplification road‑maps and near‑real‑time data feeds. No major acquisitions closed in the quarter; HCA continues to evaluate tuck‑ins and joint venture surgery center expansions. |

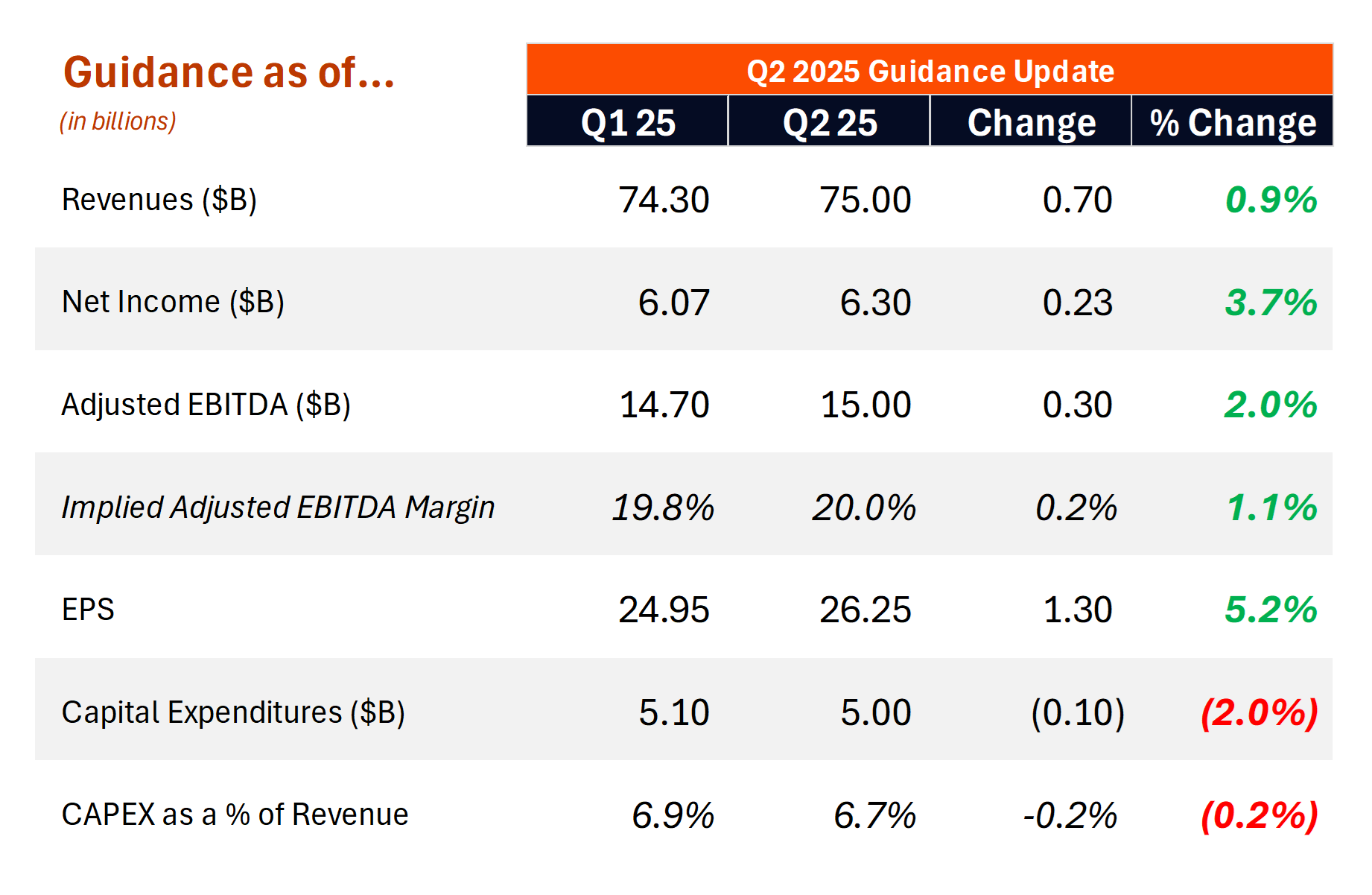

HCA increased guidance as seen above based on the following factors: - $300M increase to AEBITDA, half of which is from state supplemental payment programs, including the new Tennessee program (with a chunk of it hitting in Q3) and the other half related to HCA's overall portfolio - $200M better performance than expected in hurricane-heavy (and most other) markets and then $50M lower in a 'couple underperforming markets.'

Policy watch‑list items are the One Big Beautiful Bill Act's Medicaid and exchange reforms and possible lapse of enhanced premium tax credits; management expects internal resiliency plans to offset most headwinds. |

Business as usual, with perhaps some small chinks in the armor - whether they're polished or not will play out over the next few quarters. HCA is up to 28% enterprise-wide market share across its footprint. What is HCA doing to outperform financially that others can take away from the quarter? - Strategic Service Line Expansion: Target high-margin growth areas in demographically strong regions, evidenced by HCA's cardiology, obstetrics, and neonatal successes. Easier said than done.

- Operational Agility: HCA's sophisticated labor management and pipeline of nursing labor supply has served to stabilize expenses amid persistent inflation and labor shortages.

- Digital Transformation: Invest aggressively in digital partnerships and AI-driven solutions to streamline revenue cycle management and care coordination. Find ways to upcode.

- Policy Resilience: Build comprehensive financial resiliency programs and scenario planning capabilities, following HCA's proactive stance towards ACA subsidy uncertainties and Medicaid policy changes.

|

|

|

Random personal anecdotes and musings from me |

Can you sense it?

The magical feeling of football in the air?

In just 2 short days, we will have football for the coming 7 consecutive months.

And I just bought my son his first Texas jersey. He's already saying Hook 'em by the way. We're still working on the hand sign (it's a tough one for a 22 month old, alright?)

Anyway, my replies are always open for college football trash talking!

Til Thursday, Hospitalogists. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 46,000+ executives and healthcare decision-makers. |

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments