Happy Thursday, Hospitalogists. When it comes to health system strategy, Tenet is doing everything right. Here's a robust breakdown drilling into everything that happened at the large for-profit, highly profitable publicly traded hospital operator in Q2. The below analysis is a mix of visuals, some shorthand, and some narrative from yours truly. Let's dive in. Oh, and if you find this helpful do me a favor and forward this to someone, or share it with your team. It greatly helps me and the Hospitalogy cause to have my newsletter shared around for all to see, kinda like Christmas spirit except even better since it's a healthcare newsletter. |

Was this email forwarded to you? |

|

|

BLAKE'S BREAKDOWN: Tenet Healthcare's Q2 2025 Earnings Overview |

Going deeper on an interesting topic, theme, or trend |

Tenet's Q2 2025: Crushing the ASC Game with USPI; High Acuity Strategy Remains Key |

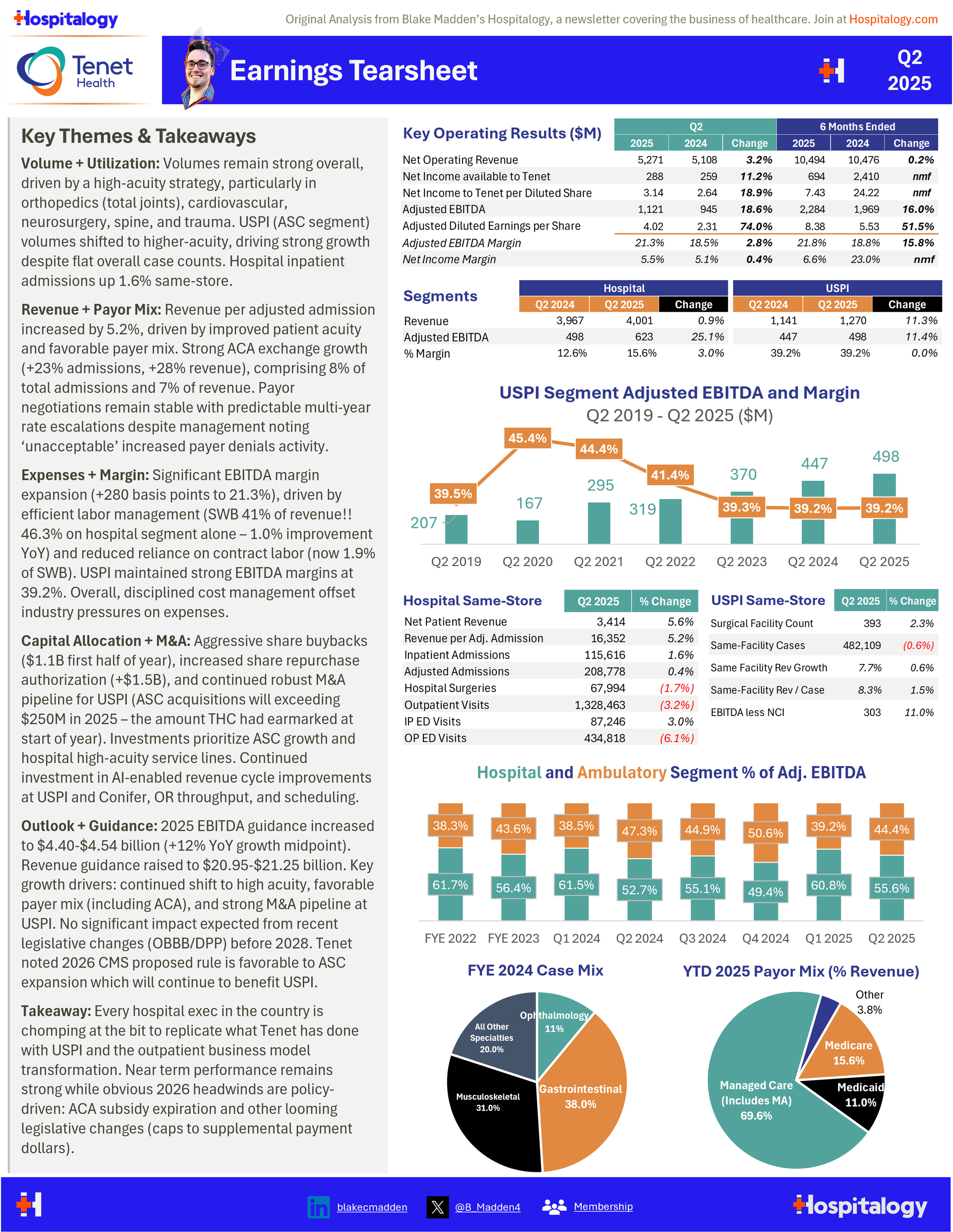

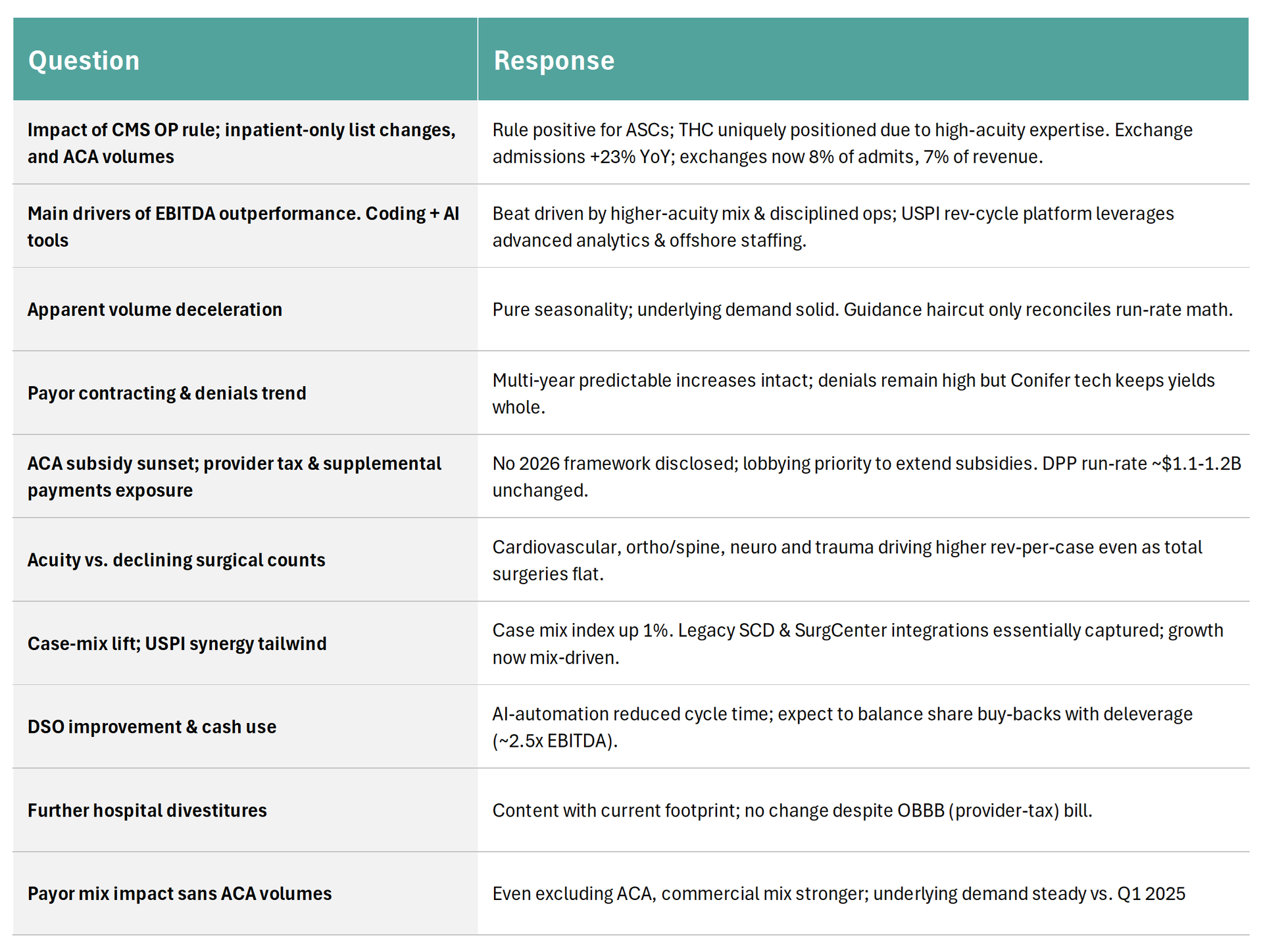

My Tenet one-pager, exclusively for my beloved Hospitalogists: |

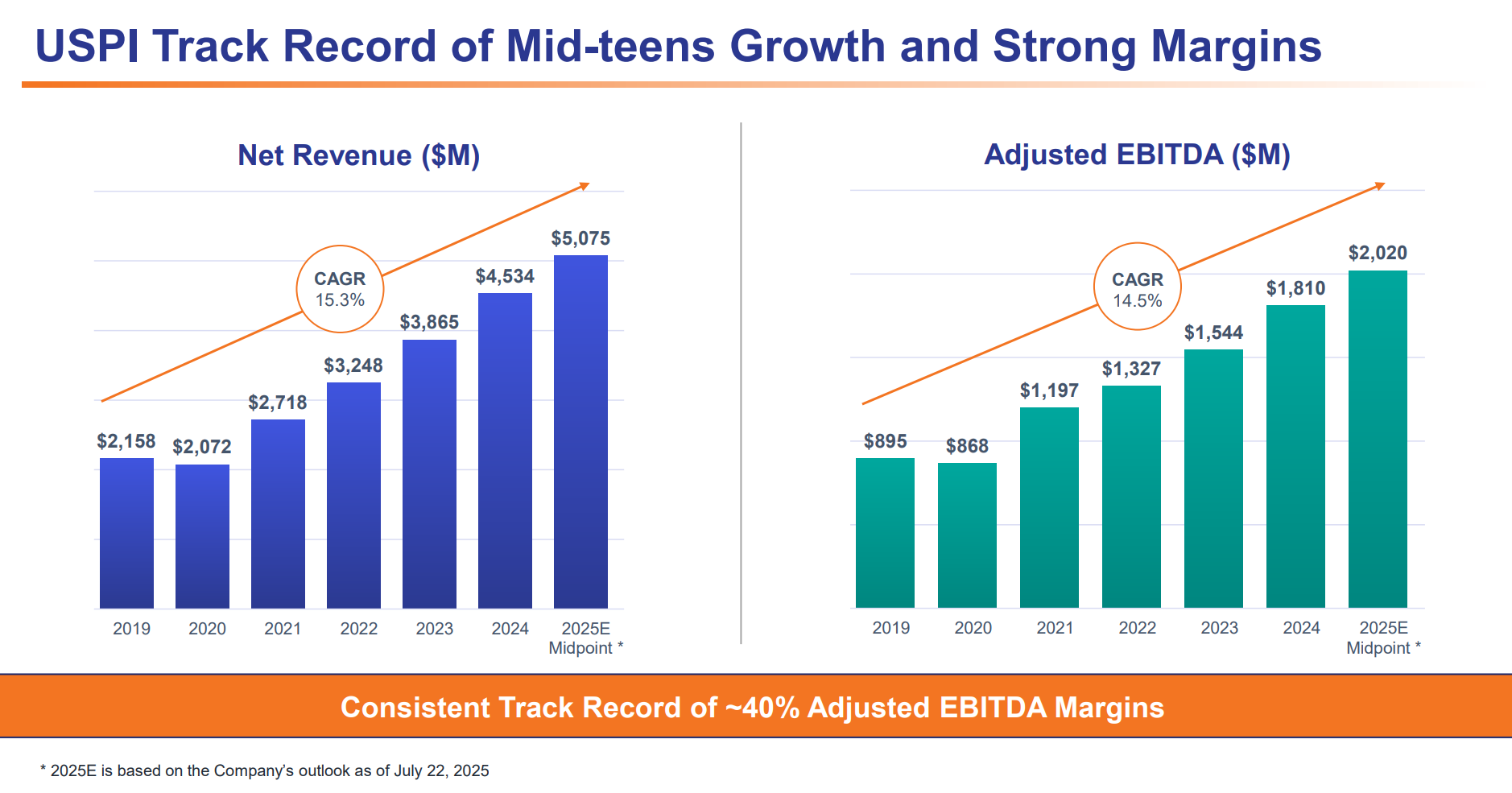

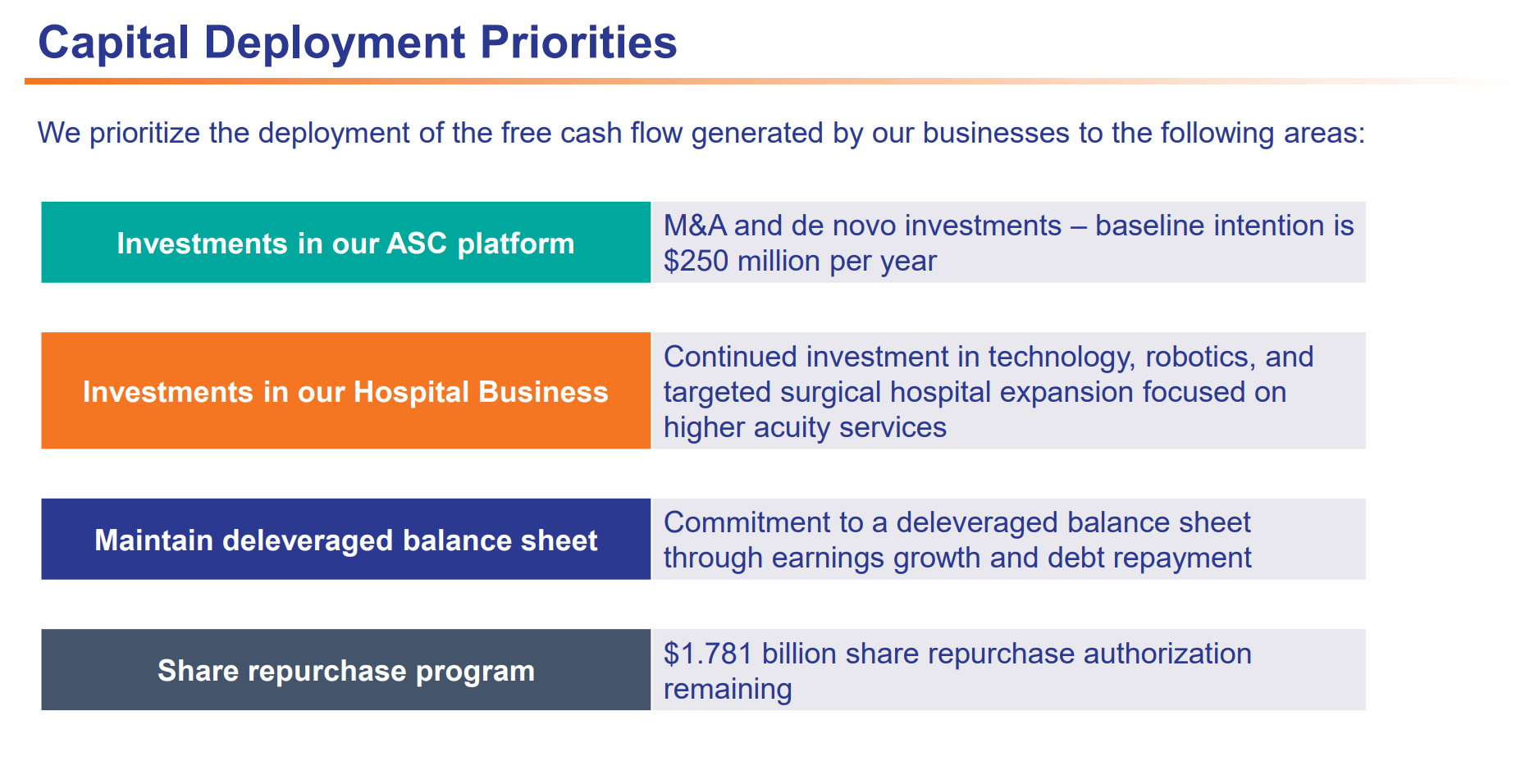

USPI fires on all cylinders - ASC migration is accelerating: Tenet's ability to post mid‑teens ASC revenue CAGR with ~40 % EBITDA margins (leading to consolidated adjusted EBITDA margin of 21.3%) validates the profitability of shifting ortho & spine volumes out of hospital ORs. Health‑systems lacking an ASC network risk both revenue and physician alignment trouble (physician ownership is key). Look at the below graphic and see exactly where the bulk of large health system dollars ought to go. Outpatient facilities like ASCs require less capital and are more profitable (40% vs. mid-teen margins on the hospital side). From a capital expenditure perspective, USPI's capex as a % of revenue sat at 1.9% in Q2. Tenet's hospital segment? 5.2%. |

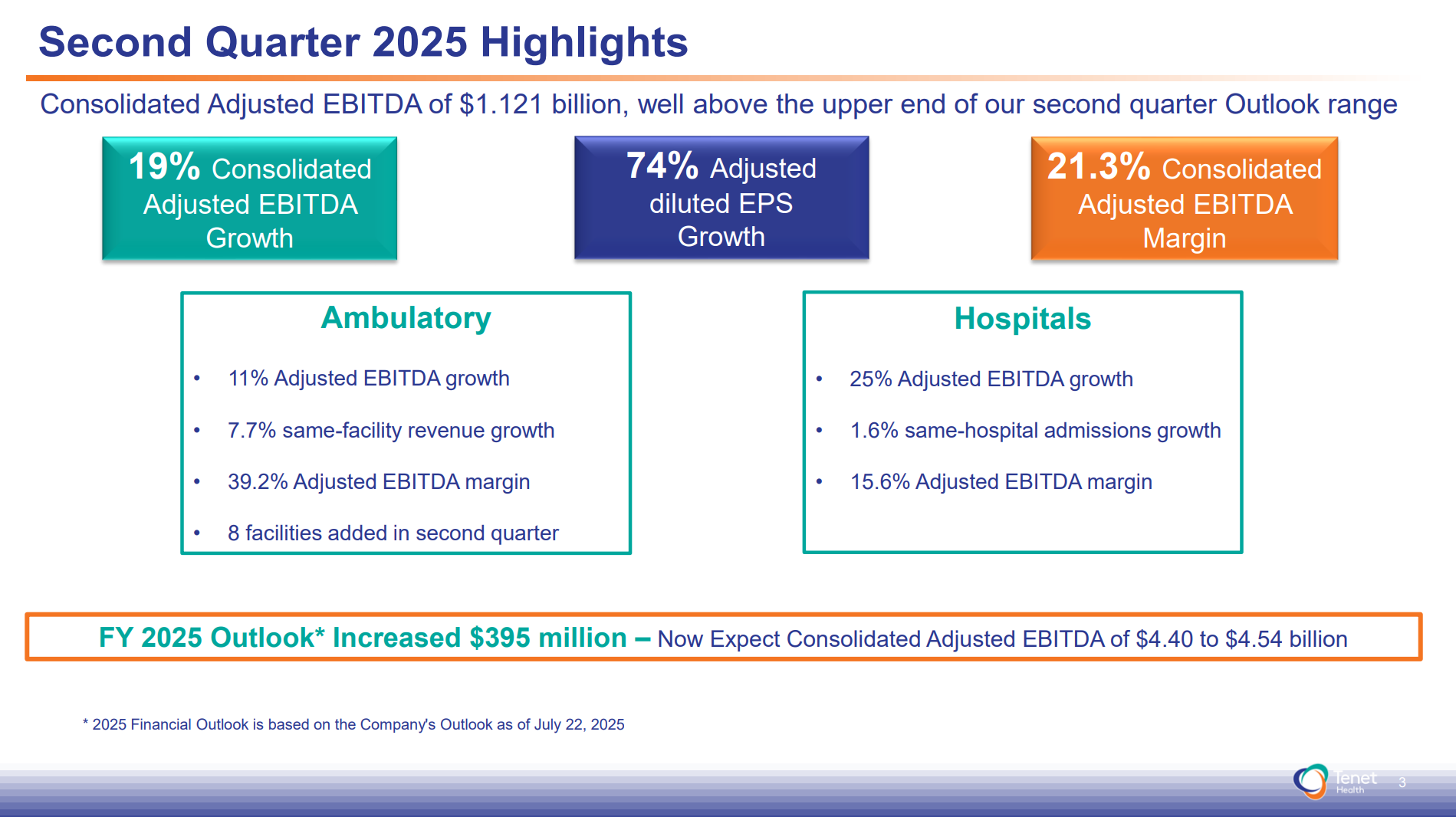

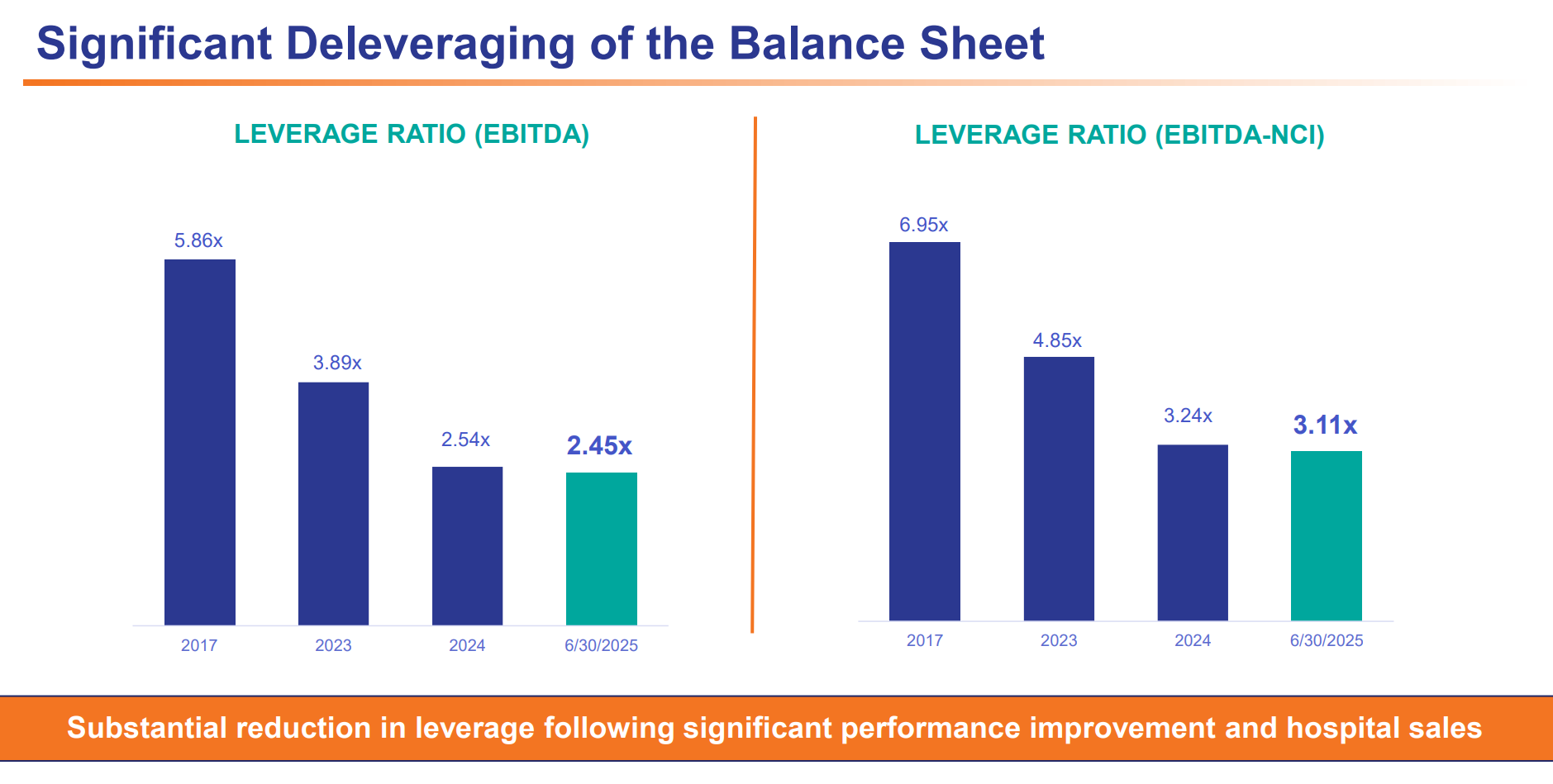

High‑acuity hub strategy works: Despite selling 13 hospitals since 2022, Tenet's hospital EBITDA is up 25% year over year (YoY); broad scale is less critical than focused service‑line depth, transfer‑accept policies and disciplined labor management. Tenet's high acuity successes beg the question whether there's an AI player behind the scenes supercharging their documentation. Historically Low SWB Continues: Salaries, wages, and benefits hit 41% - 41%!! - of net revenues in Q2, a 1.4% improvement and 10%-15% more efficient than nonprofit health system counterparts. De-levered to the Max: With historically low debt leverage (<2.5x; 3.11x EBITDA less NCI) and ~$2B annual FCF, Tenet can simultaneously expand USPI, solve for higher inpatient acuity mix, and continue buybacks. Policy Updates: Exchange subsidies and state DPP/provider‑tax rules remain the two external swing factors, and they're big ones considering ACA volumes comprised nearly 10% of total Tenet admissions in Q2. Contingency planning for 2026 exchange churn and potential Medicaid supplemental taper is prudent across the industry. Volume and Utilization: |

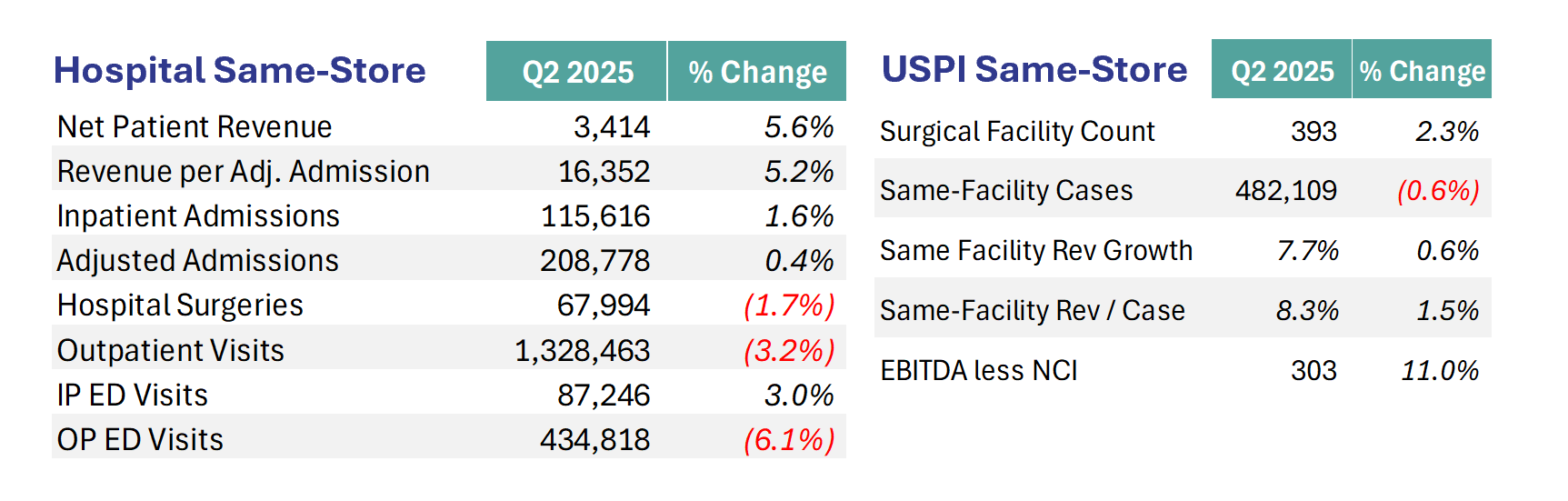

Volumes remain strong overall, driven by a high-acuity strategy, particularly in orthopedics (total joints), cardiovascular, neurosurgery, spine, and trauma. USPI volumes continue their shift to higher-acuity (noticing a theme? Higher acuity, higher acuity, higher acuity!!), driving strong growth despite flat overall case counts. Hospital inpatient admissions up 1.6% same-store. Hospital: Same-store admissions up 1.6%; adjusted admissions growth revised down slightly to 1.5%-2.5% for full year. Tenet reiterated its "high‑acuity hub" strategy and full‑year same‑store adjusted‑admission growth of 1.5‑2.5%. |

ASC (USPI): Same-facility revenues up 7.7%, total joint replacements up 12.6%, net revenue per ASC case up 8.3%, overall case volumes slightly down (-0.6%) due to shift to higher acuity procedures. - High-acuity strategy continues in cardiovascular, ortho, spine, neurosurgery, and trauma surgery. Case‑mix index up ~1 % y/y; average LOS down 2.8 % to 4.82 days in hospital segment indicating efficient throughput despite sicker patients.

- Exchange patient volume: 23% admission growth, heavily emergency-driven, consistent with past trends.

Revenue Growth and Payor Mix: Revenue per adjusted admission increased by 5.2%, driven by improved patient acuity and favorable payor mix. Strong ACA exchange growth (+23% admissions, +28% revenue), comprising 8% of total admissions and 7% of revenue. Payer negotiations remain stable with predictable multi-year rate escalations despite increased payer denials activity. - Consolidated revenue: $5.3 billion, up 3.2% YoY.

- Revenue per adjusted hospital admission: up 5.2%, driven by acuity and payer mix.

- ACA Exchange: Now 8% of admissions, 7% of revenue. Volume up 23%, revenue up 28% YoY.

- Stable payer negotiations, with "no unusual" pushback or disruptions, but ongoing issues with elevated payer denials activity addressed through AI and offshore capabilities.

- USPI reimbursement: Net revenue per case +8.3 % driven by payor‑contract escalators (with inflation incorporated) and higher case‑mix (joints, spine, neuro).

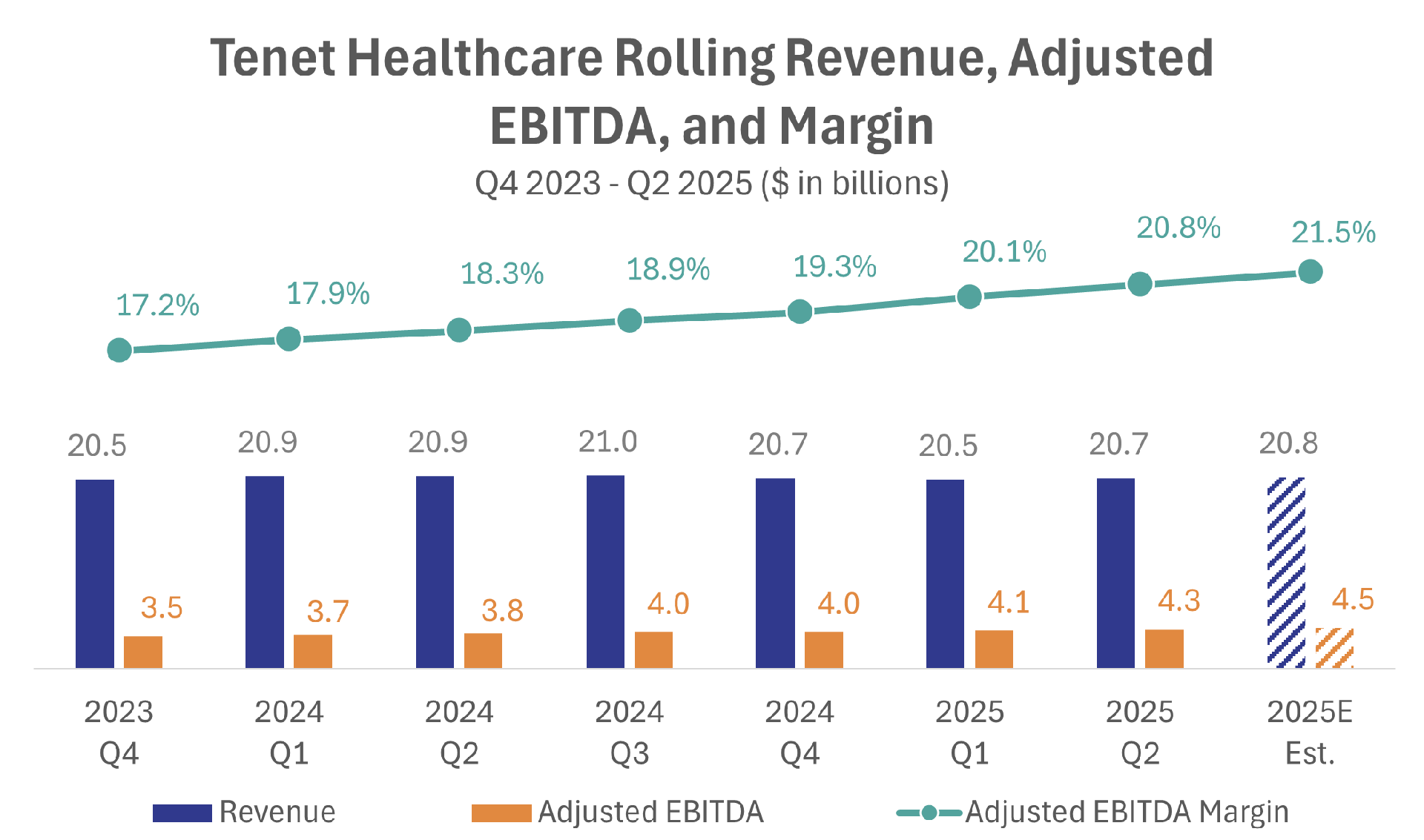

Expenses and Margin: Significant EBITDA margin expansion (+2.8% to 21.3%), driven by efficient labor management and reduced reliance on contract labor (now 1.9% of SWB). USPI maintained strong EBITDA margins at 39.2%. Overall, disciplined cost management offset industry pressures on expenses. - Hospital segment margin: 15.6%, up 300 bps YoY.

- USPI segment margin: 39.2% - flat YoY.

- Salaries, Wages & Benefits (SWB): 41% of net revenues (sheesh), improved by 1.4% while hospital segment SWB alone was 46.3%. Contract labor comprised 1.9% of SWB expense.

- Supplemental Medicaid revenue: $79 million favorable impact (one-time benefit).

- Direct expense per adjusted patient admission $15,981 (+5.0%); per adj. patient day $3,435 (+4.6%).

Capital Allocation: |

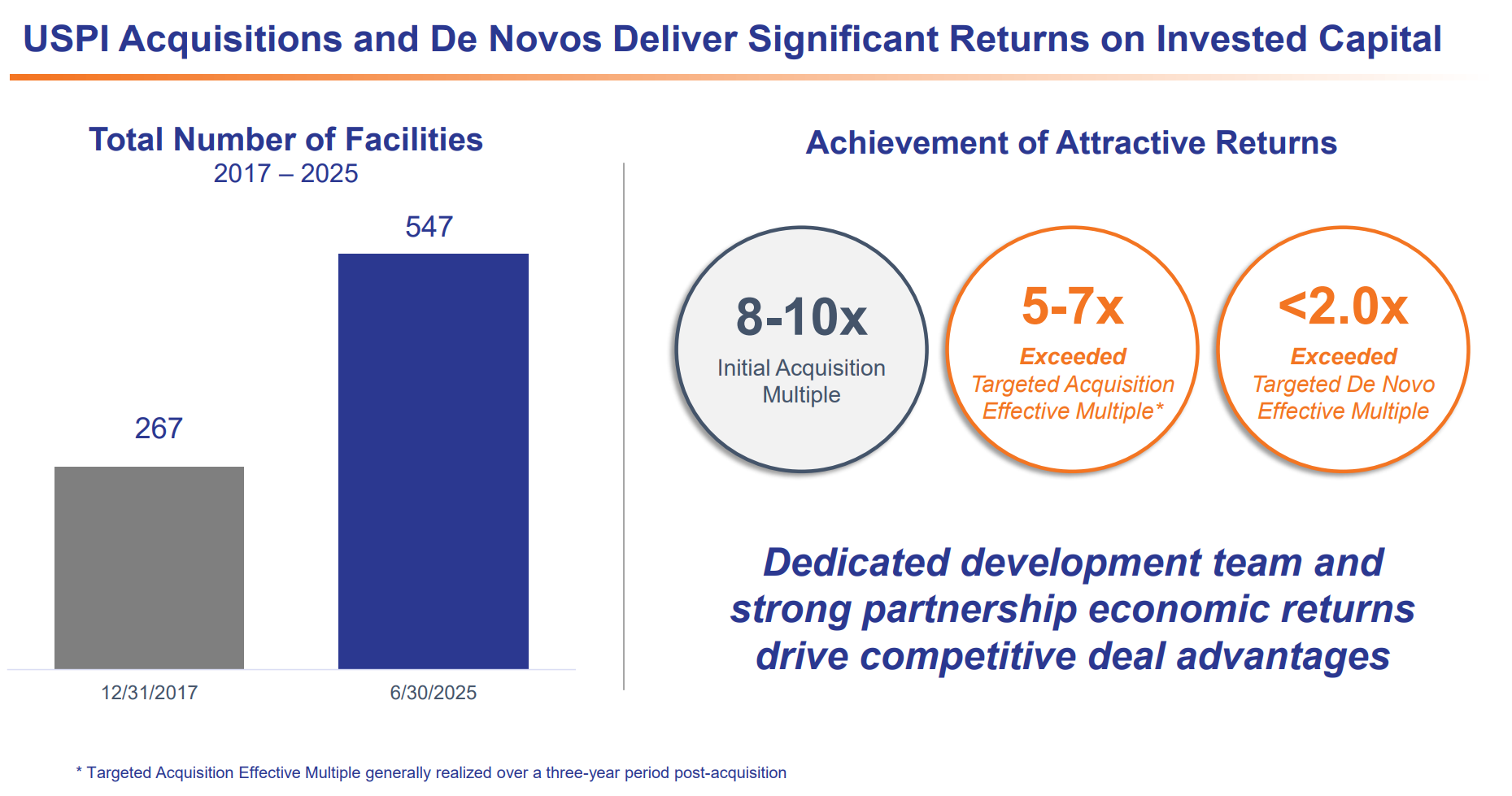

Aggressive share buybacks ($1.1B first half of year), increased share repurchase authorization (+$1.5B), and continued robust M&A pipeline for USPI (ASC acquisitions exceeding $250M in 2025). Investments prioritize ASC growth and hospital high-acuity service lines. Continued investment in AI-enabled revenue cycle improvements at USPI and Conifer. Free cash flow generation hit $743 million in Q2 while Tenet full-year guidance raised to ~$2.2B. ASC M&A Spend: Exceeding baseline of $250 million; 8 new centers added in Q2, including spine and ortho-specialty centers. YTD spend ~$130M; pipeline strong – expect >$250 M in 2025 with 8 centers added this quarter. Tenet targets post‑synergy EBITDA multiples of 5‑7x (with pre-synergy multiples likely 7x-9x as industry standard). |

No significant debt maturities until 2027. strong balance sheet ($2.6 billion cash) and the aforementioned historically low leverage. |

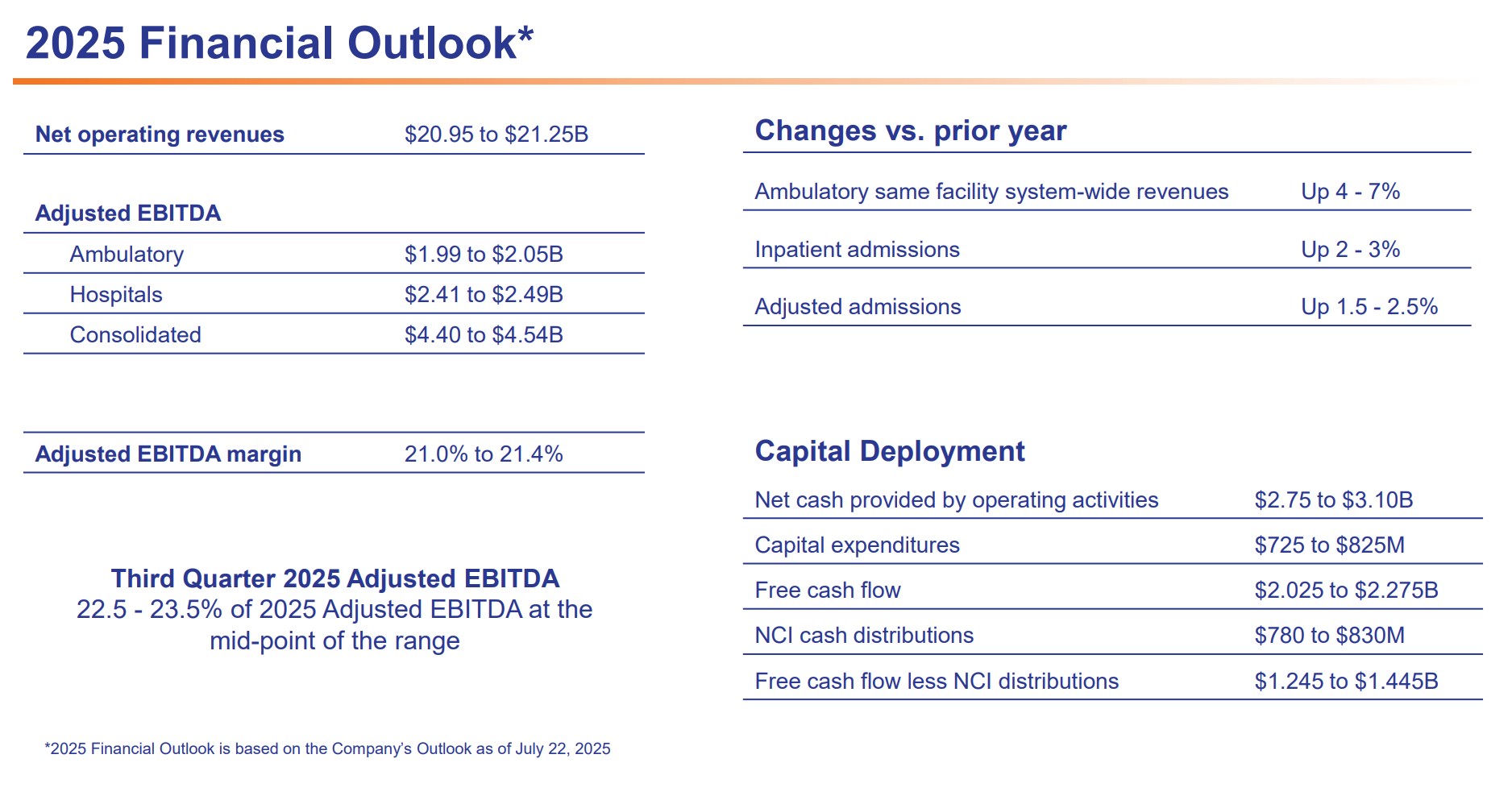

Outlook and Guidance: Once again, Tenet upped its guidance with the following key drivers as assumptions: acuity driving net revenue per volume, 4‑7% same‑facility ASC revenue growth, 1.5‑2.5% same‑store hospital adjusted‑admission growth, SWB inflation ~3%, and minimal Covid headwind. THC has no plans to incorporate exchange‑subsidy expiry or DPP claw‑back effects prior to 2028 which I found notable. |

Every hospital exec in the country is chomping at the bit to replicate what Tenet has done with USPI and the outpatient business model transformation. You should expect to see large nonprofits quietly replicate this ASC buildout strategy nationwide. Near term performance remains strong. Exchange subsidies and state DPP/provider‑tax rules remain the two external swing factors. Contingency planning for 2026 exchange churn and potential Medicaid supplemental taper is prudent across the industry. Tenet is flourishing in 2025 and has expanded its margin significantly in recent memory through aggressive USPI growth. |

Key Management Commentary - The most notable trend in the second quarter is the strength and success of our high acuity strategy... continuing to demonstrate the ability to generate revenue and earnings across our hospital portfolio.

- In USPI, we've seen high acuity, good case mix, good payer mix, good growth in ortho and total joints...resulting in net revenue per case up 8.3% and strong EBITDA margins of 39.2%...Our strength is in cardiovascular, orthopedics, spine, neurosurgery, broad-based general surgery, robotics... emergency-driven trauma, and trauma surgery.

- Health care exchange remains important; we saw about a 23% increase in admissions and 28% increase in revenues year-over-year. Exchange volumes now represent 8% of total admissions and 7% of total consolidated revenues…Extending the exchange subsidies is important...exchanges were a critical safety net during Medicaid redeterminations...and represent critical support for small businesses…Given current administration dynamics, subsidy extension affects red states more significantly, emphasizing its political importance…Our Medicaid supplemental payments run rate remains about $1.1 billion to $1.2 billion annually.

- Denials activity has ramped up post-COVID to levels I would argue are not acceptable... We have deployed more technology, automation, trained offshore staff, and adapted effectively.

- Our consolidated salary, wages, and benefits were 41% of net revenues, a 140 basis point improvement from prior year... driven by data-driven capacity management, disciplined expense controls, and lower contract labor…We benefited from improved recruiting strategies, nursing school partnerships, and improving retention rates... real investments in nursing and hospital supervisory levels have created a stable workforce, supporting margin improvement.

- We expect to exceed our baseline intention for $250 million of M&A spend in USPI for 2025... we added 8 new centers this quarter specializing in high acuity procedures.

|

|

|

SPONSORED BY PHRMA Foreign-first pricing is a bad deal for American patients. To lower prescription drug prices in America, let's address the real reasons Americans pay more. The U.S. is the only country that lets PBMs and 340B hospital markups drive up medicine prices for patients, while other countries refuse to pay their fair share for American innovation. It's time to crack down on the middlemen and end the free riding. |

|

|

My almost 2-year old has a new favorite catchphrase - "Happy birthday, yogurt!" You might say he's not quite grasping the meaning of the phrase but I'm willing to let it slide. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

| Get your brand in front of 45,000+ executives and healthcare decision-makers. |

I'm building a community of leaders in strategy, finance, and ops

at hospitals and health systems to help us connect, learn, and grow together. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments