PARTNERED WITH  |

|

|

Happy Tuesday, Hospitalogists! Today's send is a roundup on key themes and notable developments in the value-based care space across Astrana, Privia, agilon (oof), and quicker hits on Evolent, P3, and the Oncology Institute. Finally, I'm excited to share I'll be hosting an AMA ('ask me anything') with Elliot Cohen, Cofounder of General Medicine which just raised $32M to redefine healthcare consumerism and build a consumer-centric, delightful platform for people to find and receive high-quality care. It's a massive bet and will be a great conversation! Register here. |

Was this email forwarded to you? |

|

|

SPONSORED BY NAVINA I encourage you to read this article from Navina. It shares what happens when industry leaders think bigger about using AI to thrive in value-based care, such as using it to decode contract details like attribution and risk adjustment, and to prioritize high-impact initiatives that actually move the needle. This isn't yesterday's AI. This is today's applied AI… Embedded directly into clinical workflows for a smarter way to identify at-risk patients, target care approaches, and improve outcomes. Introducing efficiencies that save clinicians hours each week and reduce burnout. Providing insights and data that empower healthcare organizations to lower costs, boost quality metrics, and keep patients healthier. If you want to see what applied AI in value-based care really looks like…

|

|

|

Going a bit deeper on an interesting topic, theme, or resource |

Rounding up Value-Based Care in Q2 |

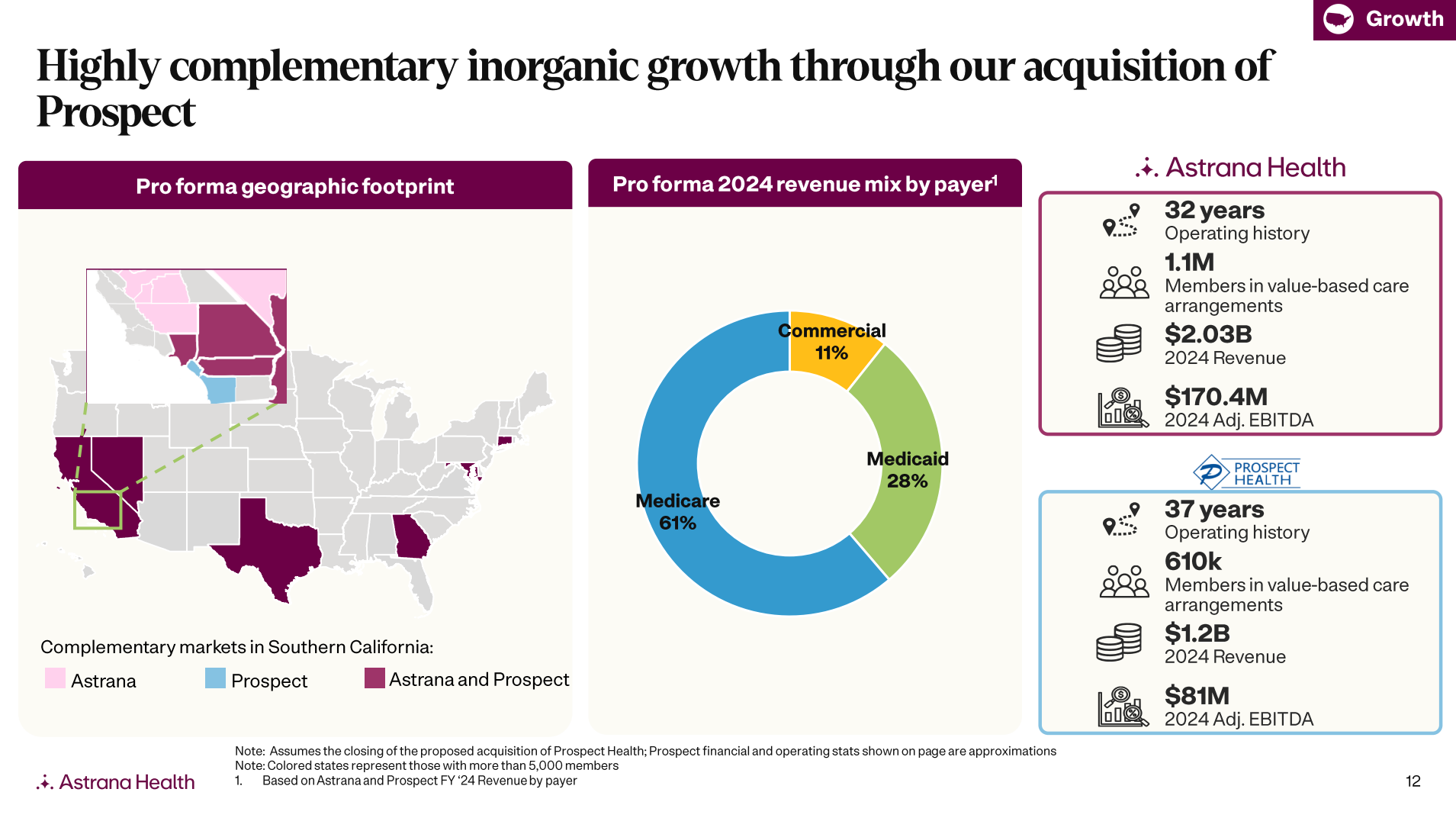

Astrana Health delivered another disciplined quarter with blended year over year medical cost trend near 4.5% - in line with expectations - as Care Partners outperformed, Care Delivery in Nevada was EBITDA positive, Texas tracked to breakeven, full risk rose to 78% of revenue, and the Prospect deal closed on better terms with 12 - 15M of synergies and leverage at 2.7x while Medicaid and exchange exposure look manageable and RAF held at 1.02 despite V28. Astrana will also work on integrating Prospect, formerly owned by Centene into its overall California market strategy. As noted in the earnings presentation, Prospect and Astrana are highly complementary culturally and align nicely geographically. Prospect was acquired for $705M (down from the announced $745M) from the bankrupt Prospect Medical Holdings, and the asset was expected to generate $1.2B in revenue and $81M in EBITDA in 2024, so this acquisition grows Astrana's revenue base by a half, profitably, and will hit $3.1-$3.3B in revenue and $215M - $225M in adjusted EBITDA in 2025. Of note, Astrana has made some splash acquisitions to fuel its market expansion plans over the last couple of years. Apart from Prospect, Astrana also acquired Collaborative Health Systems (yes, a different CHS) from Centene and Community Family Care Medical Group in early 2024. |

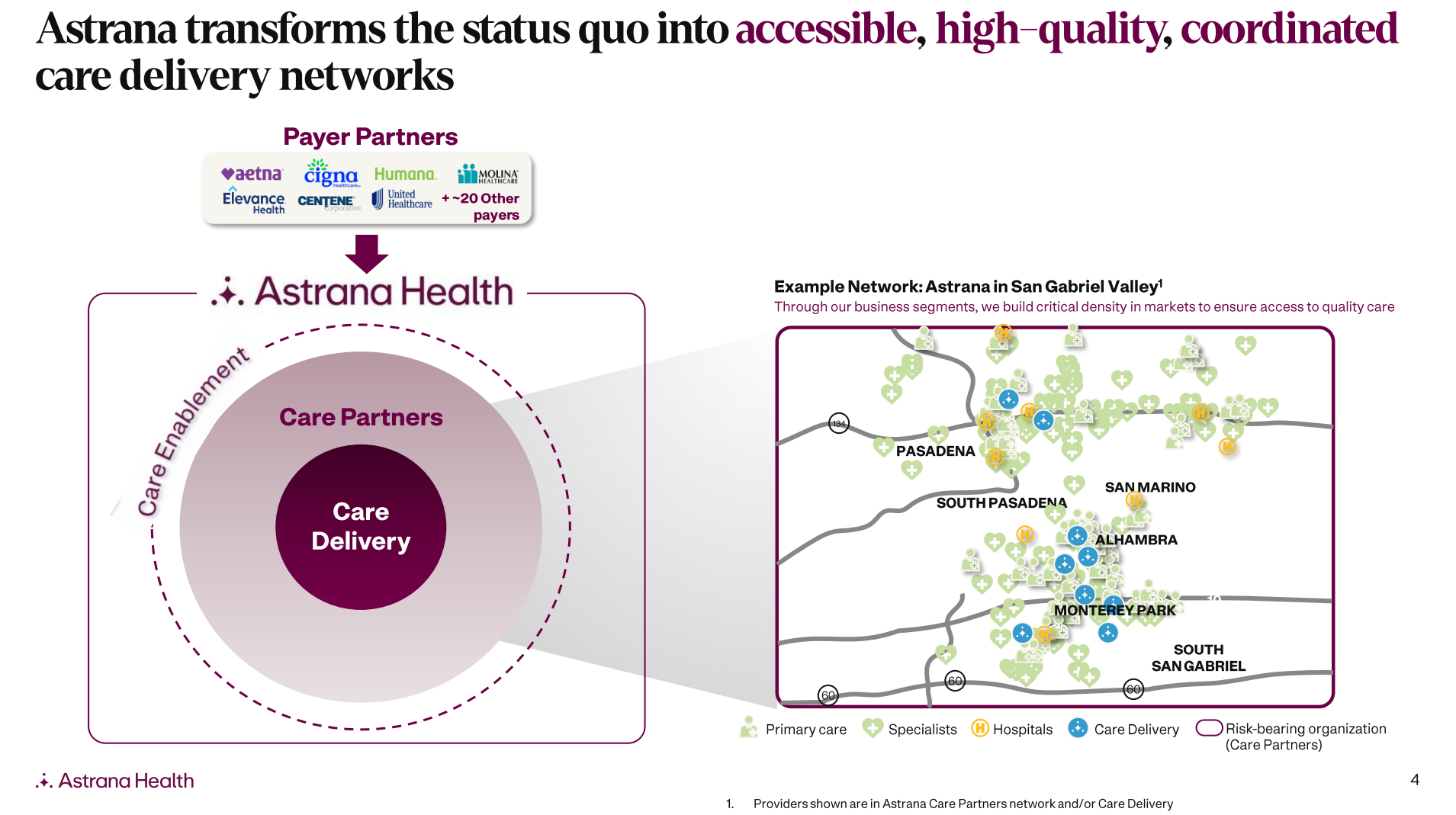

The below is a nice graphic illustrating Astrana's 3 operating segments and how they, hand in hand with market density and appropriate technology / data, deliver value to payors and patients: |

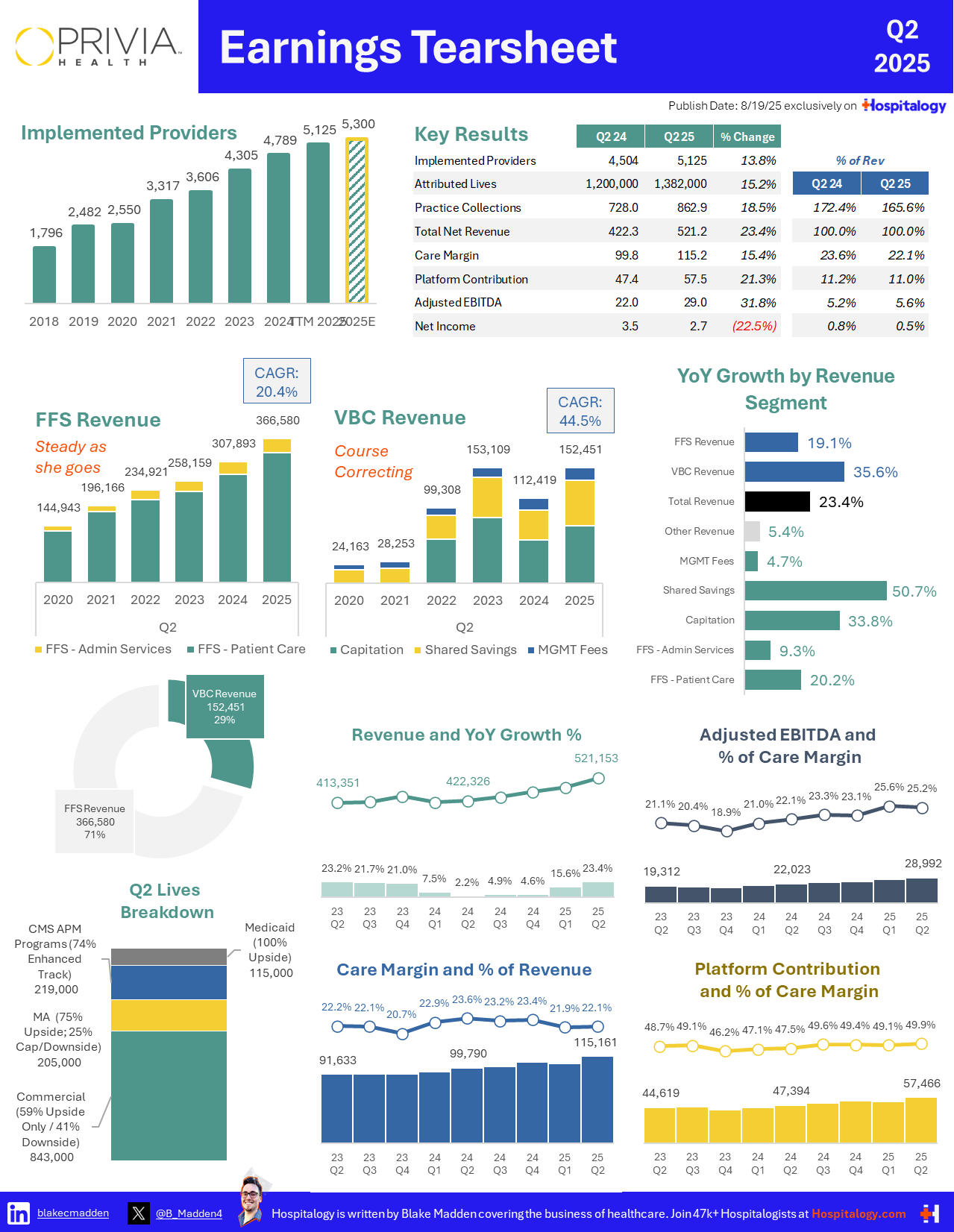

Privia Health executed cleanly across its physician led medical groups, risk entities, and tech and services platform with 5,125 implemented providers, 1.38M attributed lives, strong ambulatory utilization, and shared savings outperformance (50%+ growth!). As a result Privia raised guidance to the high end of its 2025 range. It's very telling to note the difference between analyst questions on successful platforms like Privia and Astrana asking about growth vectors versus other middling peers discussing profitability or tripping over their own feet. Questions were directed at Privia's sustainability of implemented providers (a key driver of Privia's overall growth) along with retention of existing clinical base. Privia's value prop and flywheel continue to…fly. From a technology standpoint, Privia called out scribing as reducing admin burden, and importantly, of course, improving productivity. RCM automation was also mentioned in helping with lower denials and days' A/R. Overall profitability is driven by growing into the MSSP Enhanced track, quality performance, physician productivity, and better overall RCM yield. |

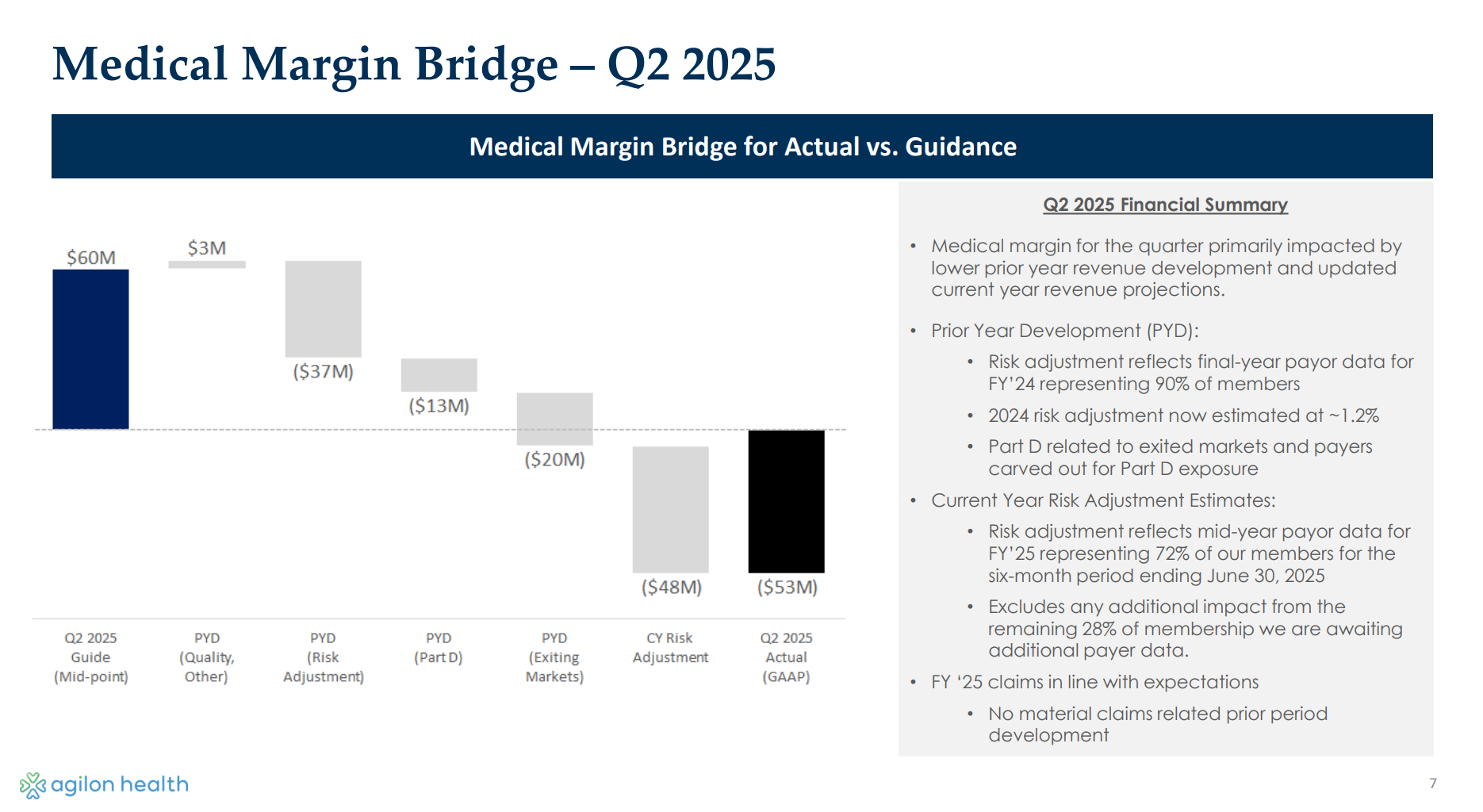

agilon Health continues to get destroyed by lagging payor data as it rolls out its new enriched data platform (now covering 72% of members). It missed on risk adjustment and recorded large true-ups, then reset ultimately withdrew its 2025 guidance along with seeing its CEO Steven Sell step down, shrinking Part D exposure to <30%, and focusing on payor repricing for 2026. Its YoY cost trend ran near 6% (with inpatient and Part B oncology as main cost drivers) and ACO REACH remained profitable, making 2025 a repair year and 2026 a 'we've lost all trust so now you really have to prove it' year. Wouldn't be surprised to see agilon slink back to the private markets after this torrential beatdown quarter after quarter as the once high-flying growth story is now defunct. A case study in how sorely data - and timely data - is needed to manage risk populations across markets appropriately. |

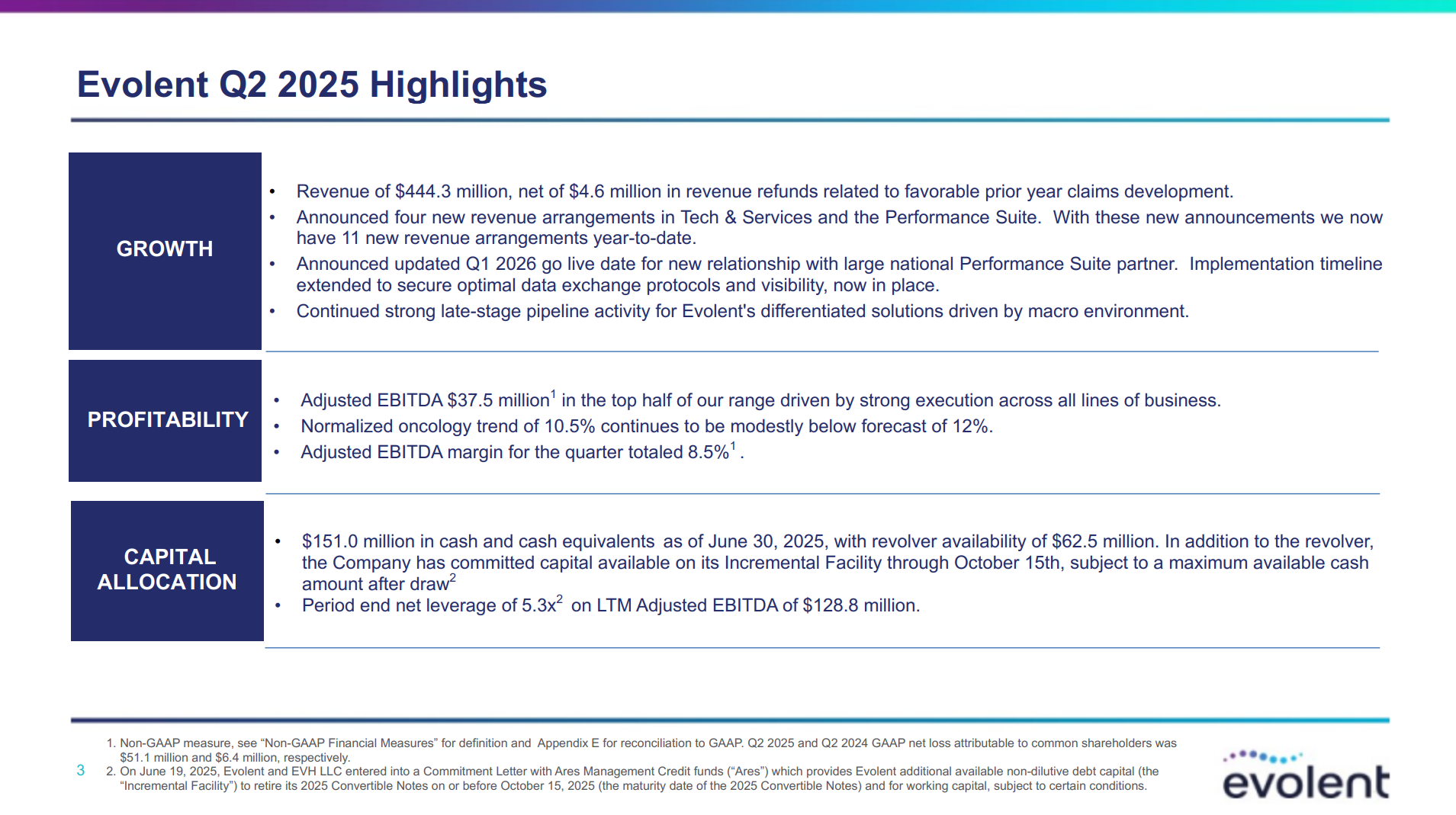

From a clinical program perspective, agilon is expanding burden of illness and quality programs with physician point of care tools, heart failure live in over half of markets, palliative program across most markets, and a push to see high risk seniors more often. Target is 4+ Star quality performance with readmit, admission, and ER rates 20% to 30% better than local FFS benchmarks in year 2+ maturity markets. Evolent Health outperformed on EBITDA, signed 4 deals including Aetna for 250k MA lives in Florida for Q1 2026, expanded a weighted pipeline that supports 2026 revenue >2.5B, and showed real AI lift with 11% review efficiency and a target of 80% auto approvals as oncology trend near 10.5% stayed below forecast and new performance suite contracts carry tighter corridors and data terms. |

P3 Health Partners, similar to agilon, showed some rust stemming from prior-period adjustments, declines in revenue and membership after exiting unfavorable markets, and 'underperformance of a single payor.' Overall the firm showed operational traction beneath prior period noise with 3 of 4 markets at breakeven or better, ED and readmit rates down, hospice and palliative savings visible, about 20M of payer contract improvements locked, and a possible 2026 adjusted EBITDA path of $120M-$170M tied to the MA rate lift, benefit rationalization, and tighter UM and specialty capitation. |

The Oncology Institute grew revenue 21% with pharmacy up 41% and improving margin while adding fully delegated oncology risk in Nevada Medicaid and expanding delegated MA in Florida and California, launching AI pilots in prior auth, RCM, and member support, and keeping the Q4 adjusted EBITDA positive target in sight as cap cohorts mature. My quick take: Value-based care as a whole is seeing themes of durability, visibility, and control in a post-pandemic, high-utilization environment. Partners and investors are asking similar questions…is your model sustainable? Do you have insight into what's happening within your populations and if not, why? How are you leveraging AI to move the needle for your care teams and improve your medical and care margins? What's the growth story, and how does your business fit in to the overall sustainability of value-based care? How can you be good partners to payors while also protecting yourself from delegated risk? We've definitely seen a marked shift between the 'haves' and the 'have not's' as far as … general growth story versus 'trying to survive in 2025.' |

|

|

SPONSORED BY TEAM CONNECT Has CMS put your hospital on the mandatory TEAM list? In January, 748 hospitals will enter CMS' Transforming Episode Accountability Model (TEAM), a high-stakes, 5-year alternative payment model for major surgical episodes. Participants will face increasing levels of risk and high expectations for reducing Medicare costs during a 30-day episode. Don't do it alone. TEAM Connect is a collaborative community created to help TEAM participants navigate episode-based payment models. Membership is free for hospital leaders, ACOs, and physicians and gives you access to webinars, discussion forums, and a national network of healthcare professionals who are operationalizing bundled payment models.

See if your hospital is on the list and join today!

|

|

|

My favorite reads & resources from the week |

*This read is brought to you by one of my brand partners who help make this newsletter possible! |

|

|

Random personal anecdotes and musings from me |

That's it for Tuesday! Keep your eyes peeled for a deep dive with Arbital Health tomorrow, then a lighter send Thursday. Thanks fam. And don't forget to register for the AMA next Tuesday. Register here. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 47,900+ executives and healthcare decision-makers. |

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments