Hospitalogists, Welcome to another grand edition of Hospitalogy where it's everyone's favorite season. Fall? What? No…hospital earnings season. C'mon guys - you know the drill by now! Let's dive in, starting with HCA. |

Was this email forwarded to you? |

|

|

Going deeper on an interesting topic, theme, or trend |

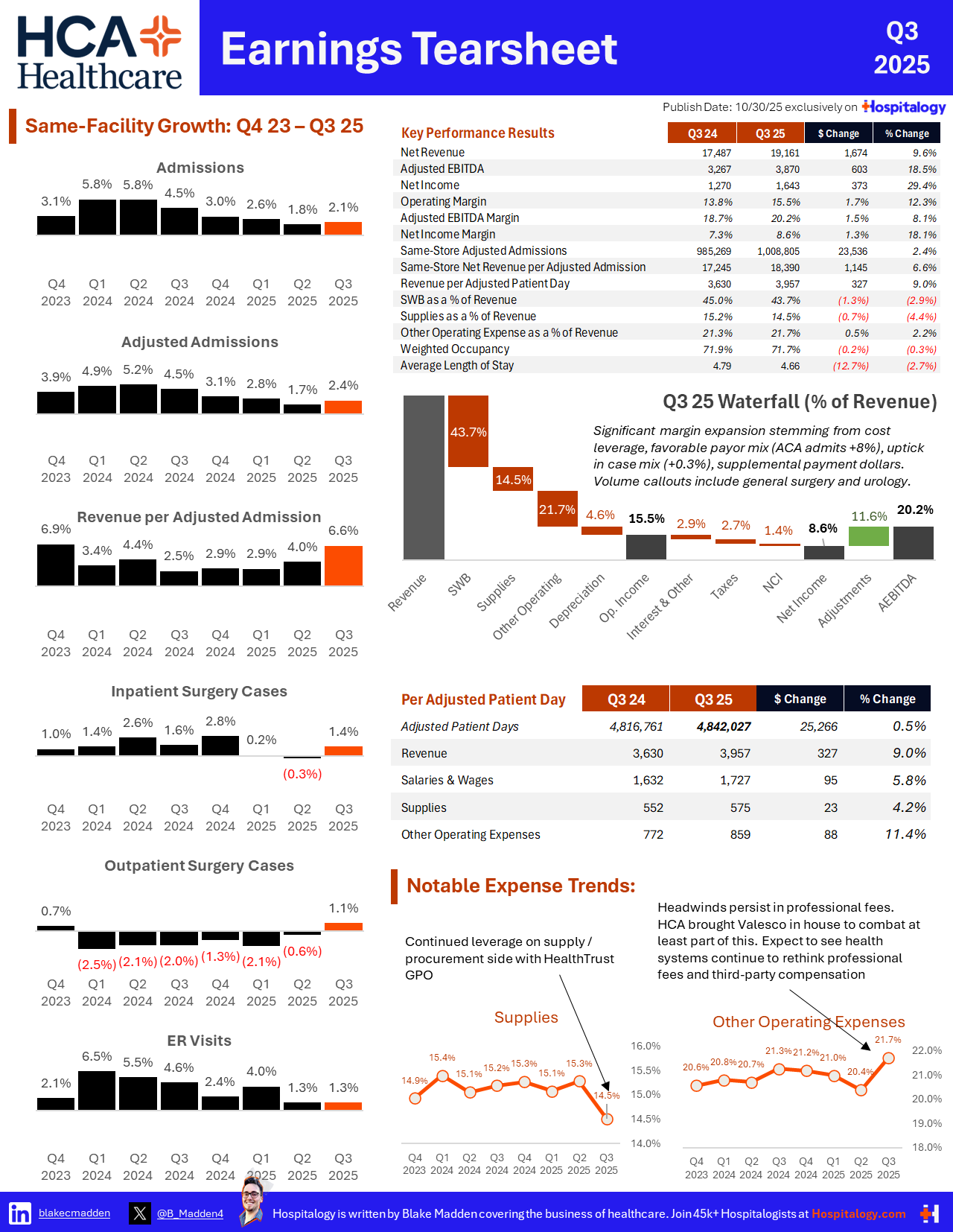

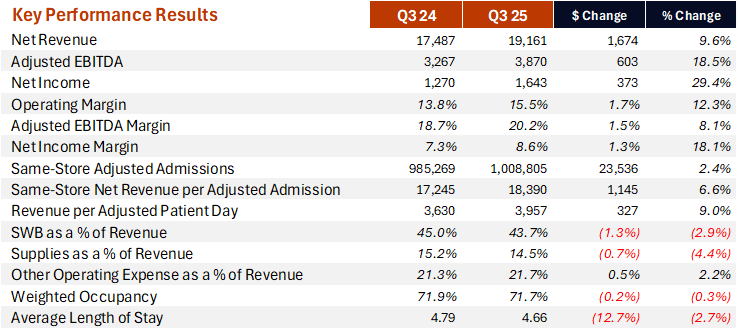

HCA Q3 2025 Executive Summary |

Overall, it was another business as usual quarter for HCA - the hospital titan - as near-term threats loom in 2026. HCA continues to churn out solid volume growth while the real bellwether for the $75B health system is its ability to command on price - both with a favorable payor mix, negotiation prowess, density in growing markets, and a focus on high acuity services (ortho, neuro, cardiology, and oncology). Opportunities and issues facing HCA and other hospital operators include the continued ACA subsidy dance, risk / reward around future supplemental payments dollars, ongoing health system transformation (ambulatory buildout, AI margin opportunities), and professional fees challenges (radiology). We'll get more color and quantifiable impact of the enhanced subsidies and more on HCA's Q4 report in February, post government shutdown, and when there's more visibility into what lawmakers actually do with these initiatives. For now, the for-profit hospital operator will enjoy its time in the sun. |

- HCA noted outpatient general surgery and urology as bright spots in volume growth during Q3 while most other service lines (ortho, IP cardiology) remained steady. Notable softness included outpatient gynecology and inpatient neurosurgery, despite broader neuro growth.

- Same-facility adjusted admissions finished up 3.7% with exchange volumes leading the way at 8% year over year growth. Other notable admissions info:

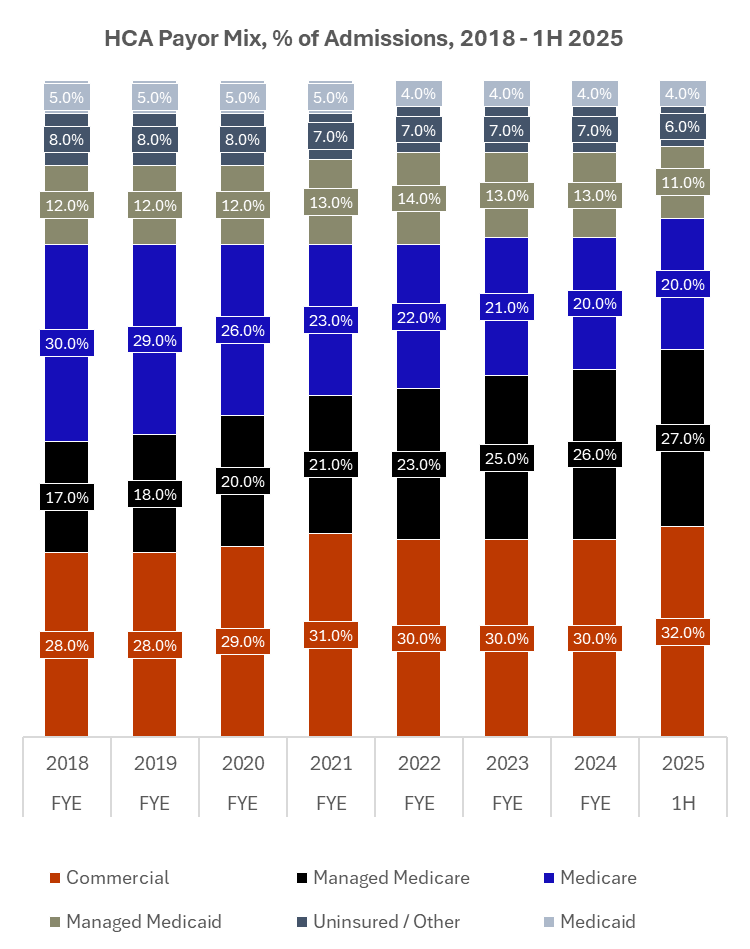

- MA admissions grew 4.8%, while Traditional Medicare grew just 0.9%. You can see this payor mix phenomenon happening across all hospitals. From 2018 to today, HCA's payor mix (as a % of admissions) went from 17% MA to 27% MA:

|

- From a capacity standpoint, there are no material labor‑driven capacity constraints at present. Length‑of‑stay management improved in Q3 and surge planning is in place for seasonal spikes.

- Key management quote: "Well, when we look at our outpatient surgery, we had strong general surgery activity. Our urological service line was very strong on the outpatient side. On the inpatient side, our neurosciences surgical capabilities, our orthopedic surgical capabilities, cardiac, all of these were up and had very good performance on a year-over-year basis. So again, diversification is a powerful element for us. diversification amongst these service lines, different mills use for delivering care to our patients, all of it sort of works as a system to create again the enterprise performance that we're able to produce. But those are some of the categories that moved favorably. We had a couple that weren't as positive. Again, that's par for the course from one quarter to the other and not really indicative of anything structural. Our gynecology business on an outpatient in the third quarter was slightly down. So that's one item that was down, but it was covered by some of these other areas. And then within the inpatient side, our neurosurgery business was down modestly, and that impacted the inpatient business, but it was overcome by some of these other areas." - Sam Hazen, HCA Q3 earnings call

|

Revenue Growth, Payor Mix, Reimbursement |

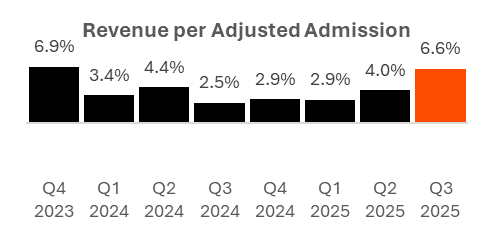

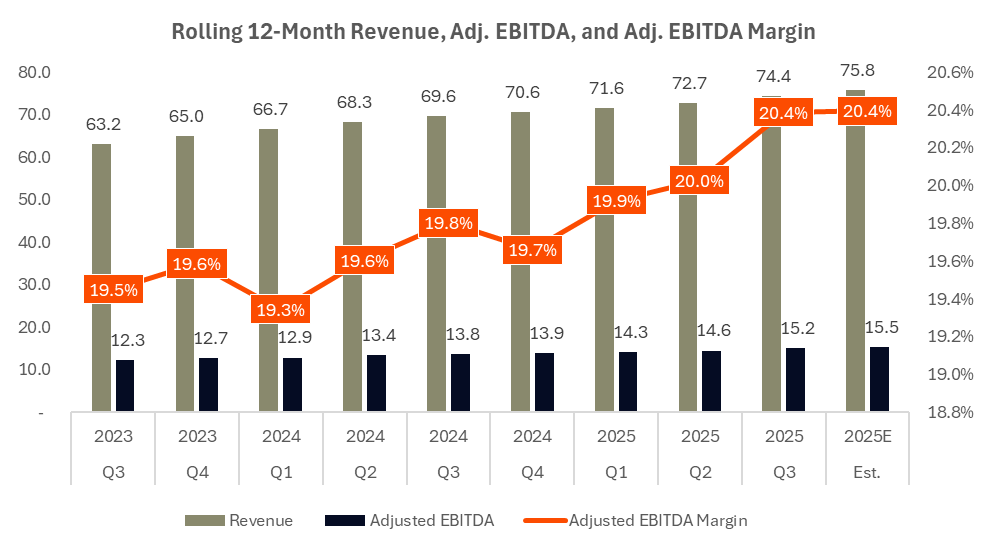

- Q3 revenue per equivalent admission up 6.1% year over year. Same‑facility revenue per equivalent admission up 6.6%. Inpatient revenue per admission up 6.3% reported and 7.1% same‑facility. Drivers were stronger payer mix, improved dispute resolution, consistent acuity, and higher Medicaid supplemental revenue. Same-store revenue per adjusted admission growth by quarter can be seen below. It's a pretty rich trend for HCA:

|

- Supplemental payments are a real earnings lever and a real risk. HALF of HCA's growth in net revenue per admit stemmed from growth in supplemental payments programs. Q3 adjusted EBITDA benefited by ~$240M from state Medicaid supplemental and directed payment programs, with the main impacting programs being Tennessee, grandfathered approvals in Texas and Kansas (meaning HCA booked all payments from these states from 2025 in Q3). Management raised full‑year guidance partly on an expected $250M to $350M year‑over‑year net benefit from these programs, but expects a decline in state supplemental payments in Q4.

- Case mix index ticked up 0.3% while payor mix was strong.

- HCA also noted its ability to win in dispute resolutions over payors in what stems from HCA's decision to go to battle with UnitedHealth in Florida alleging $145M in underpayments to 17 HCA hospitals.

- Key management quote: "…if you just think about kind of the walk up on state supplemental payment programs and you apply that to our full-year guidance, I think that gives you a sense that now we're expecting it to be $250 million to $350 million, favorable full-year '25 to full-year '24. And that gives you a sense of our kind of our early thinking as we kind of finish guidance right here, this is where we think the year will come in at this point. I did note, and there's a lot of volatility here, that guidance update does not include any additional impact from any other state supplemental payment programs that may get approved by CMS in 2025 once the government reopens. So just keep that in mind as well." - Mike Marks, HCA Q3 25 earnings call

|

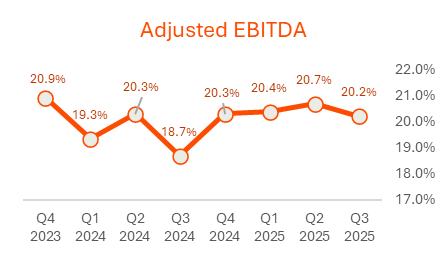

- Adjusted EBITDA margin expanded to 20.2% in Q3 from about 18.7% in Q3 last year, supported by labor and supplies performance and the supplemental revenue tailwind.

|

- Labor normalization is holding. Same‑facility contract labor was essentially flat year over year and was 4.2% of total labor cost. HCA is now squeezing professional fees and supplies while using scale tools like HealthTrust and digital workstreams to protect margin. One quick note on contract labor - it ticked up just barely - by 0.2% of salaries & wages - in Q3 sequentially from Q2. It's pretty minor, but I do think it's notable from the perspective that it probably signals the bottoming out of the labor market.

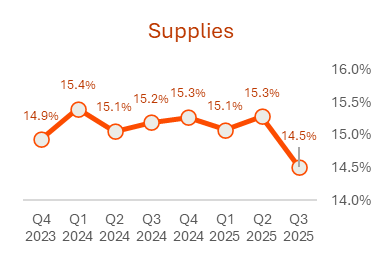

- On the supplies and other expenses front, HCA continued to show strong leverage over supplies and procurements and noted its effectiveness with renegotiating contracts with its GPO, HealthTrust, while deploying technology in meaningful areas. For supplies in general, HCA isn't concerned / is seeing very minimal impact of tariffs.

|

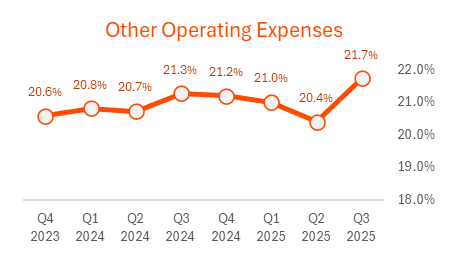

- What's most notable in the expense category is HCA's - and every hospital's - ongoing challenge to tackle professional fees and teh cost structure of anesthesia, radiology, and other hospitalist functions. HCA has mentioned Valesco is a $40-50M drag to profitability, and this trend continued in Q3. Same-facility prof fees increased 11% (1% sequentially). Prof fees as a whole comprise ~24% of HCA's other operating expenses and you can see the small spike caused by this dynamic below in the financials. Overall, HCA is optimistic about the ability to manage this expense moving forward as they more deeply integrate Velasco into HCA-specific workflows and throughputs optimizations.

|

- Key management quote: "…to HealthTrust, a lot of effort in flight on our contract renewal cycles. We tend to run 2-year cycles, some contracts as many as 3. And so those renewals flow as follows. And we spend a lot of effort in those contract negotiations, and that's certainly one component of our supply expense annual trends. The second component would be mix of technology. And so as you're aware, every year, there's new technology coming in. And then there's management of technologies that goes through its maturation cycle that's a big part of our overall management routines. The third part of our resiliency plan is our efforts to manage utilization. And so we have a very active resiliency plan. Supplies is one of those areas that we are continuing to both enhance and accelerate our resiliency plans focused on appropriate management of supplies and the utilization of supplies throughout the platform. As I think about bridging into the future, the other component that we're keeping a close watch on our tariffs, where our HealthTrust team continues to work through a very diligent effort to manage the tariff risk. Both in terms of sourcing, the way that we negotiate with contracts, our vendor partners on contracts and then also in terms of moving products and moving choices of products across countries of origins." - Mike Marks, HCA Q3 25 earnings call

|

Capital Allocation, M&A, and Partnerships |

- HCA continues to hover at the lowest end of its leverage target. It has repurchased significantly more stock in 2025 - about $3B more, if my math is right, than 2024 - while CAPEX will remain flat at ~$5B for the year, or about 6.6% of total net revenues.

- On the facility development front, HCA is chasing more tuck-ins and de-novo growth, aiming for a target of 15+ ambulatory nodes / care settings per hospital in its markets.

- Key management quote: "There's 3 or 4 things I would note that are driving our strong cash flow from operations as we think about it. One certainly is just we've had really solid adjusted EBITDA growth. And that strong operational performance that we continue to highlight as we think about the strength of our revenue cycle operations with Parallon, we turn that revenue into cash. And so that's a piece of that. And you're seeing that in kind of our working capital management plans. We have a pretty robust working capital management strategic plan that includes not only net days in ARR, but includes things like inventory levels, prepaid levels. And that work around working capital continues to assist us as we think about growing our cash flow. The other point, and I made this on the call, but it's important to note is that year-to-date, we have been able to defer $1.3 billion of estimated federal income tax payments to the fourth quarter. And so keep that in mind as well. But when I think about the long term, this idea of clearing out your revenue with cash and the strength of Parallon and our revenue cycle operations and the strength of the working capital management plans of the company, I think, puts us in good stead for continued strong management and performance around cash flow into the future."

|

Innovation and Technology |

- AI is moving from pilot to P&L. Two immediate use cases are ambient clinical documentation (Commure / Augmedix) and automated denial and underpayment workflows in revenue cycle. As we've discussed, expect sustained payor pushback on coding intensity as they're hyper aware of what's going on in the space with AI. HCA responded to this criticism by saying the ROI for AI in these arenas lives in administrative throughput and billing recovery rather than up‑coding. The company's broader digital transformation is woven into its resiliency program (quantified at $600M-$800M in improvements back in November 2023) and shared‑services scale.

- Key management quote: "…our coding practices remain consistent and accurate as verified by multiple layers of audits. Specifically related to AI, we do -- as Sam mentioned, we're deep into our efforts around digital transformation across our company, including in our revenue cycle. Our focus in terms of AI automation and our revenue cycle right now is really specifically focused on working to respond to the growing denial and underpayment activities from the payers. We have noted before, we are also both piloting and rolling out ambient AI documentation tools designed to help our physicians be more complete, more accurate and more timely in completing their clinical documentation. So that's a quick update of what we're seeing in the utilization space." - Mike Marks, HCA Q3 25 earnings call

|

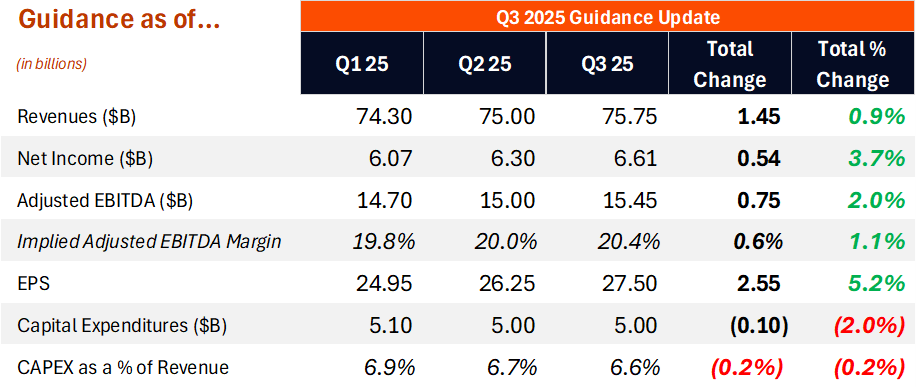

- The above table displays midpoint figures from each guidance update related to HCA's quarterly reports. Stemming from a strong payor mix, favorable updates in state supplemental programs, strong acuity, increasing volumes, and continued expense leverage, HCA has bumped up its guidance multiple times in 2025.

- Despite aforementioned headwinds (literally) in hurricane season and supplemental payment programs, HCA's implied growth rate in Q4 expects to hit around 7%.

- 2026 outlook: Solid, stable demand across HCA markets in line with 2-3% long-term growth. Stable expense trends consistent with past couple of years. We'll get more insight on outlook after Q4 reports once the federal government situation gets clarified.

- Key management quote: "One of the things we talked about at our investor conference back in November of '23 was what I term the staying power of HCA Healthcare. And that staying power is really connected to 3 points. One, the relevance of our systems within the communities that they serve. The second thing is the scale across the company when it comes to just the sheer size of HCA Healthcare. The third aspect to that is the diversification. And so you're hearing about how the diversification provides what I call staying power for our organization, allowing us to push forward with our agenda, produce solid returns on our capital and create better outcomes for our stakeholders." Sam Hazen, HCA Q3 25 earnings call

|

|

|

Happy Halloween! Baby Madden is going as a construction worker. He's in a huge excavator phase right now and can, of course, name all of the various types of equipment and machinery. This morning he took off sprinting down the sidewalk looking for sites to excavate for his newfound important role. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 49,000+ executives and healthcare decision-makers. |

I'm building a community of leaders in strategy, finance, and ops

at hospitals and health systems to help us connect, learn, and grow together. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments