PARTNERED WITH  |

|

|

Happy Thursday Hospitalogists! As we round out hospital earnings season, I couldn't miss Ardent. Ardent is facing one of the tougher operating environments as a smaller health system in secondary markets with exposure to supplemental payment reform, ACA subsidies, and retention and recruitment on the professional fees side. The struggles will persist into Q4 and investors weren't happy. Hospitalogists can learn a lot about the 2026 hospital environment from Ardent's Q3. Let's dive in! |

Was this email forwarded to you? |

|

|

SPONSORED BY SMARTERDX Looking for an AI partner that gives you real results? It's important to start with the metrics that matter.

Financial metrics. Operational metrics. Quality metrics. That's why SmarterDx compiled an RCM leader's guide to cut through the noise and get to the numbers… so you know if the AI you're considering really works. Complete with an easy-to-use checklist, this is a benchmark for what real AI impact looks like and the questions you should be asking to get the most out of an AI partner. Before you put ink to paper, get this guide to help RCM teams assess potential AI partners and uncover the real impact an AI solution can have for your hospital. |

|

|

Going deeper on an interesting topic, theme, or trend |

Ardent Health Q3 2025: Volume Can't Save Margin When Industry Headwinds Intensify |

Executive Summary: Demand Strong, Economics…Broken? |

A 2 out of 10 quarter for Ardent, with potential to get worse from here. Volumes are fine, payors are playing hardball with rates and denials, looming regulatory headwinds, rising professional fees, expectations for an even worse Q4 all loom large for a hospital operator facing systemic pressures without much of an ability to answer these challenges in the way of actual operating or strategic maneuvers.

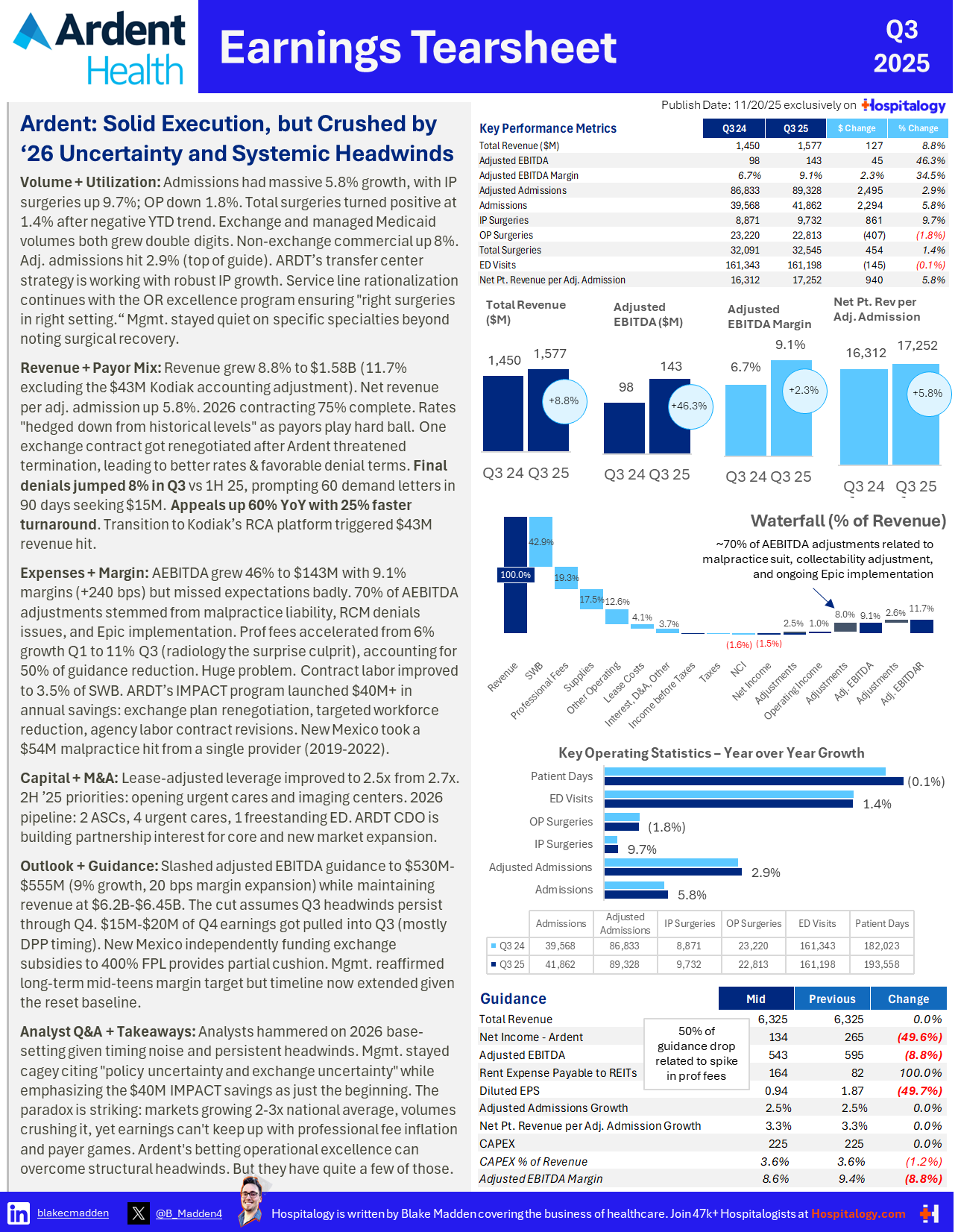

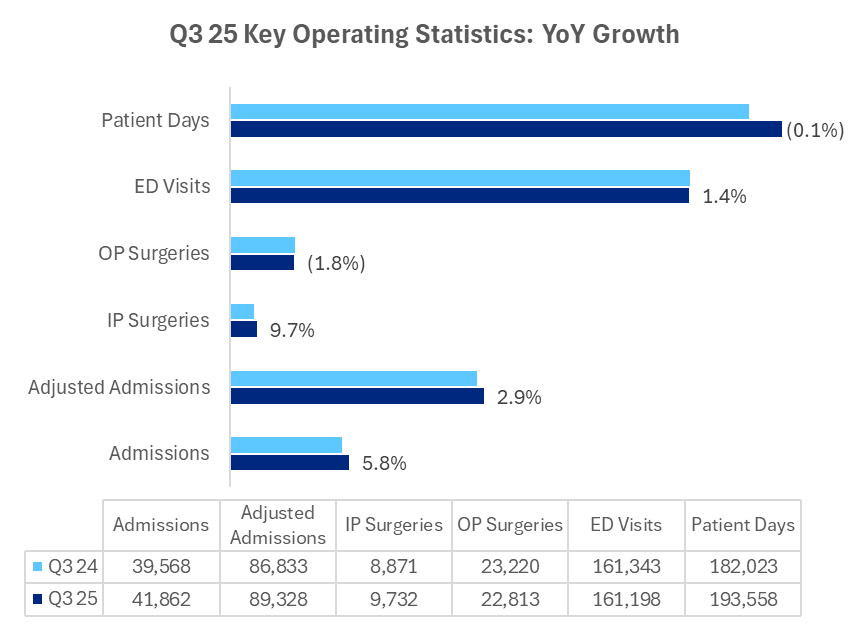

Ardent Health delivered one of the more paradoxical quarters in recent hospital operator history: 5.8% admissions growth and 46% adjusted EBITDA expansion year-over-year, yet still missed expectations badly enough to slash full-year guidance to $530M-$555M from implied higher targets. The company's Q3 reveals a sobering reality facing mid-market operators today: strong volumes and disciplined execution can't overcome structural headwinds when professional fees accelerate instead of moderate and payer denials intensify rather than stabilize. |

The guidance cut reflects two persistent industry pressures that worsened throughout Q3 and scared investors so much that the stock dropped 30%+ on the day post-earnings. Professional fees accelerated from 6% growth in Q1 to 11% in Q3 (radiology emerged as 2025's pressure point after ER and anesthesia dominated prior years), accounting for roughly 50% of the EBITDA reduction. Payer denials jumped 8% in Q3 versus the first half of 2025 after appearing to stabilize earlier in the year, forcing Ardent to file 60 demand letters in 90 days seeking $15M in recoveries while increasing appeals 60% year-over-year. Still, Ardent is executing just fine. At 9.1% adjusted EBITDA margins (240 bps expansion) with 9% growth at the midpoint of revised guidance, Ardent's performance isn't catastrophic. The company operates in markets growing 2-3x faster than national averages, maintains lease-adjusted leverage of 2.5x (down from 4.0x at IPO), and generated $154M operating cash flow versus $90M prior year. But the earnings miss and guidance reduction exposed a notable, diverging dynamic: geographic market selection and operational excellence matter less when systemic external pressures, like professional fee inflation and payer behavior (denials), overwhelm traditional hospital management strategies. Ardent's response centers on its IMPACT program, targeting $40M+ in annual run-rate savings through exchange contract renegotiations, targeted workforce reductions, and agency labor rate revisions. The company successfully renegotiated one troubled exchange contract after threatening early termination, securing better rates and terms to prevent denial activity. Management emphasized the shift from pursuing headline rate increases to tightening contract terms that prevent technical denials and payment slowdowns. Yet even with these initiatives ramping through Q4 and into 2026, the fundamental question remains whether $40M in identified near-term savings can offset professional fees growing low double-digits and payer denials showing no signs of abating. The quarter also featured two significant non-recurring charges: a $43M revenue adjustment from transitioning to Kodiak's RCA platform (recognizing reserves earlier in accounts' lifecycles) and a $54M professional liability reserve increase in New Mexico (100% attributable to a single provider from 2019-2022 and social inflation pressures). While excluded from adjusted EBITDA, these items highlight operational complexity and market-specific risks that can create unexpected accounting headwinds even when improving underlying capabilities. |

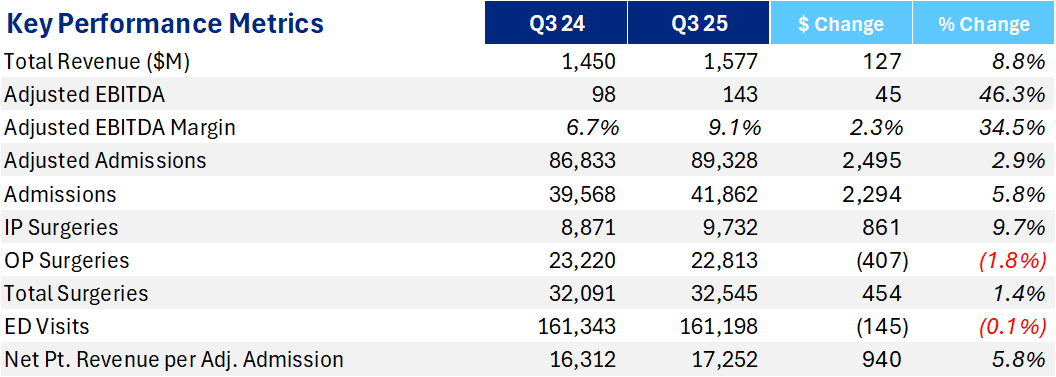

The paradox continues. Ardent crushed volume targets across nearly every metric in Q3, demonstrating the power of its geographic positioning and transfer center strategy. Admissions grew 5.8% in the quarter and 6.7% year-to-date, significantly outpacing its 2-3% population growth in its markets. Adjusted admissions increased 2.9% in Q3, landing at the top end of 2-3% full-year guidance and up 2.4% year-to-date.

The surgical volume story marks Q3's most encouraging operational shift. Total surgeries turned positive at 1.4% growth after declining 0.7% in Q1 and 0.2% in Q2. Inpatient surgeries exploded 9.7% while outpatient surgeries fell 1.8%, creating a clear acuity mix improvement. Management attributed this reversal to transfer center initiatives successfully capturing higher-acuity cases and the OR excellence program ensuring "right surgeries in right setting" through ongoing service line rationalization.

Payor class dynamics drove much of the volume strength. Exchange volumes grew double-digits (management called out 35% year-over-year growth on the Q2 call, with double-digit continuation in Q3). Managed Medicaid also jumped double-digits while non-exchange commercial climbed 8%. This mix evolution matters given Ardent's exposure to exchange subsidies and managed care penetration, creating both growth opportunities and reimbursement complexity as the company navigates 2026 contracting cycles.

Ardent operates in fundamentally advantaged markets growing 2-3x faster than national averages with sustained demographic tailwinds and rising care complexity. The 6.7% year-to-date admissions growth against 2-3% population expansion suggests the company is capturing meaningful market share through its transfer centers and outpatient access point expansion. Yet this volume strength makes the earnings disappointment more striking: Ardent is winning on utilization and losing on economics, a dynamic that transcends operational execution and reflects structural industry pressures. |

Revenue + Payor Mix + Acuity |

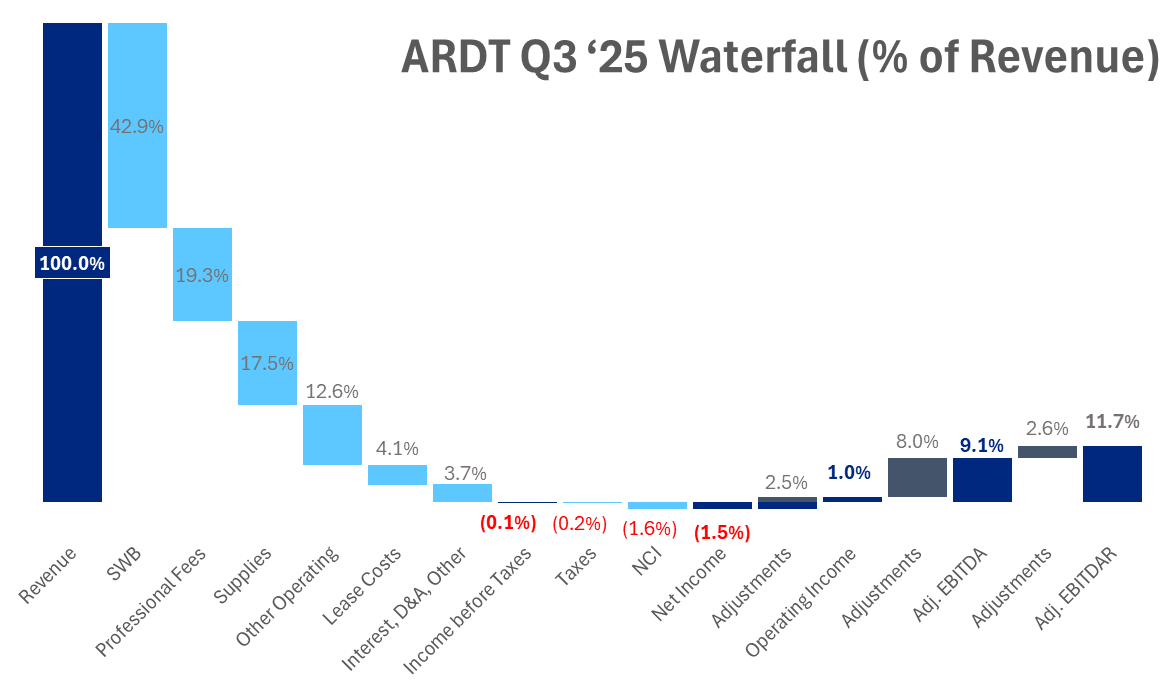

Revenue grew 8.8% to $1.58B in Q3, or 11.7% excluding the $43M Kodiak accounting adjustment. Net patient service revenue per adjusted admission increased 5.8%, driven by acuity mix improvements and contracted rate increases. Full-year revenue guidance remained intact at $6.2B-$6.45B (6% growth at midpoint), reinforcing that Ardent's top-line momentum persists despite earnings pressure. Topline remains important for debt servicing. Keep that in mind.

During Q3 Ardent transitioned to a new RCA platform - Kodia. The transition created a one-time $43M revenue reduction by recognizing reserves earlier in accounts' lifecycles compared to Ardent's previous internally developed model that utilized a 180-day cliff methodology. So basically a more conservative estimate for the potential collectability of accounts. Ardent management wanted us to know that this change is simply an alteration of reserve timing and doesn't represent underlying rev cycle performance, and future results from both models should align. The platform serves 2,100+ hospitals and provides enhanced real-time reporting capabilities, positioning Ardent for improved revenue cycle management as it scales. The adjustment notably reduces reported revenue for Q3 but (of course!!) gets excluded from adjusted EBITDA calculations.

On the payor negotiation front, 2026 contracting status reached ~75% completion, up from 55% last quarter, with rates "hedged down from historical levels" and "closer to traditional type increases" per management. Translation: payors are tightening the screws and Ardent is accepting more modest rate escalation than historically achieved, though execs on the call indicated they'd be revisiting contracts and certain terms in the coming years.

Payer denial dynamics worsened materially throughout Q3. Final denials jumped 8% versus H1 2025 averages after appearing to stabilize through early 2025. Management described denial pressures as widespread across managed products (Medicare Advantage, managed Medicaid, exchanges) rather than concentrated with specific payers. Ardent responded by filing 60 demand letters in 90 days seeking $15M in recoveries, increasing appeals 60% year-over-year while cutting turnaround time 25%. The company reorganized internally to integrate revenue cycle, legal, and contracting teams into a multidisciplinary response unit leveraging advanced analytics to reduce denials.

Despite holding #1 or #2 market positions across most markets, management emphasized Ardent remains "the value-based provider" in those geographies, suggesting limited pricing power against consolidated payer bases. This creates a revenue ceiling even as volumes grow: Ardent can capture market share and higher-acuity cases but faces constraints on rate realization and increasing payer tactics around denial activity and payment timing that erode net yield regardless of contracted rates. |

Adjusted EBITDA grew 46% to $143M with 9.1% margins (2.3% expansion). These figures, while representing strong year-over-year improvement, fell meaningfully short of expectations and triggered the guidance reduction to $530M-$555M for full-year 2025. More on that in a bit. Very notably, Q3's adjusted EBITDA figure includes a pull forward of $15M-$20M of earnings previously expected in Q4, stemming from directed payment program timing. Excluding this benefit, underlying Q3 performance would have been even worse. Ringing the investor alarm bells and raising some eyebrows, Ardent executives assumed Q3 headwinds persist through Q4 at elevated levels when establishing revised guidance. Here's the breakdown on expense trends, with the big one being professional fees. Professional fees is a huge talking point right now among hospitals and health systems, and Ardent's exposure was no different. The expense trend here emerged as the dominant headwind, accounting for roughly 50% of Ardent's guidance reduction (!!!). Over the course of the year, Ardent had expected prof fees to mitigate and decelerate. But rather than moderating as anticipated, professional fee growth accelerated: 6% in Q1, 9% in Q2, 11% in Q3, with second-half expectations now low double-digits versus previous high single-digit assumptions. They called out radiology specifically as 2025's primary pressure point after ER and anesthesia dominated prior-year discussions. So it sounds like there's not a ton of visibility or ability to get a handle on the situation. Maybe it's time for some investment into AI-enabled radiology functions! Who knows! Ardent also noted they're negotiating more flexible cost structures aligned to volume and strategically replacing contract labor here with full-time hires to right-size professional fee structures, though these efforts take time to manifest. Also, it's notable that Ardent's market selection probably plays a role here with recruitment and retention efforts. Labor pools are structurally smaller in the markets Ardent chooses. They're not always in the big cities. Other labor metrics showed continued discipline with salaries and benefits improving to 42.9% of revenue from 43.8% a year ago. Contract labor, as mentioned on other earnings reports, is at a valley and declined again to 3.5% of salaries and wages from 3.8% in Q1/Q2 and 3.9% from last year. The quarter also included a $54M malpractice case that seems to have gotten out of hand. The case is 100% attributable to ONE provider in New Mexico - a single provider Ardent hasn't employed for several years (2019-2022) plus overall social inflation pressures in that market. Ardent talked about how New Mexico is experiencing significant medical malpractice cost escalation for multiple years with increasing premiums and case sizes. The charge gets excluded from adjusted EBITDA but still…ONE provider causing a $54M hit to profitability in the quarter is nutso. And you wonder why healthcare costs so much when things like malpractice are baked into price. Market-specific tail risks can create unexpected charges even after provider relationships end. Even for a single provider. On the mitigation and initiatives front, Ardent needed to have a response ready for investors, and they did. The hospital operator launched its IMPACT program to drive efficiency across 7 buckets: revenue integrity, productivity, payer disputes, supply chain management, purchased services, RCM, and …of course…professional fees. 3 near-term initiatives already underway include the exchange contract renegotiation detailed earlier, targeted workforce reduction, and agency labor contract revisions lowering base rates and premium pay. Ardent expects these three actions alone to generate $40M+ in annual run-rate benefit by early 2026. Additional initiatives include precision staffing, supply chain vendor consolidation, and OR excellence program service line rationalization. Still…$40M in near-term identified savings feels pretty bleak against the headwinds Ardent is facing entering 2026. They're staring down at the cliff. Professional fees alone created roughly half the guidance reduction, and payor denials continue worsening with no clear stabilization signal. Analysts pressed repeatedly on whether initiatives within Ardent's operating and strategic control can overcome external pressures - and that's a huge tell that calls into question Ardent's ability to weather the storm that could potentially flip the boat whether you build the Titanic or row out in a fisherman's boat. Time to start praying. Sometimes things are just out of your control. |

Capital + M&A + Partnerships |

On the plus side, Ardent ended with a net leverage position of 2.5x - from 2.7x in Q2 and 4.0x at IPO.

For now, the balance sheet provides meaningful flexibility for strategic growth investments despite near-term earnings headwinds. 2H 2025 development includes several urgent care and imaging center openings in typical hospital expansion fashion. The 2026 pipeline entails 2 ASCs, 4 urgent cares, and 1 FSED. Management reaffirmed its strategy of developing 10 ambulatory access points per hospital to capture downstream revenue and expand market reach. In comparison, HCA is at 14-15 and is well on its way to 20 access points.

Ardent has accelerated activity in building partnership interest for both core market expansion and new market entry opportunities. Pretty unique to Ardent is its JV model that attracts growing interest given industry consolidation pressures and the capital requirements for independent operators to compete effectively. To date, we haven't heard of any major partnerships or JVs materializing.

When analysts pressed on capital deployment priorities given $900M available liquidity and earnings pressure, Ardent indicated share repurchases are not currently under Board consideration. Management emphasized commitment to "optimizing shareholder value" but clearly prioritizes growth investments and balance sheet flexibility over returning capital to shareholders at this stage. Makes sense and is yet another signal toward conservatism and doomsday prep. Ardent also maintained a 4% of revenue CAPEX target (up from historical 3%) to support urgent care and imaging network expansion.

Notably absent from the quarter: any meaningful technology or innovation discussion beyond the Kodiak revenue cycle platform transition. No AI deployment commentary, no digital health partnerships, no care model innovation updates. This stands in contrast to larger operators discussing ambient scribes, virtual nursing, and technology-enabled efficiency programs. I'm sure under the hood there's plenty of activity (especially given Ardent's footprint is on a single instance of Epic, which is closely aligned with Nuance), but Ardent's focus remains squarely on traditional hospital operations and outpatient access point expansion rather than technology-driven transformation. |

As mentioned, Ardent slashed adjusted EBITDA guidance big time, to $530M-$555M, reflecting persistent professional fee and payor denial pressures that worsened throughout Q3 rather than moderating as anticipated. The midpoint implies 9% EBITDA growth with 20 bps margin expansion, which is still respectable but well off its earlier expectations. The revised guidance assumes Q3 headwinds continue through Q4 at elevated levels. Big problem. Looks like Ardent IPO'd near the top, eh? Looking toward 2026, Ardent declined to provide formal guidance but outlined several considerations: - The IMPACT program should deliver $40M+ annual run-rate benefit from near-term initiatives with additional savings ramping throughout the year.

- Professional fees and payor denials are expected to remain elevated without clear moderation signals.

- Exchange subsidy uncertainty creates policy risk, though New Mexico announced it will independently fund enhanced subsidies to 400% of the federal poverty line.

- Management reaffirmed belief in achieving mid-teens EBITDA margins longer-term but acknowledged the reset baseline extends that timeline. This reset presents credibility issues for Ardent moving forward. Now it turns into "prove it" mode.

To wrap it all up, Q3 was a pretty terrible quarter for Ardent leaving many questions to be answered, which sparked a selloff. Policy dynamics loom large for 2026 planning and present plenty of uncertainty as one of the most exposed hospital operators to OB3, Medicaid cuts, ACA subsidies. OB3 legislation creates regulatory uncertainty (Ardent has previously noted that worst-case OB3 impact was $150M-$175M after 2030). Behavioral health workforce constraints limit growth opportunities in that service line (similar dynamic facing UHS). The rural transformation fund represents a potential tailwind pending implementation details. Exchange subsidy expiration risk partially mitigates through state-level actions like New Mexico's, though exposure remains meaningful given Ardent's double-digit exchange volume growth they claim has minimal impact on the business. Rates are decelerating rather than the more aggressive escalation seen in prior cycles with inflation baked in. The rate moderation combined with tightening contract terms suggest Ardent is accepting current market realities around constrained pricing power. Can Ardent overcome its local market realities? Shoot me a note with your thoughts on the no good, very bad quarter for the most recently IPO'd hospital operator. |

Analysts hammered on 2026 base-setting throughout the Q&A, reflecting skepticism about recovery potential given persistent headwinds and Q3 timing noise. Management stayed measured, emphasizing "policy uncertainty and exchange uncertainty" make formal 2026 guidance premature while highlighting controllable IMPACT initiatives as the primary earnings recovery lever.

When pressed on professional fee dynamics, Ardent explained the cyclical specialty-by-specialty pressure pattern: ER and anesthesia dominated prior years, while radiology emerged as 2025's culprit. The company is negotiating more flexible cost structures aligned to volume and replacing locums with full-time hires, though these efforts require time to manifest across contract renewal cycles. Management expressed confidence that lapping through most specialty renewals provides better visibility for moderation ahead.

Payer denial specificity drew multiple questions. Management clarified denials are widespread across managed products (Medicare Advantage, managed Medicaid, exchanges) rather than concentrated with specific payers. The 8% Q3 jump versus H1 reflects payers getting "more aggressive at unilaterally either down quoting claims or flat out denying claims." Ardent responded with 60% more appeals filed, 25% faster turnaround time, and 60 demand letters in 90 days seeking $15M. The reorganization integrating revenue cycle, legal, and contracting teams into a multidisciplinary response unit represents a structural shift in how Ardent combats payer behavior.

The growth versus margin trade-off surfaced as analysts questioned whether volume growth creates margin pressure. Management emphasized service line rationalization and the OR excellence program ensure focus on high-acuity cases in appropriate settings. The 9.7% inpatient surgery growth versus 1.8% outpatient decline demonstrates acuity capture, though the earnings miss suggests revenue yield challenges overwhelm volume and acuity gains.

Capital deployment questions revealed no current share repurchase consideration despite $900M liquidity. CFO Lumsdaine emphasized Board commitment to "optimizing shareholder value" but clearly prioritizes growth investments over returning capital. This stance reflects either management conviction in growth opportunities or recognition that buying back shares following an earnings miss and guidance cut would signal limited confidence in near-term recovery.

The exchange contract renegotiation example stood out as a tangible IMPACT program win. After threatening early termination on a contract seeing significant margin erosion from denial activity, Ardent secured better rates, denial prevention terms, and a 2027 step-up provision. Management framed this as one example of the revenue integrity work underway, though acknowledged these renegotiations take time and can't immediately offset Q3/Q4 headwinds.

Most striking throughout analyst dialogue: the paradox of strong operational execution producing disappointing financial results. Ardent is winning on volumes, capturing market share, improving surgical mix, and generating strong cash flow. Yet professional fees accelerating to low double-digits and payer denials jumping 8% in a single quarter overwhelm these operational wins. The $40M IMPACT program feels like bringing a knife to a gunfight when structural industry headwinds intensify rather than moderate. |

|

|

Nabla is looking to hire across multiple roles - here are a few to consider for Hospitalogists: |

|

|

Texas vs. Georgia post-mortem: a good old fashioned a** whooping. I've never seen a team so hopelessly outcoached. We start every away game hungover, multiple drops, busted coverages, and expect to compete with the best of the best with elite athletes all over the field? Serious credit to Kirby for getting his guys ready (they always get up for big games) and completely taking the game away through coaching decisions. As a Texas fan, it was utterly deflating to watch the 4th quarter and Arch (who played an incredible game all things considered) sit on the bench for 10 minutes. Better luck next week against Arky and we have an incredibly outside chance at making the playoff - and we don't deserve that at this point in the year |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

| |

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 50,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments