PARTNERED WITH  |

|

|

Happy Tuesday Hospitalogists!

We're continuing the hospital Q3 earnings series with Community Health Systems (CHS), then we'll round out the next two with UHS and Tenet. Let's dive in! |

Was this email forwarded to you? |

|

|

SPONSORED BY WELLSKY The real cost in value-based care? Missed opportunities during transitions.

Risk-bearing organizations are being asked to control cost and improve outcomes, often without the tools or visibility to do it. A new tip sheet offers three actionable ways to manage cost before, during, and after care transitions, including: Real-time visibility across the care continuum Earlier, smarter discharge planning Dedicated clinical teams closing the gaps between handoffs One ACO reduced 60-day readmissions by 8% and SNF stays by a full day using this approach. Bonus: Patients were 4x more likely to be discharged to high-performing SNFs. Add these 3 strategies to your VBC playbook and execute smarter transitions to drive both clinical and financial results.

|

|

|

The most important news from the week |

Community Health Systems (CHS) Q3 2025 Earnings Analysis: The Same Tune, or a New Song? |

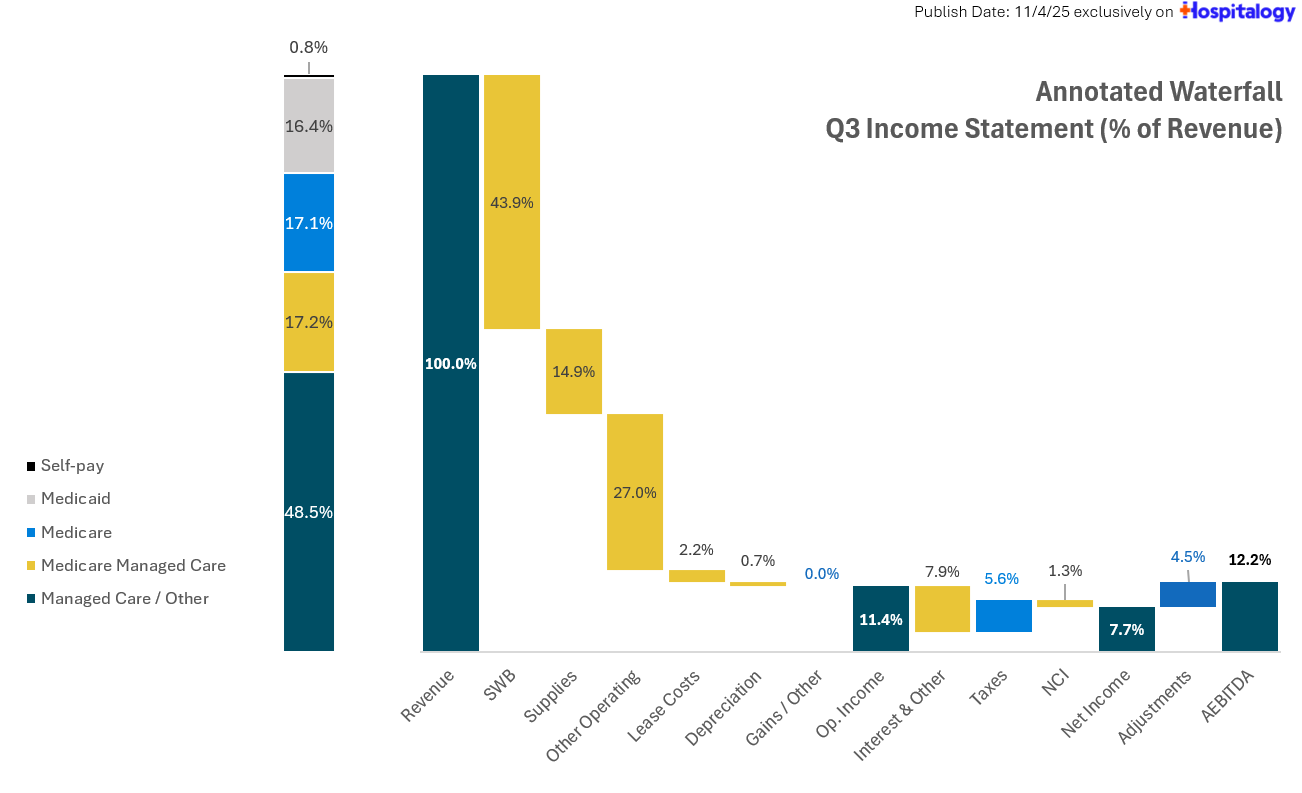

Overall, CHS continues to play its same tune ever since I've entered healthcare - high debt loads, cost containment struggles, then divestitures, then signs of promise, execution on that promise…then rinse and repeat. I hesitate to believe the narrative until CHS shows some ability to compound its results, and you can see why the stock itself has traded sideways for several years despite a favorable hospital environment. CHS delivered a stable third quarter built on rate and mix strength, expense control, and incremental operational improvement. Despite surgical softness, CHS eked out year-over-year margin expansion and maintained momentum toward positive free cash flow. Management attributed outpatient weakness to muted consumer confidence and macro softness in certain markets. Similar to HCA, CHS saw strong growth in reimbursement stemming from better payor mix dynamics and supplemental payments increases. Same-store net revenue climbed 6% year over year, with net revenue per adjusted admission up 5.6%. About a third of that increase came from Medicaid state-directed payments in Tennessee and New Mexico, with the rest from rate and commercial mix improvements. Acuity remained slightly diluted due to orthopedic and cardiac softness. CHS contained expenses and expanded adjusted EBITDA margins 20 basis points year over year. Supplies hit ~15% of net revenue, down 20 basis points, while contract labor trended lower and hourly wage growth stayed within expectations. Medical specialist fees grew 4% year over year to $165 million, representing 5.4% of net revenue. |

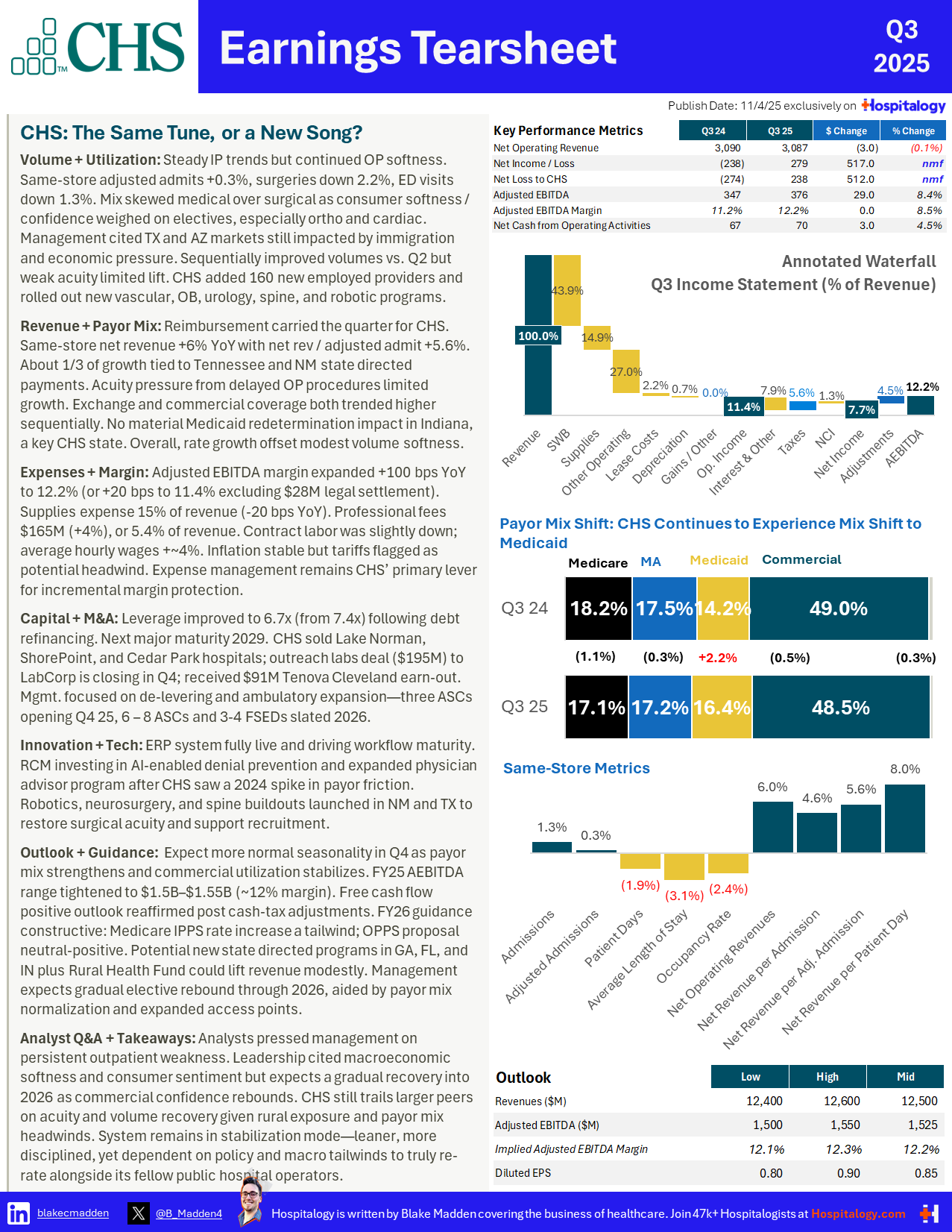

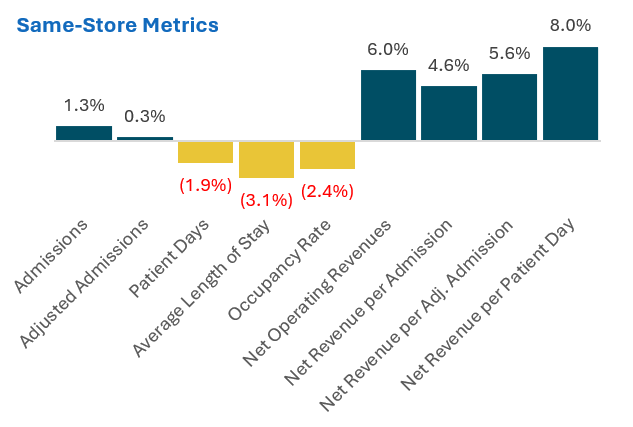

Volume growth in Q3 reflected a familiar story - steady inpatient activity offset by weaker outpatient performance. Inpatient admissions rose 1.3%, adjusted admissions were up 0.3%, and surgeries declined 2.2%. Outpatient electives, particularly in orthopedics and cardiac, lagged due to consumer caution and uneven recovery in certain markets. Emergency visits decreased 1.3%, though much of that decline came from uncompensated care, which cushioned the EBITDA impact.

CHS continued building service line depth in targeted markets. The system acquired a vascular surgery practice and relocated a large OB practice onto its Birmingham campus, launched a urology program in Las Cruces, established a new neurosurgery and spine line in Laredo, and added robotic surgery programs in two New Mexico markets. The company reported 160 more employed physicians and APPs.

Management expects a more typical Q4 seasonal recovery supported by improved payer mix and patient sentiment. Exchange-plan volumes remain below 5% of total revenue, but CHS sees potential for a small elective uptick as exchange members pull forward procedures before possible policy changes. |

Key management quote: So as we called out in the second quarter and as I believe we still saw in the third quarter, some of the economic headwinds more the macroeconomic climate and consumer confidence seem to be the big headwind. And I think that continued on into the third quarter. Particularly some of our markets are experiencing some heavier or more softness economically than other markets. And so we still believe that that has been the primary driver of some of the softness. Now as consumer confidence seems to be stabilizing, it's bounced off its lows in the second quarter a little bit and seems to be improving. We are seeing some recovery, and I think that we experienced that where we saw some improvement in payer mix into the third quarter, and we're certainly experiencing that in some of our markets. So that gives us a little more confidence as that payer mix improves and people are feeling better, they're starting to come back in for more procedures. Although we were still down on an outpatient elective surgery volume year over year, it was improved over second quarter. So we did see some improvement there. I'd also point out maybe that the immigration climate probably is affecting some of our markets still. If you think about markets in Arizona, across Texas primarily, there's still probably a little bit of an overhang there where patient behavior, people are staying away from hospitals, at least on an elective basis more than we've seen in the past. Now we're also experiencing or noticing that in our ER visits and many of those are uncompensated. So where you're seeing some lower volume and maybe why that hasn't completely been noticed in our EBITDA generation is because some of that volume that we're seeing or loss of volume, particularly in the ERs and uncompensated care. And so that has not had an EBITDA negative EBITDA impact on us. |

Revenue Growth, Payor Mix, Reimbursement |

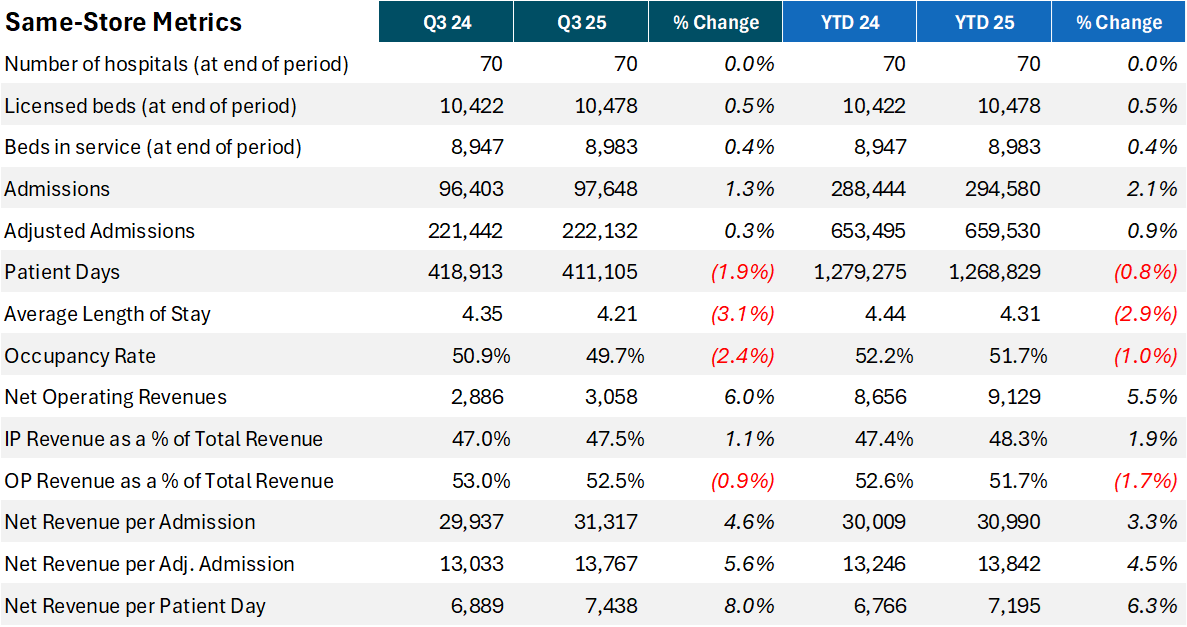

Revenue performance outpaced volume trends as rate and mix did the heavy lifting. Same-store net revenue grew 6%, with net revenue per adjusted admission up 5.6%. About one-third of the yield gain came from state-directed Medicaid payments in Tennessee and New Mexico approved earlier in the year. The balance came from commercial rate increases and favorable payer mix, offset partially by lower surgical acuity.

Payor mix improved through the quarter compared to prior quarters this year, driven primarily by commercial volumes with a modest lift from exchange membership. Still, CHS is seeing significant growth in Medicaid mix. Despite significant Medicaid redetermination activity in Indiana - one of CHS's largest states - execs said they haven't yet seen a measurable impact on Medicaid volume or revenue. |

CHS also reported progress stabilizing payor denials. After a notable spike in 2024, denials have leveled off as CHS invests in physician advisor coverage and applies AI-driven denial prevention and appeals tools within its internally managed revenue cycle. Finally, CHS noted a small positive impact from the Medicare final rules coming in. Key management quote: "About a third of that 5.6% improvement in same-store net revenue per adjusted admission is a result of the Tennessee and New Mexico state-directed payment programs approved in the second quarter. The rest of the improvement is payer mix related, even with some lower acuity." — Jason Johnson, Interim CFO |

CHS saw some margin expansion in Q3 |

Adjusted EBITDA margin expanded to 12.2%, or roughly 11.4% excluding a legal settlement, marking 20 basis points of year-over-year improvement despite the soft outpatient mix. Supplies dropped to 15% of net revenue, down 20 basis points, as the company continued optimizing its ERP platform for better workflow and cost control. Labor costs stayed in check. Contract labor declined slightly, and average hourly wage increases tracked within expectations. The company continues to hire directly, with employed physicians and advanced practice providers up 160 year over year, reducing reliance on contract staffing. Medical specialist fees rose 4% to $165 million, representing 5.4% of net revenue. Leadership expects some continued upward pressure, particularly in radiology, though AI and workflow efficiency may help offset future growth. Key management quote: "We expect continued upward pressure on medical specialist fees in the fourth quarter and into next year, especially in radiology, while increased use of emerging or developing technology, including AI tools, should eventually help on this front." |

Capital Allocation, M&A, Partnerships |

CHS continues to stabilize its capital structure while freeing up cash for strategic investments. The company refinanced $1.743 billion of 2027 notes through a $1.79 billion issuance of 9.75% senior secured notes due 2034, reducing leverage to 6.7x from 7.4x at year-end 2024. The next significant maturity is now pushed to 2029, giving CHS more balance sheet runway. Operating cash flow totaled $70 million in Q3 and $277 million year to date as reported, or $403 million when excluding $126 million of cash taxes tied to hospital sale gains. Management reaffirmed expectations for positive full-year 2025 free cash flow after adjusting for these taxes. CHS expects positive free cash flow in 2025, giving it flexibility to delever or pursue small-scale acquisitions and access point expansion. To that end, the hospital operator plans to open three ASCs in Q4 2025 and six to eight in 2026, alongside three to four freestanding emergency departments per year and selective urgent care projects. These lower-cost access points are faster-cycle growth levers than are large inpatient towers, especially in the year of our UnitedHealth Group overlords' 2026. CHS received $91 million in contingent cash from the Tenova Cleveland sale in October and expects to close the $195 million sale of its outreach lab assets (to Labcorp, recall) later this quarter. Earlier in the year, CHS also completed divestitures of Lake Norman, ShorePoint, and Cedar Park hospitals. CHS expects to continue its divestiture streak as well: "Yes, we're still pursuing some divestitures. We're in some early conversations that it's too early at this point. We don't know how far those will go. But certainly, we're continuing to get some inbound interest. We are in some more advanced discussions on a couple of deals, which we think could be announced even later this year. But no agreements have been signed at this point, so nothing to report today, but we are advancing some discussions on other deals." - During 2025, through the date of this press release, the Company has divested (i) its 50% ownership interest in two hospitals (one of which was completed on February 1, 2025, and the other of which was completed on May 1, 2025), (ii) its 80% ownership interest in one hospital (which was completed on June 30, 2025), and (iii) three other hospitals (two of which were completed on March 1, 2025, and one of which was completed on April 1, 2025).

- On July 22, 2025, the Company entered into a definitive agreement with Laboratory Corporation of America Holdings ("Labcorp"), pursuant to which Labcorp has agreed to acquire select assets and assume certain leases of the ambulatory outreach business of the Company's subsidiaries in 13 states, including certain patient service centers and in-office phlebotomy locations. The total purchase price payable to the Company at the closing of this transaction is $195 million, less certain purchase price adjustments. For additional information regarding this definitive agreement, see the Current Report on Form 8-K filed by the Company on July 22, 2025.

- In October 2025, in connection with the Company's divestiture of Tennova Healthcare – Cleveland, which was completed effective August 1, 2024, the Company received additional cash consideration of approximately $91 million as a result of modifications to applicable supplemental reimbursement programs. Such amount did not qualify for recognition during the three months ended September 30, 2025 and is expected to be recognized as an impairment (gain) loss on sale of businesses in the Company's consolidated statements of income (loss) during the three months ending December 31, 2025.

|

Innovation and Technology |

CHS's technology strategy is beginning to deliver operational returns. The company's ERP implementation is complete and now in optimization mode, helping standardize supplies management and improve process stability across hospitals. In revenue cycle operations, CHS has deployed AI tools to detect and prevent payer denials earlier in the process, paired with expanded physician advisor coverage to ensure clinical documentation supports patient status determinations. These changes have stabilized net revenue yields after a challenging payer environment in 2024. On the clinical side, CHS continues to invest in robotics, spine, and surgical technology as part of its broader focus on higher-acuity service line growth. Key management quote (the bots are coming): "So we called out really third quarter of last year in 2024 a big spike in denials. Since that time, it's stabilized. It has not really gotten any worse. But we continue to invest in our physician advisor program. We're investing in some AI tools in terms of how we do denials with our internal revenue cycle team. We are using a combination of third party vendors as well as internally developed products on that for purposes of our revenue cycle team. Our revenue cycle is managed internally with our own team, they do use a combination of products. So as we get better at it, I would say we've been able to kind of hold things stable, which would indicate that the payers are probably also denying more claims, but we've been more efficient or better at overturning some of those denials in order to kind of keep things status quo." |

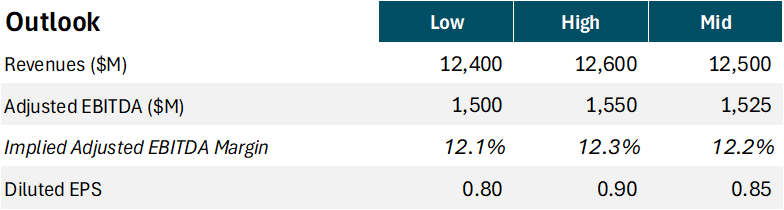

Management tightened 2025 adjusted EBITDA guidance to $1.50 to $1.55 billion, excluding contributions from unannounced divestitures or new supplemental payment programs. Positive free cash flow is expected for the full year after adjusting for divestiture cash taxes. Looking to 2026, CHS expects a modestly favorable policy environment. The finalized Medicare inpatient rate updates should be a tailwind, while even if the outpatient rule is finalized as proposed, the combined impact should be slightly positive year over year. Additional upside could come from new state-directed Medicaid payment programs in Georgia, Florida, and Indiana, as well as participation in a developing Rural Health Fund. For modeling, CHS recommended analysts exclude the $28 million legal settlement from 2025's base. Key management quote: "…there's a couple other SDP programs out there in Georgia, Florida, Indiana, the Rural Health Fund, which we don't know, can't quantify at this point, but that should be incrementally positive for us. And then we're making continue to make some growth investments. And as you just mentioned, with positive free cash flow this year continuing on into next year may allow us to further invest in some incremental growth capital." …As I mentioned in my prepared remarks, we have taken the time to visit several local health systems. We've met with health system leaders in, I think, substantially all of our major markets already. They're very enthusiastic about the progress we're making. And I just am becoming increasingly confident that our investments, strategic priorities and the resources that we're appropriately laser focused on those most important aspects of our business. I think we'll see some of that come to fruition here in the near term with a few areas. I'm highly focused on quality of care. So our quality ratings, our patient and physician experience, employee satisfaction and I won't take my CFO hat on and I'll continue to be laser focused on free cash flow and making sure we've made such great progress over the last probably nine quarters in a row on free cash flow trending positively now that we're getting to kind of crossover from being negative to positive free cash flow, I think that's going give us a lot more opportunity. So as I think though about those kind of five priority areas for myself and the progress that we're already making on quality and getting focused on the others, I think that will help really accelerate what we can do in the future. |

|

|

SPONSORED BY PERFECTSERVE PerfectServe knows every disconnected tool and clunky workflow is a silent margin killer. So they built their platform for true integration. It not only unites your scheduling and communication workflows; it cuts the noise and eliminates the friction that's quietly draining time, dollars, and staff morale. Plus, it plays nice with your existing tech stack (even solutions from competitors). Ditch costly fragmentation in favor of fewer misrouted calls, smarter handoffs, and less frustration.

|

|

|

My favorite reads & resources from the week |

*This read is brought to you by one of my brand partners who help make this newsletter possible! |

|

|

Random personal anecdotes and musings from me |

I hope everyone had a great Halloween! My 2 year old dressed as a construction worker (we were his associates, of course) but I can't tell you how many people came up to us and raved about our 'Louvre Robber' costumes. So we totally just went with it, since we're so trendy and in the know on these kinds of things. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 49,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments