PARTNERED WITH  |

|

|

Happy Thursday, Hospitalogists. I'm prepping my 2026 travel schedule and want to know… are you going to any industry events next year? Can you do me a huge favor and fill out this super short survey to help my team figure out where (and when) we should do some Hospitalogy meetups in 2026? By the way, we're trying something new for next Tuesday's send, featuring contributions from YOU. Excited to see what you all think. Stay tuned! |

Was this email forwarded to you? |

|

|

SPONSORED BY TALKWALKER BY HOOTSUITE HLTH 2025 was full of big moments - from CareIntellect's expansion to AI breakthroughs - that sparked media coverage and social conversations. Talkwalker analyzed public signals to capture all of it live, breaking down macro trends and micro-level conversations into data-driven, actionable insights. See what you missed in Talkwalker's HLTH 2025 Dashboard. This is just one example of the real-time intel healthcare organizations can get to stay on top of industry trends and brand-specific signals. Talkwalker is a healthcare marketer's edge, cutting through the noise to surface what's trending and what people are saying in real-time about an organization, its competitors, and more. This AI-driven platform is also an essential tool for operations leaders, synthesizing business-critical news that helps them identify risk sooner and make faster, more informed decisions.

|

|

|

Going deeper on an interesting topic, theme, or trend |

Tenet Healthcare Q3 Earnings Breakdown: Solid Ops, Uncertain Policy, Acuity Drives Results |

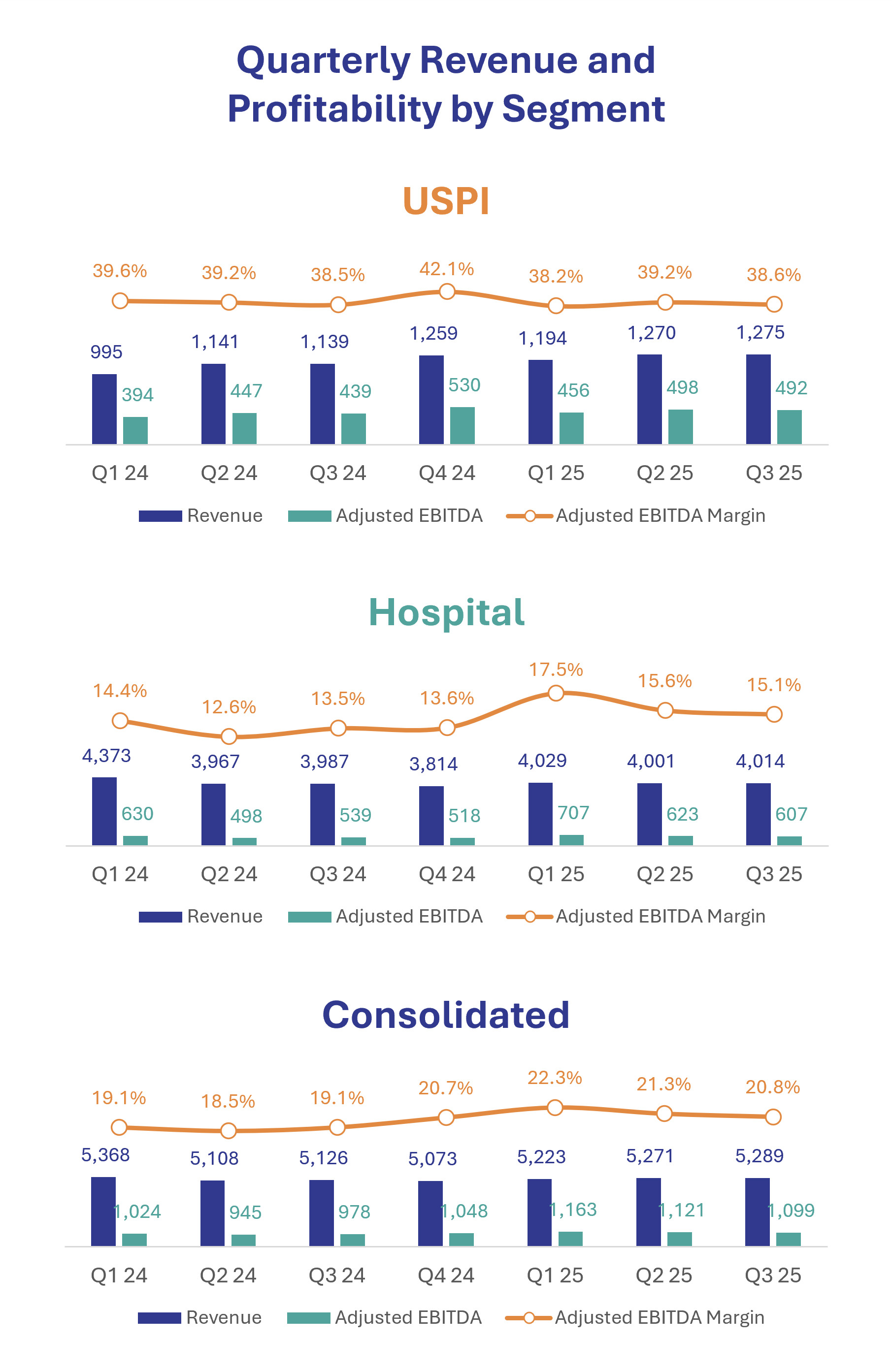

Boiling years of execution and work down to one singularity, acuity is the core strategy and term for Tenet in Q3. Tenet has a perfect blend of optimizing both its hospitals and ASCs for max rate and acuity. If you learn nothing else from this quarter, it's exactly this: Tenet is investing in highly complex inpatient work (neurology) and higher complexity outpatient work (emerging cardiology, ortho). As a result, the hospital operator is firing on all cylinders and posted another solid beat and raise with margin expansion on both sides of the house, steady volumes, and a larger 2025 investment plan that doubles down on higher acuity growth while keeping leverage low and cash conversion high. |

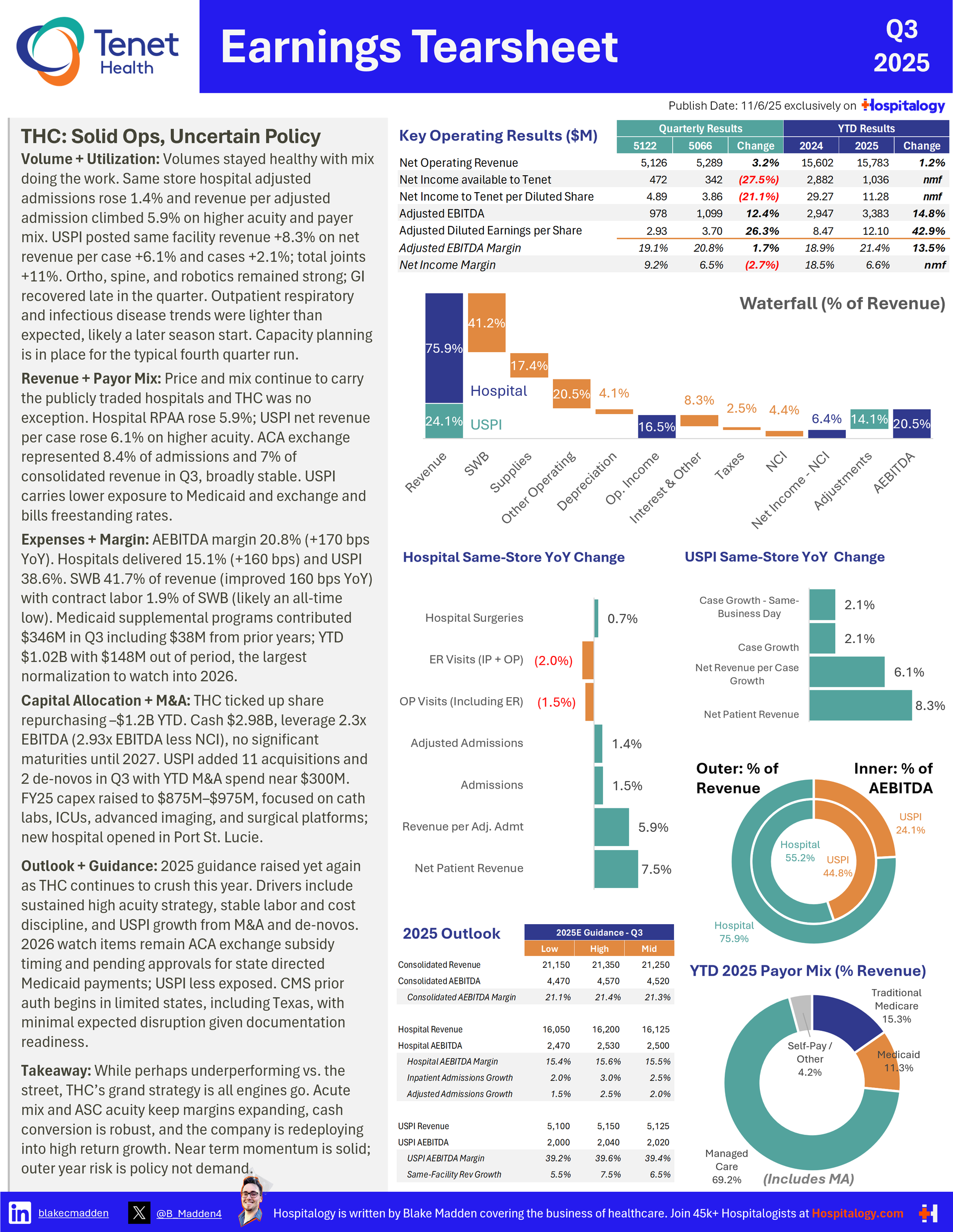

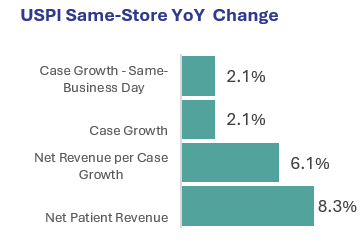

Volumes stayed healthy with mix and acuity (more on that in a sec) doing the work. Same store hospital adjusted admissions rose 1.4% and revenue per adjusted admission climbed 5.9% on higher acuity and payer mix. USPI posted same facility revenue +8.3% on net revenue per case +6.1% and cases +2.1%; total joints +11%. Ortho, spine, and robotics were callouts on the call and remained strong; GI recovered late in the quarter. Outpatient respiratory and infectious disease trends were lighter than expected, likely a later season start (flu season, sadly, drives up volumes). Capacity planning is in place for the typical fourth quarter run. |

Being a huge ASC operator, Tenet was of course asked about the inpatient only list removal, and THC management framed it as a positive tailwind for USPI without quantifying much, which makes sense considering the OPPS rule isn't even finalized yet (though it should be out any day now). The more telling comment was Tenet already trying to insulate itself from the IPO removal, saying they're already working on moving only the most complex, higher acuity work within the 4 walls of the hospitals. If I'm a hospital operator, this is the framework I'm working with - as long as you have the capacity, equipment, subspecialists, infrastructure, etc. to support this shift. Tenet has done this, increasing its CAPEX plans per bed on the inpatient side. |

Revenue + Reimbursement + Payor Mix |

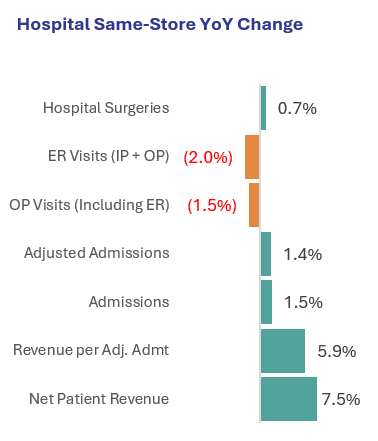

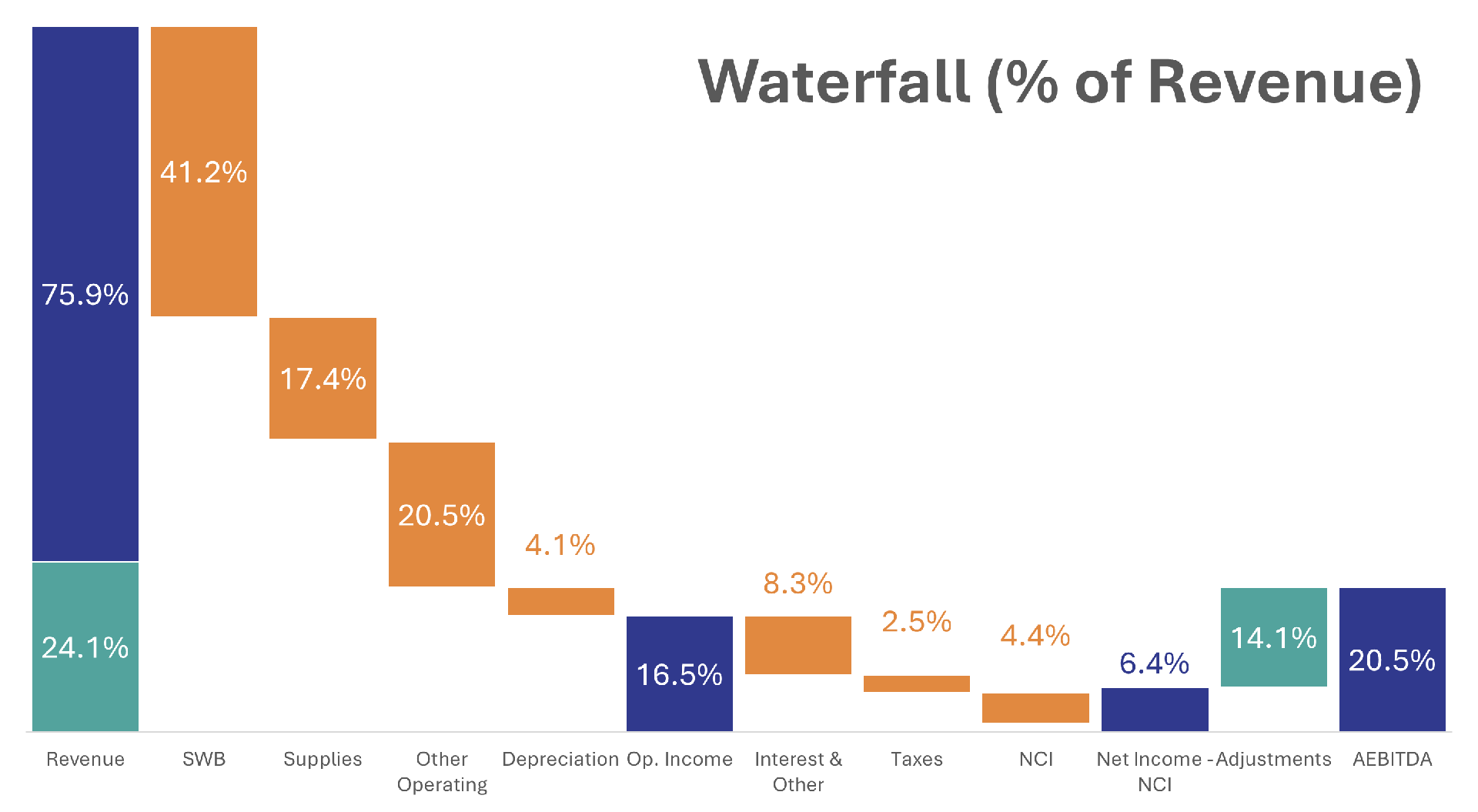

As mentioned, acuity and mix are the name of the game for Tenet. Price and mix continue to carry the publicly traded hospitals. ACA exchange represented 8.4% of admissions and 7% of consolidated revenue in Q3, broadly stable. USPI carries lower exposure to Medicaid and exchange along with site neutral as it bills freestanding rates. Interestingly, denials were not a big focal point this quarter. The amount of rate lift we're seeing leads me to question whether this trend is sustainable. It probably is on the outpatient side, but the inpatient side revenue per adjusted admit of 5.9% is massive (same with HCA, CHS - all were well above 5% growth for Q3 given ACA, supplemental payments, and acuity). BONUS! Segment Analysis: |

AEBITDA margin 20.8% (+170 bps YoY). Hospitals delivered 15.1% (+160 bps; driven by acuity and payor mix) and USPI 38.6% (flat). SWB 41.7% of revenue (improved 160 bps YoY) with contract labor 1.9% of SWB (consistent with last quarter and an all-time low). Medicaid supplemental programs contributed $346M in Q3 including $38M from prior years; YTD $1.02B with $148M out of period, the largest normalization to watch into 2026. |

Capital Allocation + Partnerships + M&A |

Repurchases up, debt leverage at an all-time low - THC ticked up share repurchasing –$1.2B YTD. Cash $2.98B, leverage 2.3x EBITDA (2.93x EBITDA less NCI), no significant maturities until 2027. USPI added 11 acquisitions and 2 de-novos in Q3 with YTD M&A spend near $300M. FY25 capex raised to $875M–$975M, and as discussed above, Tenet is focused on higher capex spend for higher complexity procedure capabilities in the likes of cath labs, ICUs, advanced imaging, and surgical platforms; Tenet also new opened a new hospital in Port St. Lucie focused on - you named it - higher complexity including 'robotics and advanced cardiac cath techniques.' |

Nothing really specifically called out on the innovation side other than Tenet mentioning centralization of administrative and business functions - finance, HR, advanced analytics, etc. Everything you would expect them to say publicly. Over time, Tenet is identifying opportunities for efficiencies. How vague and business-ey. And this is coming from a consultant! Keep in mind that Conifer, Tenet's owned RCM segment that rolls up into hospital operations, holds a ton of opportunity in RCM to improve its workflows and automated processes through leveraging AI for things like better patient communication, medical coding and documentation, prior auth, eligibility, and more. In this regard, given the opportunity and expanding multiples in the RCM space, Tenet's decision (or inability) to spin off or sell Conifer may lead to more significant opportunities over time and a new growth vertical. |

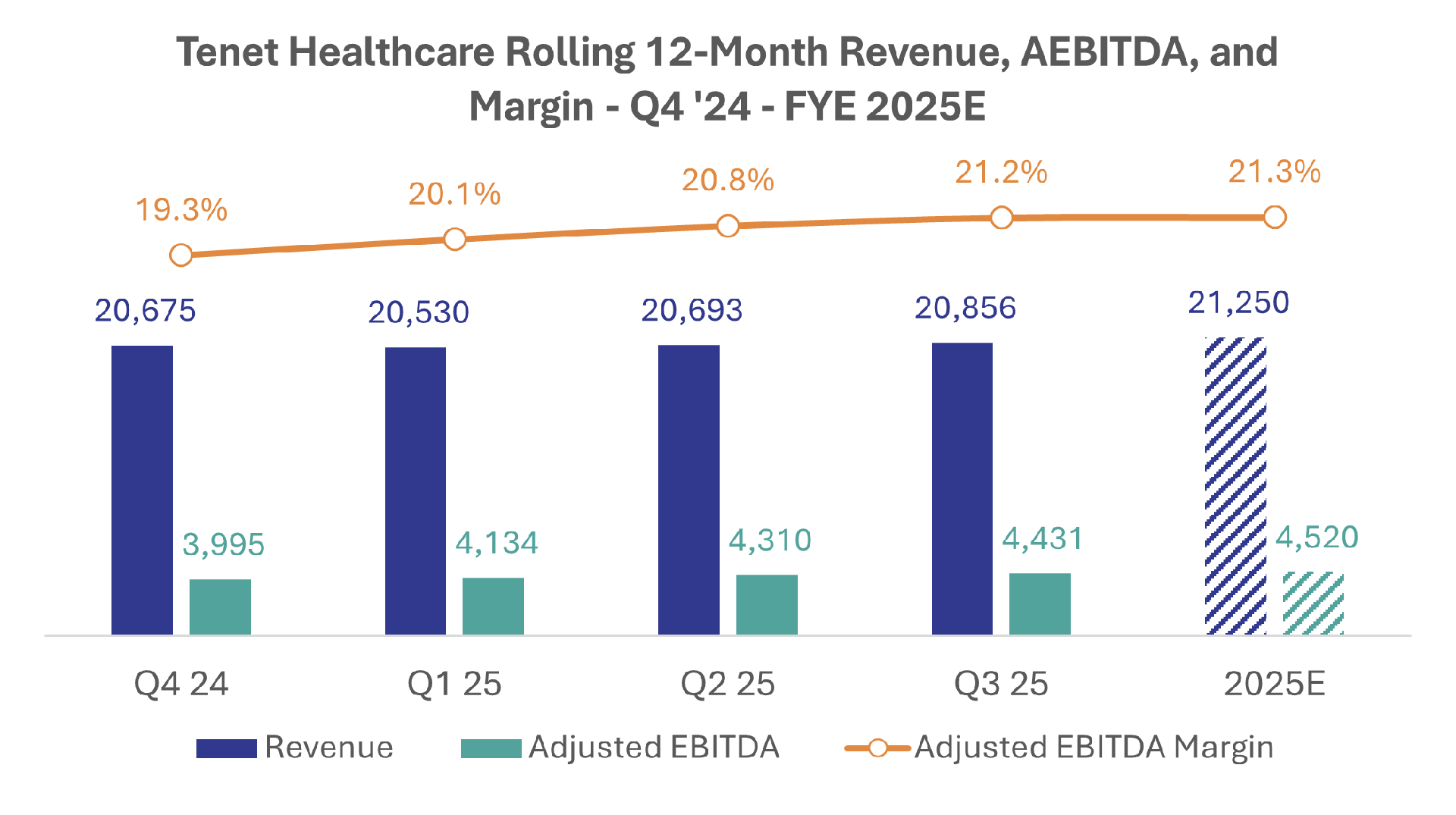

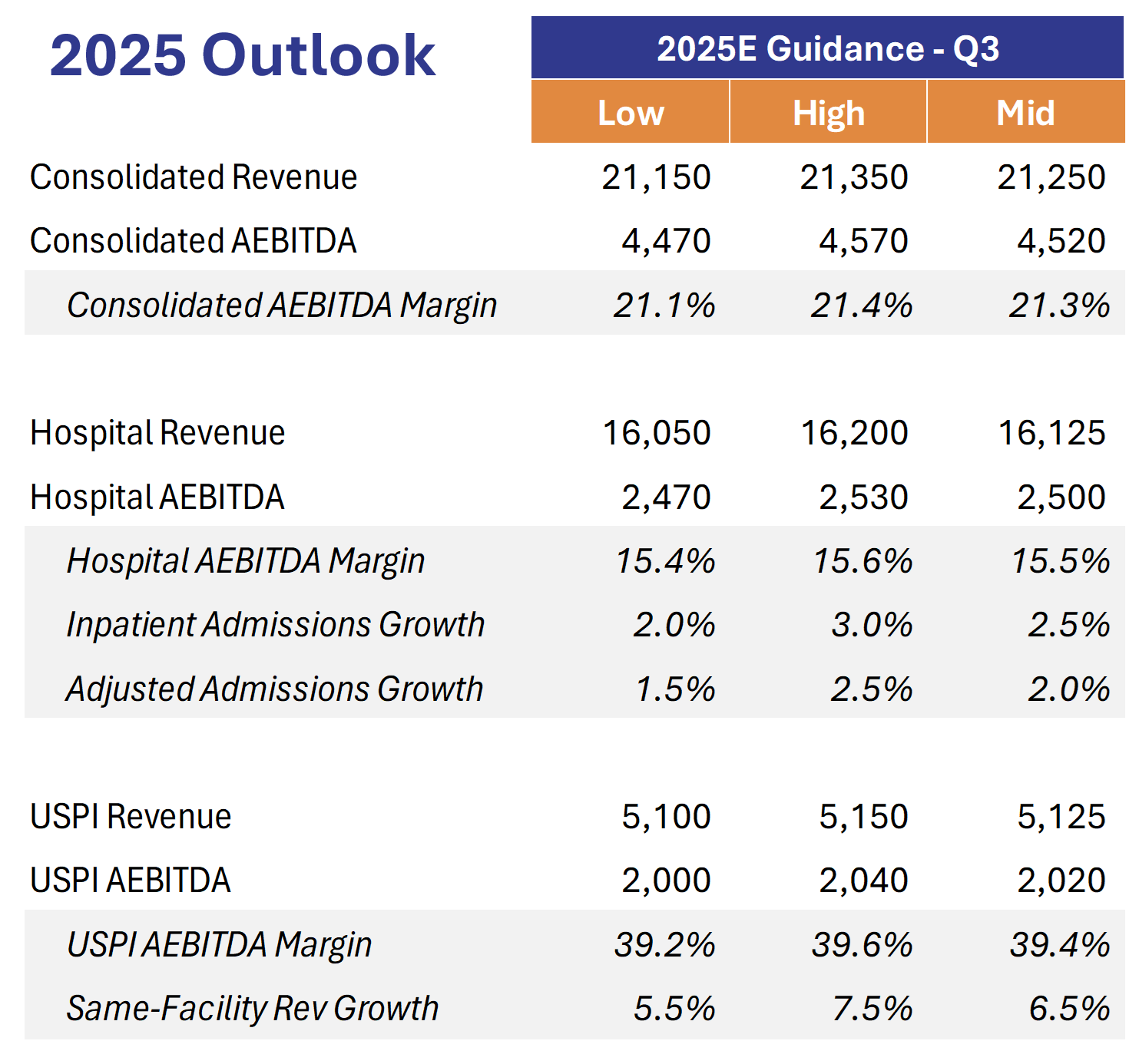

2025 guidance raised yet again as THC continues to crush this year. Drivers include sustained high acuity strategy, stable labor and cost discipline, and USPI growth from M&A and de-novos. 2026 watch items remain ACA exchange subsidy timing and pending approvals for state directed Medicaid payments; while USPI is less exposed to these dynamics. CMS prior auth begins in limited states, including Texas, with minimal expected disruption given documentation readiness. |

While perhaps underperforming vs. the street, THC's grand strategy is all engines go. Acute mix and ASC acuity keep margins expanding, cash conversion is robust, and the company is redeploying into high return growth. Another solid quarter for the health system giant as it trades up 60%+ on the year in the public markets. |

|

|

SPONSORED BY WELLSKY Managing the total cost of care isn't about slashing budgets. It's about closing the gaps between handoffs.

That's what WellSky's latest tip sheet breaks down in three plays, from using real-time data and predictive insights in the hospital, to executing smarter discharge coordination across SNFs, home health, and more.

One large provider group used this model to shorten SNF length of stay and reduce readmissions by 8%. Download the tip sheet to see how they did it.

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 49,844+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments