PARTNERED WITH  |

|

|

Happy Thursday Hospitalogists! We're continuing our series on hospital Q3 earnings analysis. This time is UHS, then Ardent, then I'll post a comparative analysis of major themes that publicly traded hospital operators are thinking about in the remaining months of Q4 as well as the outlook for 2026. Let's dive in, and let me know if there's anything I missed. |

Was this email forwarded to you? |

|

|

SPONSORED BY NEUROFLOW Your population health data has a blind spot - and it's costing you. Most population health strategies overlook behavioral health conditions, leaving leaders flying blind on some of their highest-risk, highest-cost patients. The result? Missed revenue opportunities, inefficient resource allocation, and referrals that go nowhere. NeuroFlow's latest one-pager shows how leading health systems are filling this gap with behavioral health analytics that help population health teams: Identify and prioritize high-risk patients in real time Match patients to the right behavioral health resources faster Close the loop on referrals so patients actually get care The impact goes straight to your bottom line: better outcomes, more efficient operations, and revenue you didn't even know you were leaving on the table. Download the fact sheet to see how behavioral health intelligence is changing the game for population health leaders.

|

|

|

Going deeper on an interesting topic, theme, or trend |

Universal Health Services Q3 Earnings Analysis |

Universal Health Services Q3 2025: The Behavioral Health Differentiator Faces Its Growing Pains |

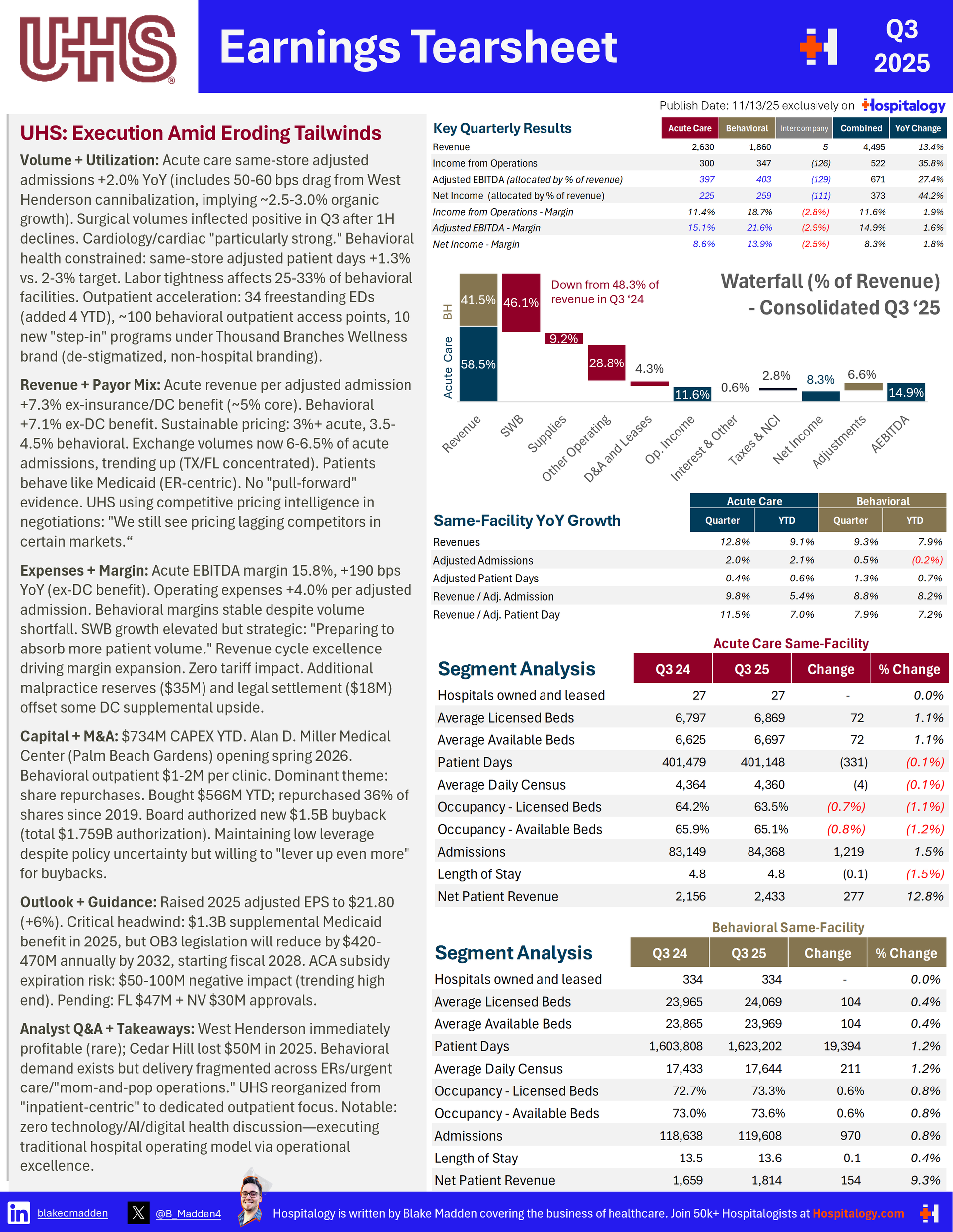

Universal Health Services' quarter laid bare both the structural strength and short-term strain of its behavioral health franchise. Despite being the only diversified operator with a majority of revenue from behavioral services, UHS is still struggling to translate secular demand into growth. Labor constraints are suppressing 25–33% of behavioral capacity despite demand being there. Behavioral utilization nationally is up, but payor utilization management and limited workforce availability have made "supply" the real bottleneck. |

At the same time, UHS sees opportunity in a competitive reset. As some peers slow expansion or shutter behavioral capacity, the company is leaning into step-down and outpatient programs where demand has surged over the past 5-7 years. The pivot toward hybrid behavioral models reflects a broader industry shift: moving care closer to the community while preserving clinical depth. For a company long defined by inpatient dominance, we're seeing UHS face health system transformation reality in real time. This evolution will determine whether UHS remains a behavioral leader or decays into a legacy operator in a fast-moving segment. |

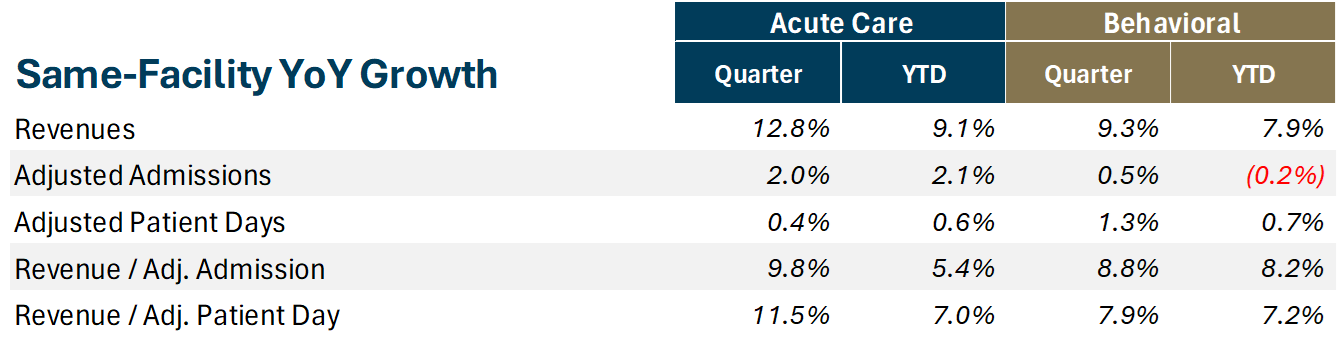

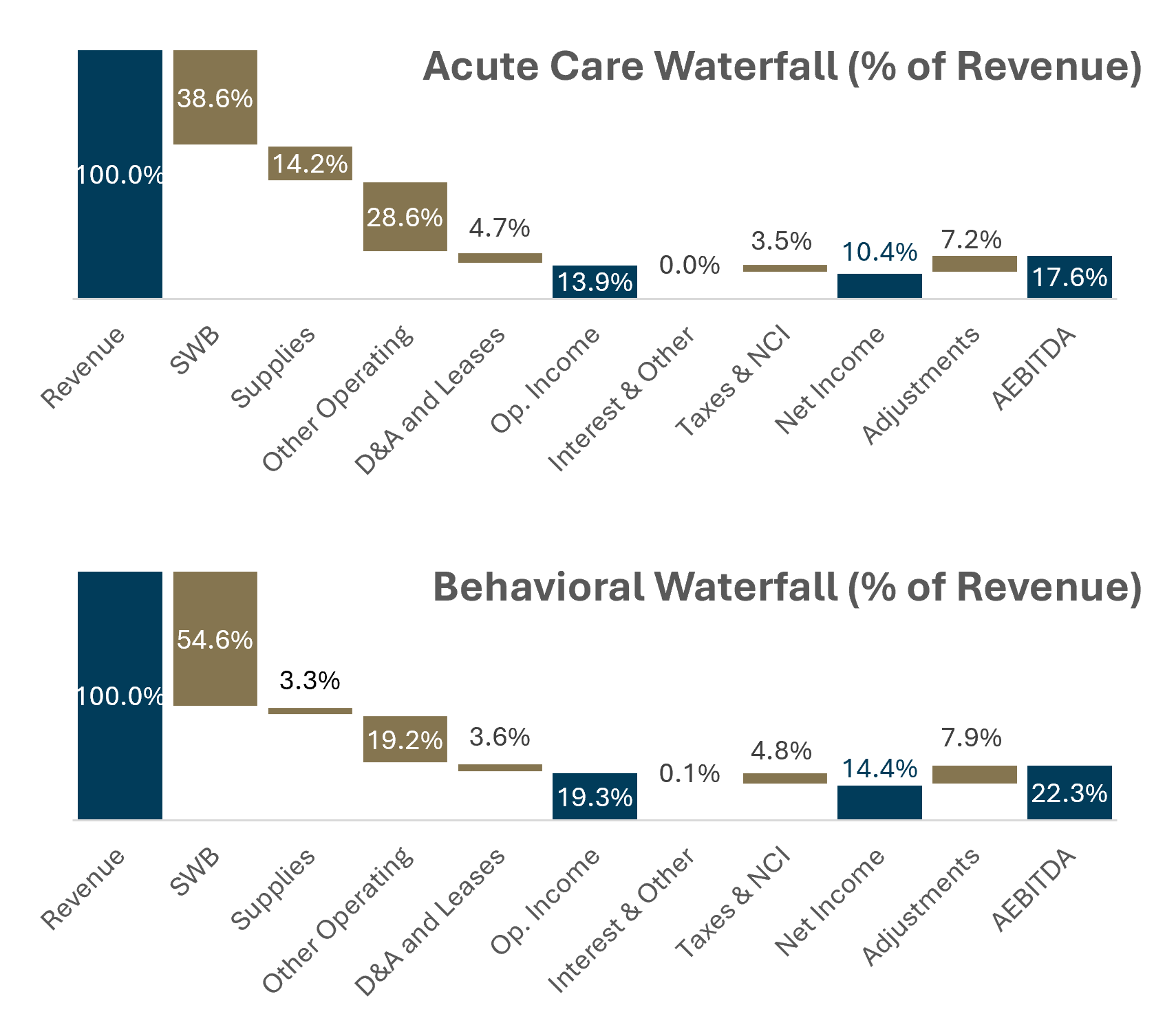

Mixed volume performance in Q3: Acute care trends were solid, with surgical growth described as "relatively across the board," and cardiac services singled out as particularly strong. Management avoided market-level disclosure but confirmed that major metros — including Las Vegas and Florida markets — performed above expectations. In behavioral health, adjusted patient days grew just 1.3%, well below the company's long-term 2–3% target. Filton attributed the shortfall to labor shortages at roughly a quarter of its facilities, limiting the ability to admit and treat despite clear underlying demand. Utilization remains high nationally, but UHS isn't fully capturing that demand given staffing and managed care constraints. Patient acuity in the acute segment appears stable to slightly higher, aligning with peer commentary across HCA and Tenet. Behavioral acuity levels are high as well, though length-of-stay compression from payer management continues to dampen volume growth even when demand rises. Taken together, UHS's utilization trends present an interesting paradox: the company has the right demand drivers but the wrong constraints and therefore is unable to fully monetize its volume potential until the workforce situation eases. |

Revenue Growth and Payor Mix |

Revenue growth for the quarter reflects stable pricing and disciplined payer management. While management didn't break out net revenue per admission, commentary implied steady mid-single-digit increases supported by commercial rate adjustments and mix benefits from higher-acuity cases in the acute business. The exchange population remains a small but monitored exposure at 6 - 6.5% of admissions. Filton downplayed concerns about coverage loss ahead of subsidy expirations, noting this group's utilization mirrors Medicaid rather than commercial — emergency room–centric and low elective volume. That dynamic should limit the near-term revenue hit from exchange churn, though it will reduce revenue per case and could increase uncompensated care exposure in 2026. Behavioral reimbursement remains a more complex picture. Managed care utilization management is the central friction point, constraining both length of stay and approved case volume. Still, outpatient expansion offers a pricing hedge: partial-day and step-down programs carry more predictable reimbursement and lower denial risk, balancing the inpatient volatility. |

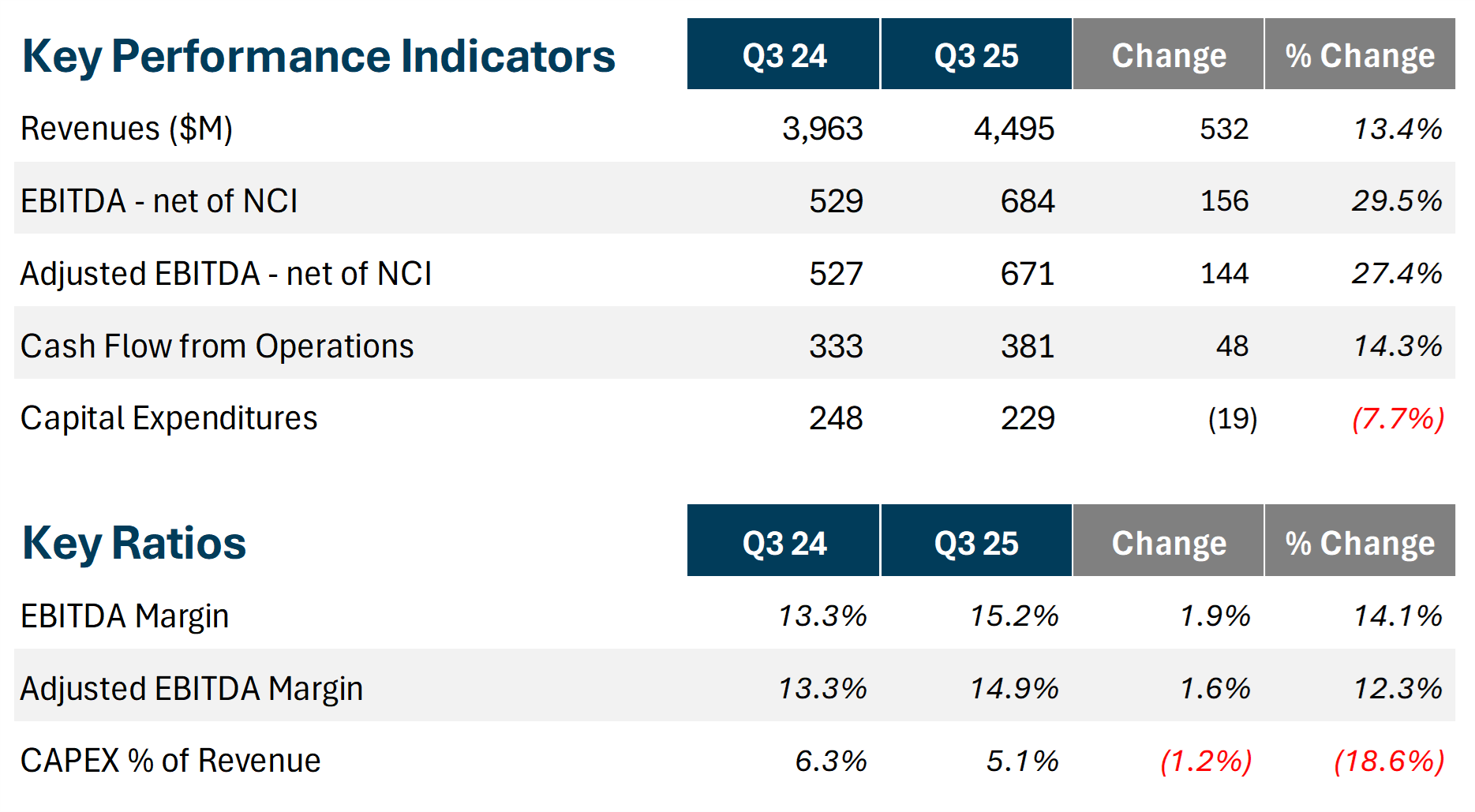

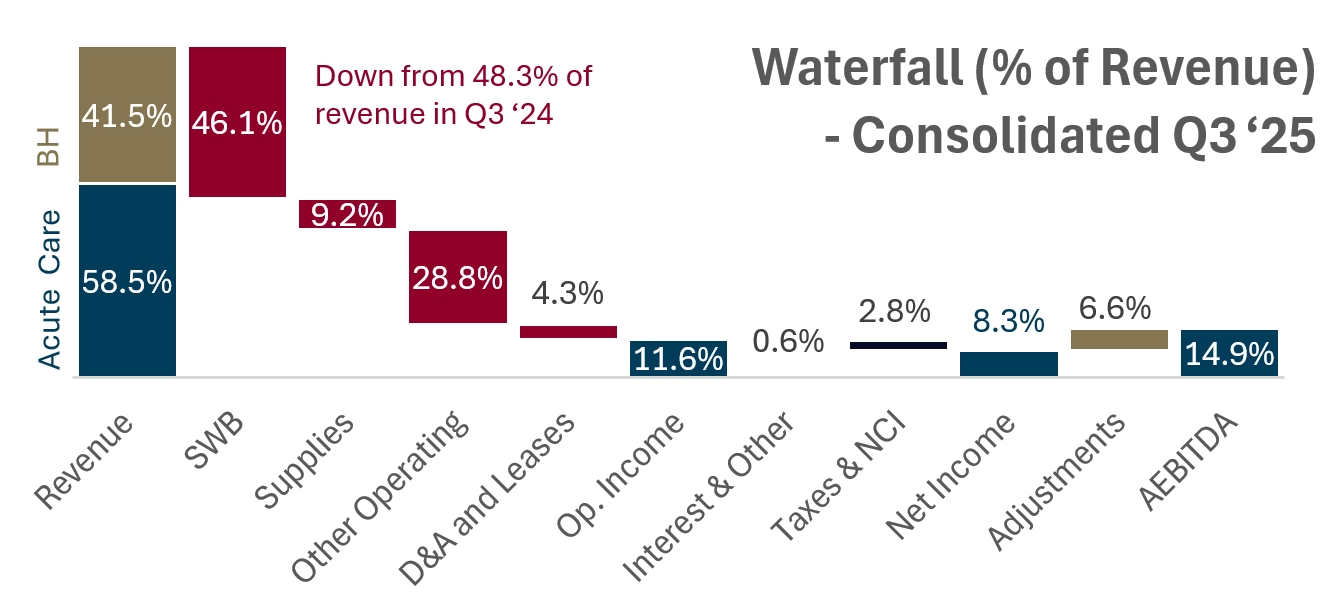

Margins improved materially in Q3. UHS posted a 15.8% same-facility acute care EBITDA margin, up 190 basis points year over year, putting it roughly on par with Tenet's hospital segment. The drivers were clear: higher acuity, disciplined expense control, and better labor productivity in acute operations. Behavioral margins were stable but constrained by wage inflation and underutilized capacity. Labor scarcity remains the single largest operating cost headwind. Professional fees — particularly in anesthesia and radiology — are inflating at double-digit rates, echoing concerns raised by HCA and others. |

The broader takeaway: UHS is expanding margin where it can (acute) and holding ground where it must (behavioral). Its low leverage and strong balance sheet allow it to absorb temporary inefficiencies without the existential stress smaller operators face. Management continues to flag Medicaid supplemental cuts as a 2026–2032 overhang, but offsetting programs in Florida and Nevada could add $75–80 million in relief next year. |

Capital Allocation, M&A, and Partnerships |

UHS is the disciplined defender among its peers. The company's capital strategy remains conservative with leverage at ~1.9x EBITDA, $4B in available liquidity, and a multi-year commitment to shareholder returns over expansion.

Since 2019, UHS has repurchased a whopping 36% of its shares, reflecting confidence in its cash flow durability and a dearth of attractive M&A targets. Capex continue to focus on de novo growth in high-growth states, including a new Florida hospital slated for 2026 and expansion of 34 freestanding EDs.

Management didn't announce any new deals but noted interest in distressed opportunities if valuations correct. Behavioral M&A remains tight, with few scaled assets trading. Expect UHS to stay opportunistic — selectively acquisitive, never aggressive — until policy clarity and labor capacity improve. |

Innovation and Technology |

Technology commentary was limited but directionally aligned with peers: automation and workforce optimization are now priority use cases. While UHS hasn't publicly detailed AI pilots, management has discussed investments in revenue cycle automation and clinical documentation areas with ability to create significant pricing lift across the sector.

Given UHS's heavy exposure to behavioral care, expect forthcoming initiatives to center on staff efficiency, remote monitoring, and AI-assisted patient triage - tools that can unlock constrained inpatient capacity. |

UHS execs reaffirmed the 5–6% acute and 6–7% behavioral revenue growth goals with cost growth around 4%, implying ongoing margin expansion. For 2026, key factors shaping the outlook include: - Supplemental Medicaid declines beginning, though mitigated by new programs in select states;

- Exchange subsidy expirations potentially trimming $50–100 million of revenue;

- Medicare IPPS increase of 2–3% supporting base rate growth; and

- Continued contract labor stabilization, providing modest expense relief

The underlying tone from management was steady, not exuberant. But one thing is clear: the 2025 playbook including volume recovery, labor normalization, and strong pricing won't repeat in 2026. Instead, expect mid-single-digit growth and incremental margin improvement, powered by outpatient expansion and disciplined capital allocation. UHS' acute business is quietly improving, de novo hospitals are ramping profitably, and the balance sheet is in great shape. Yet the same labor dynamics that fuel behavioral demand are capping its monetization. As 2026 approaches, UHS's measured posture - disciplined capital deployment, low leverage, outpatient expansion - may prove prescient. It's not a high-growth story, but it's a durable one. |

|

|

Texas vs. Georgia this weekend! I'm not expecting us to play great in Athens. We have a terrible track record this year on the road and can't seem to get out of our own way - multiple false starts, playing skittish, etc. - just look at our performance at Ohio State, in the Swamp, at Kentucky, at Mississippi State...I will say though, if we win any of the next 2 out of 3, depending on how everything else plays out, Texas may just shimmy their way into the playoff. That's a tall task with both Georgia and Texas A&M on the schedule. Though TAMU's SEC schedule has been a cakewalk. I will say - Texas' O line is finally healthy. The whole team is healthy. So there are no excuses this weekend. We will know exactly who this Texas team is after Saturday, win or lose! Hook 'em! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

| |

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 50,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments