PARTNERED WITH  |

|

|

Happy Thursday, Hospitalogists!

I'm rounding out my analysis of key for-profit hospital themes with one more lookback on the year.

This post is a smaller preview of a larger, incredibly robust report going out first thing next year. You could call it the Magnum opus of Hospitalogy.

It'll cover major nonprofit and for-profit dynamics and a deep dive into major strategic considerations and outlook facing hospitals and health systems entering the new year. So be on the lookout first week of January for it! Purpose built for health system strategy and C-suite teams to get ready for the year ahead.

Let's dive in. |

Was this email forwarded to you? |

|

|

Going deeper on an interesting topic, theme, or trend |

'Peak' Hospital Operations just happened, and uncertainty persists. Here's what happened in 2025 in a quick, analytical, scannable format. |

Key 2025 drivers & challenges |

- Volume and pricing outperformance (albeit with volume growth deceleration)

- Supplemental Medicaid uplift

- Contract labor normalization & labor market bottoming

- Revenue cycle improvements

- Favorable payor mix (commercial, exchange and MA)

- Distinct focus on acuity and mix

- Professional fees inflation

- ACA subsidy expiration

- OPPS and IPPS final rules (IPO list phase-in); 340B changes

- Lack of M&A beyond tuck-in's and bankruptcies - focus on ambulatory expansion and de-novo facility development

|

Executive summary: Hospital major themes and strategic analysis |

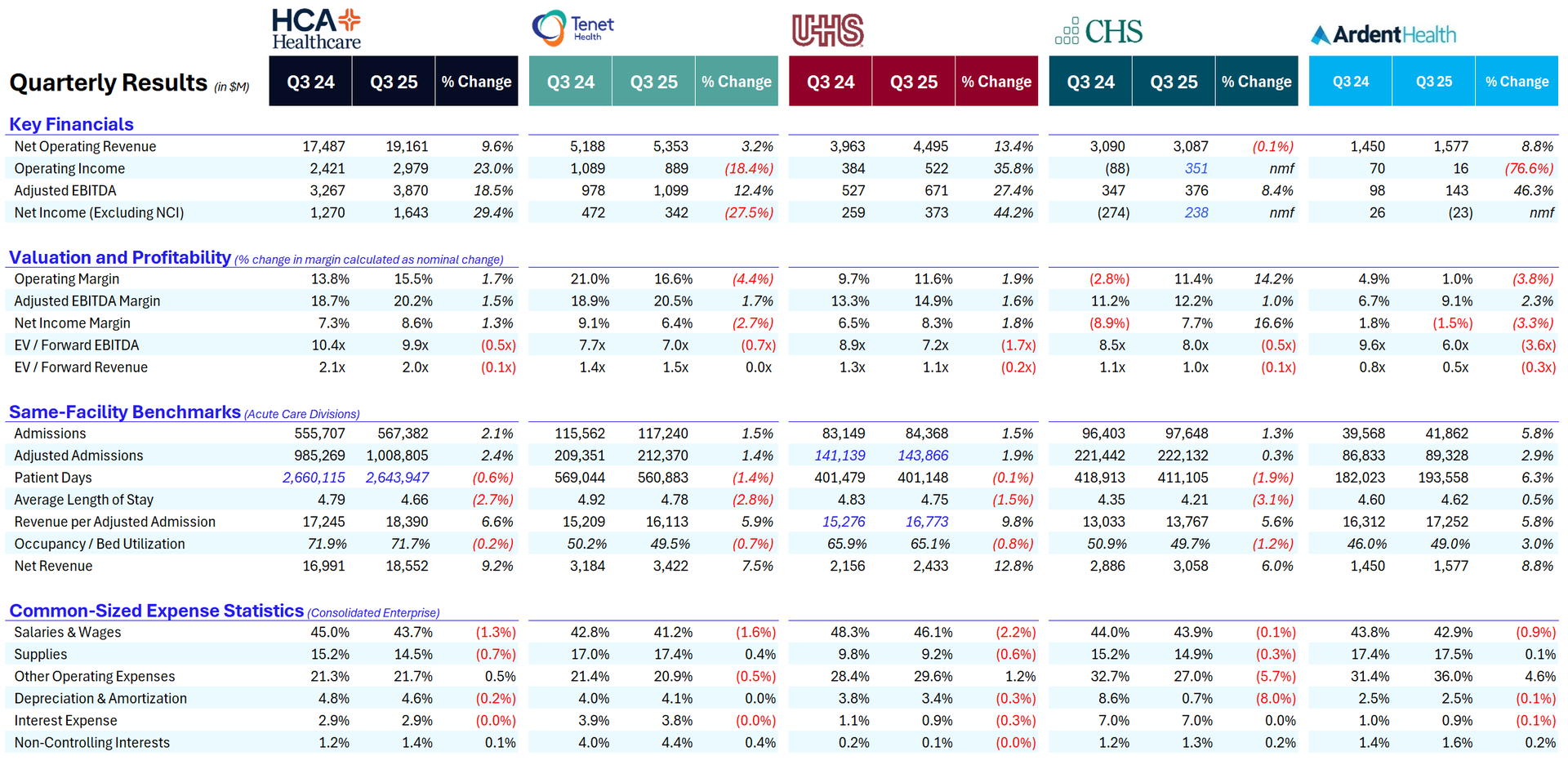

- Robust revenue cycle and pricing power: All five operators demonstrated exceptional revenue per admission/patient day growth ranging from 5.6% to 9.8%, significantly outpacing volume growth. This reflects successful commercial rate negotiations, favorable dispute resolution, a focus on high acuity services across sites of service, and effective revenue cycle management.

- The pricing environment is unusually strong: Revenue per unit growth of 5–10% is substantially above historical norms of 3–4%, driven by aggressive commercial rate negotiations, improved revenue cycle operations, and supplemental program benefits. This may not be sustainable as payers push back on utilization and coding intensity.

- Supplemental Medicaid windfall creating one-time uplift: Four of five operators (HCA, CHS, UHS, ARDT) benefited materially from state-directed payment programs, particularly Tennessee and District of Columbia programs, adding $240 million (HCA), $15–20 million (CHS), and $90 million (UHS) to Q3 results. Tenet received $38 million in prior-year supplemental revenues.

- Modest volume recovery but surgical softness persists: Same-facility adjusted admissions grew modestly across all operators (0.3% to 2.4%), with continued pressure on elective outpatient surgical volumes. All operators noted the elective surgery environment remains challenging, particularly orthopedics and cardiac procedures, suggesting persistent consumer caution.

- Elective surgery remains the canary in the coal mine: Surgical volumes remain soft across all operators, suggesting deep consumer uncertainty extends beyond immigration concerns to broader economic anxiety and high deductible burden.

- Outpatient access is the growth battleground: All operators are aggressively investing in freestanding EDs, ASCs, and ambulatory platforms, with Tenet's USPI segment demonstrating the power of this model with 38.6% EBITDA margins and 12% growth.

- Labor normalization driving margin expansion: Contract labor has stabilized at 1.9% to 4.2% of total labor costs across operators, down significantly from pandemic peaks. Wage growth remains elevated at 3–4% but manageable, with operators demonstrating improved operating leverage.

- Professional fees are the new labor pressure point: Multiple operators flagged professional fees (particularly anesthesia and radiology) growing 4–11% year over year, substantially above inflation, as physician groups exercise pricing power in a consolidating market.

- Capital deployment focused on organic growth and shareholder returns: In an environment of policy uncertainty and limited M&A opportunities, all operators prioritized share repurchases, organic growth investments, and balance sheet management. HCA repurchased $2.5 billion in Q3 alone, while Tenet repurchased $93 million, and UHS received a new $1.5 billion authorization.

- 2026 uncertainty dominated by policy concerns: All operators expressed caution about 2026 given uncertainty around exchange subsidy expiration (potentially impacting 100,000+ covered lives), Medicaid cuts from the One Big Beautiful Bill Act (OBBBA), and potential Medicare reimbursement reductions of up to 4%.

- 2026 policy risk is asymmetric and material: Operators face potential revenue headwinds from Medicaid cuts ($420–470 million annually at UHS), exchange subsidy expiration ($50–100 million annually at UHS, larger at HCA/CHS), and Medicare rate pressures, with limited offsets beyond operational efficiency.

|

HCA Healthcare Q3 Earnings Breakdown: Business as Usual |

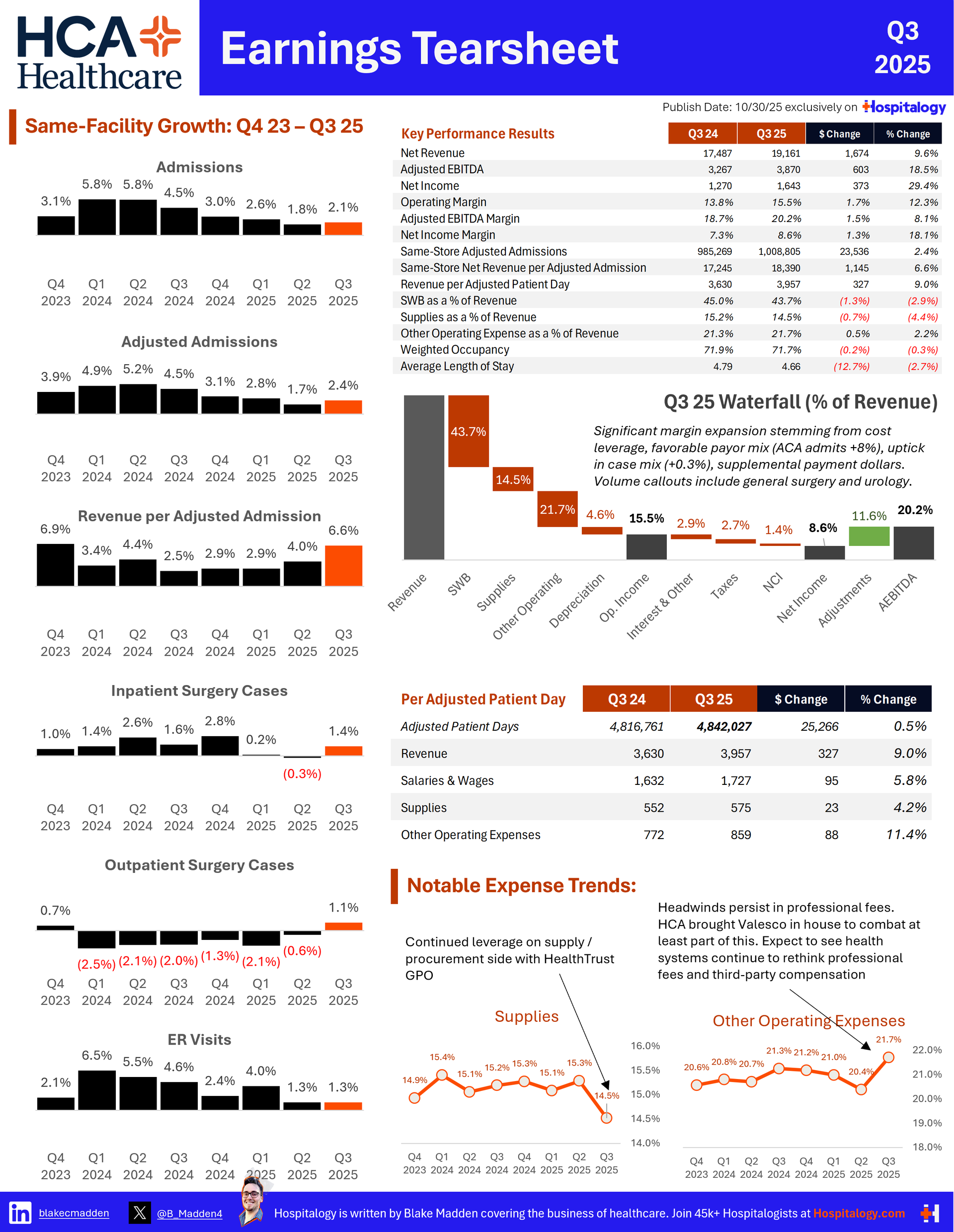

Volume + Utilization: Another quarter of broad-based growth. OP surgeries down (from Medicaid/Uninsured), but revenue increased 5% (acuity & payor mix grew 7% to counteract the decline). HCA specifically called out cardiac procedures, rehab, and obstetrics in prepared remarks on the earnings call itself. Medicare vs. MA: Same-facility Medicare admissions grew 5.3%. Traditional Medicare was flat. MA admissionsgrew11%inQ3; HCA attributed 2% of this growth to the 2-Midnight Rule. Same-facility adjusted admissions declined 8.5% in Medicaid, increased ~4% in commercial, and increased 43% in exchange. Uninsured adjusted admissions increased +7.2%. Revenue + Payor Mix: 7.1% = Same-facility revenue growth. 7.9% overall revenue growth. 'Modest' benefit from Medicaid supplemental payment programs. TOO MANY DENIALS: Point of emphasis for all hospitals in 2024. HCA has seen ramp-up in payor denial activity but didn't see a $$$ impact. Still, HCA observed a few large MA players driving the most denials. MA patients have higher LOS (around 10% higher) even adjusting for acuity. HCA blamed but is working with payors on this inefficient dynamic. Expenses + Margin: 0.9% increase in adj. EBITDA from improved labor (down 1.6% as a % of revenue) and contract labor (4.6% of total labor spend, down 18% over 2023). 2.5% - 3.5% wage increases for 2025. Supplies & other operating expenses squeezed revenues a bit. HCA sees opportunity with AI (immature today) and other investments to improve admin functions. It recently announced an expanded partnership with Commure to deploy ambient AI system-wide. Capital Allocation + CAPEX: ~$1.2B in CAPEX in the quarter. ~$1.8B in share repurchases and ~$170M in dividends distributed. HCA plans to have added 600 IP beds and 100 new OP facilities by the end of 2024. $6B in capital projects under development. 2,600 sites of care by the end of 2024. Outlook + Guidance: HCA thinks elevated volume growth will continue at 3% - 4% while reimbursement will increase 2% - 3%, resulting in growth 'near or slightly above' long-term HCA targets in 2025. $50M or $0.15/share lost estimate from hurricanes in Q3. Exchange growth will moderate in 2025 to 8% - 10% vs. 30% in 2024. My Take: While we may have reached peak 'hospital multiple' HCA continues to benefit from a strong & stable operating environment entering 2025 in its markets: broad-based growth with 'very few challenges.' Expect HCA to continue to win IP market share over less efficient competitors as it drives toward having 13 access points per hospitals in its markets. |

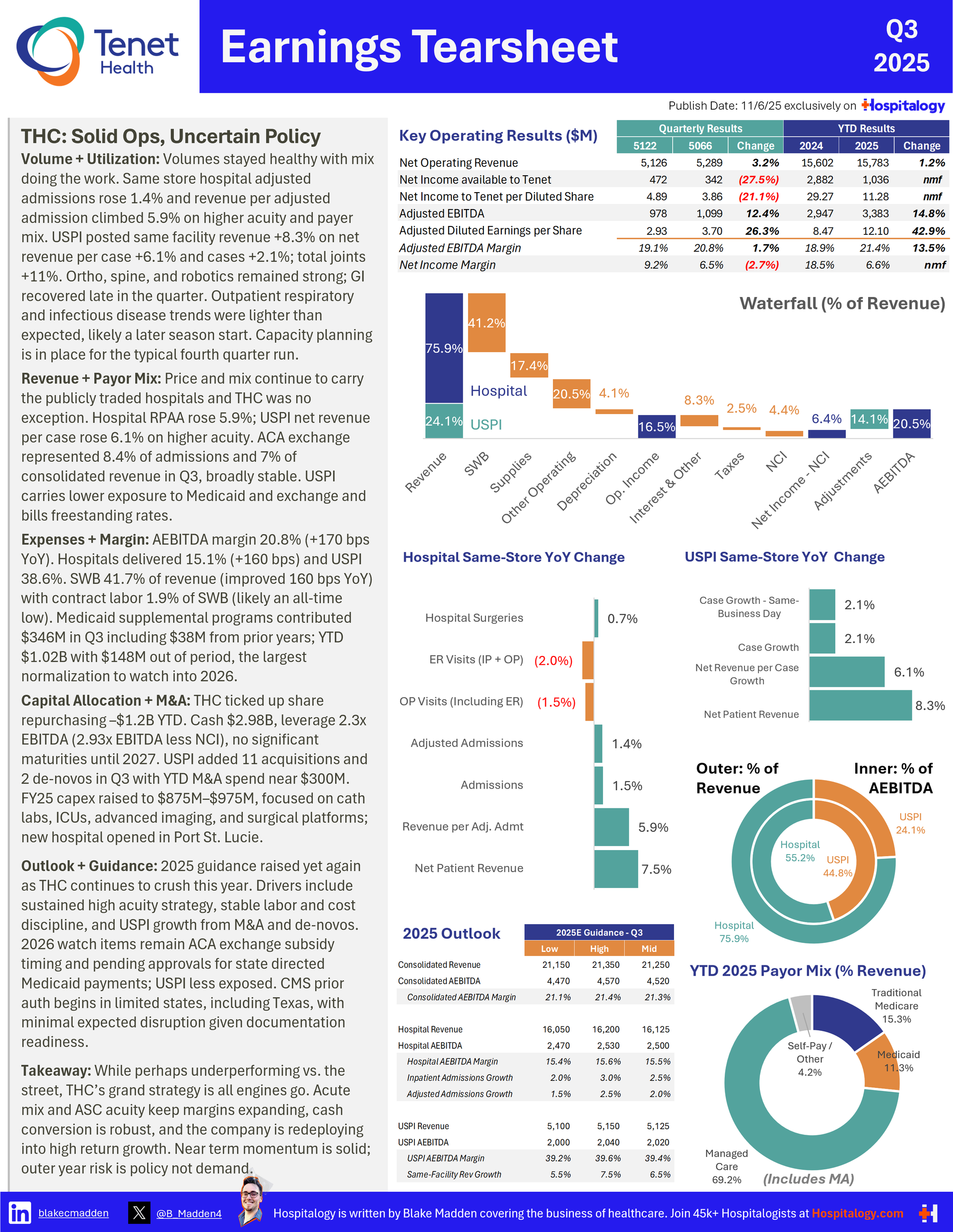

Tenet Healthcare Q3 Earnings Breakdown: Solid Ops, Uncertain Policy, Acuity Drives Results |

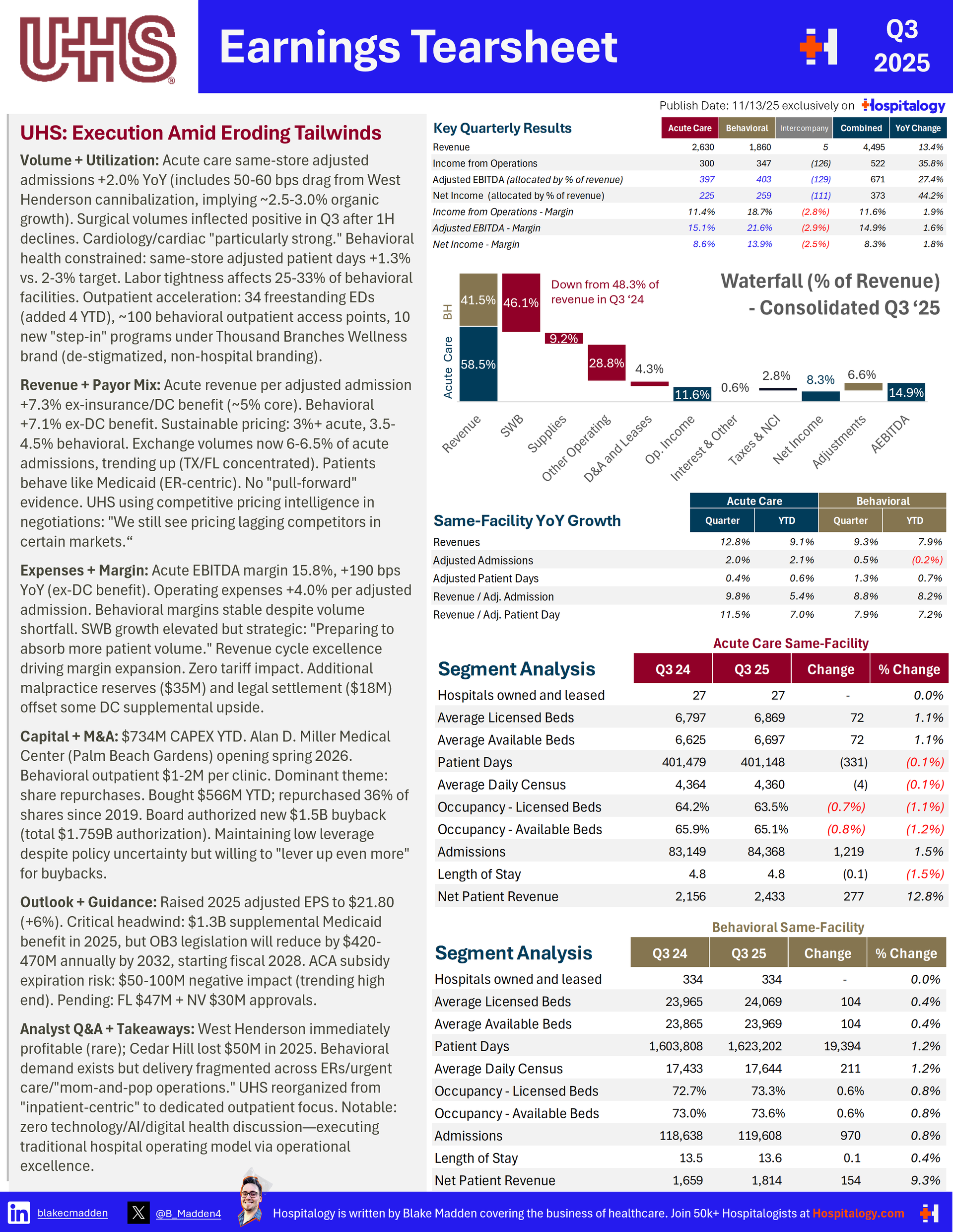

Universal Health Services Q3 2025: The Behavioral Health Differentiator Faces Its Growing Pains |

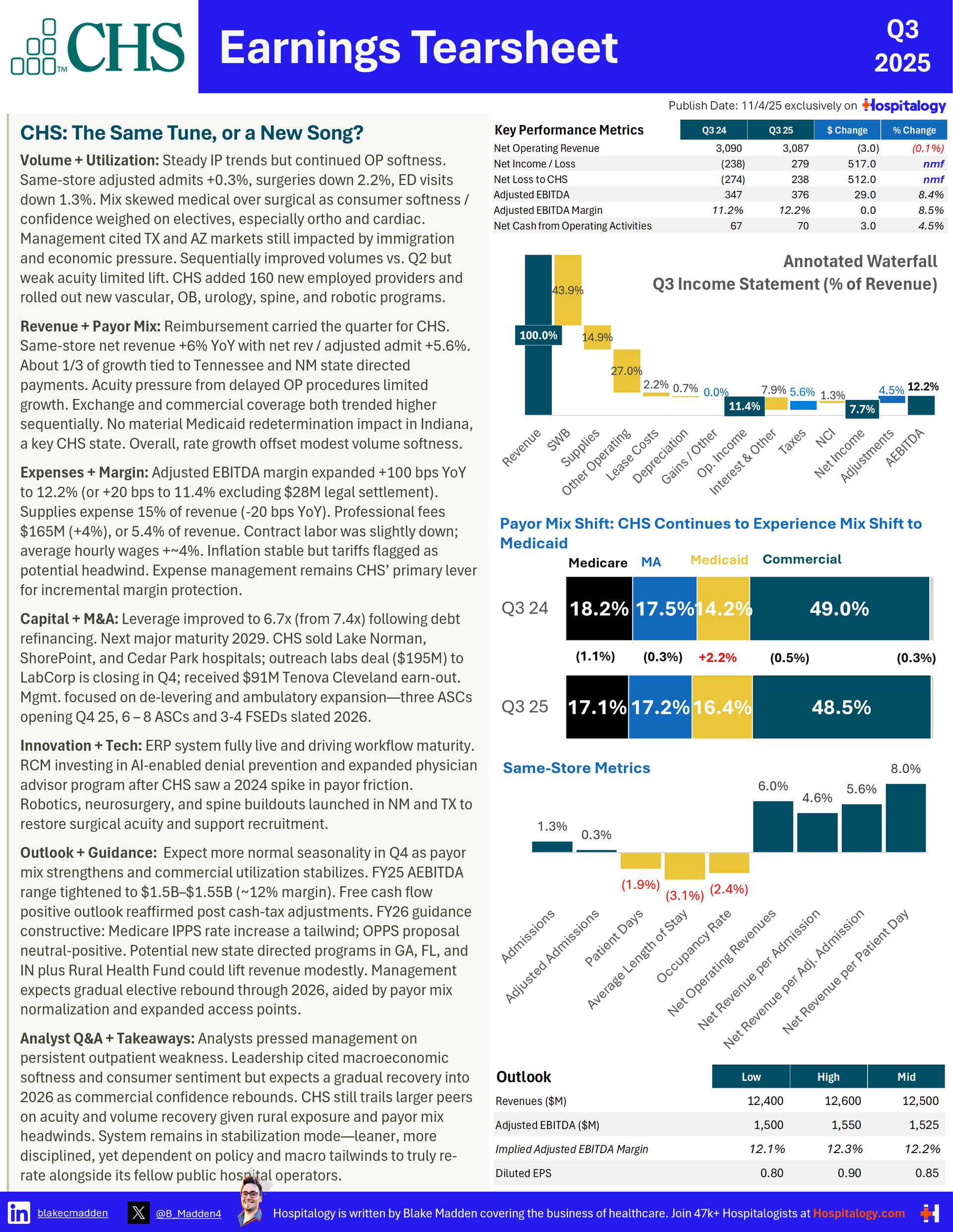

Community Health Systems (CHS) Q3 2025 Earnings Analysis: The Same Tune, or a New Song? |

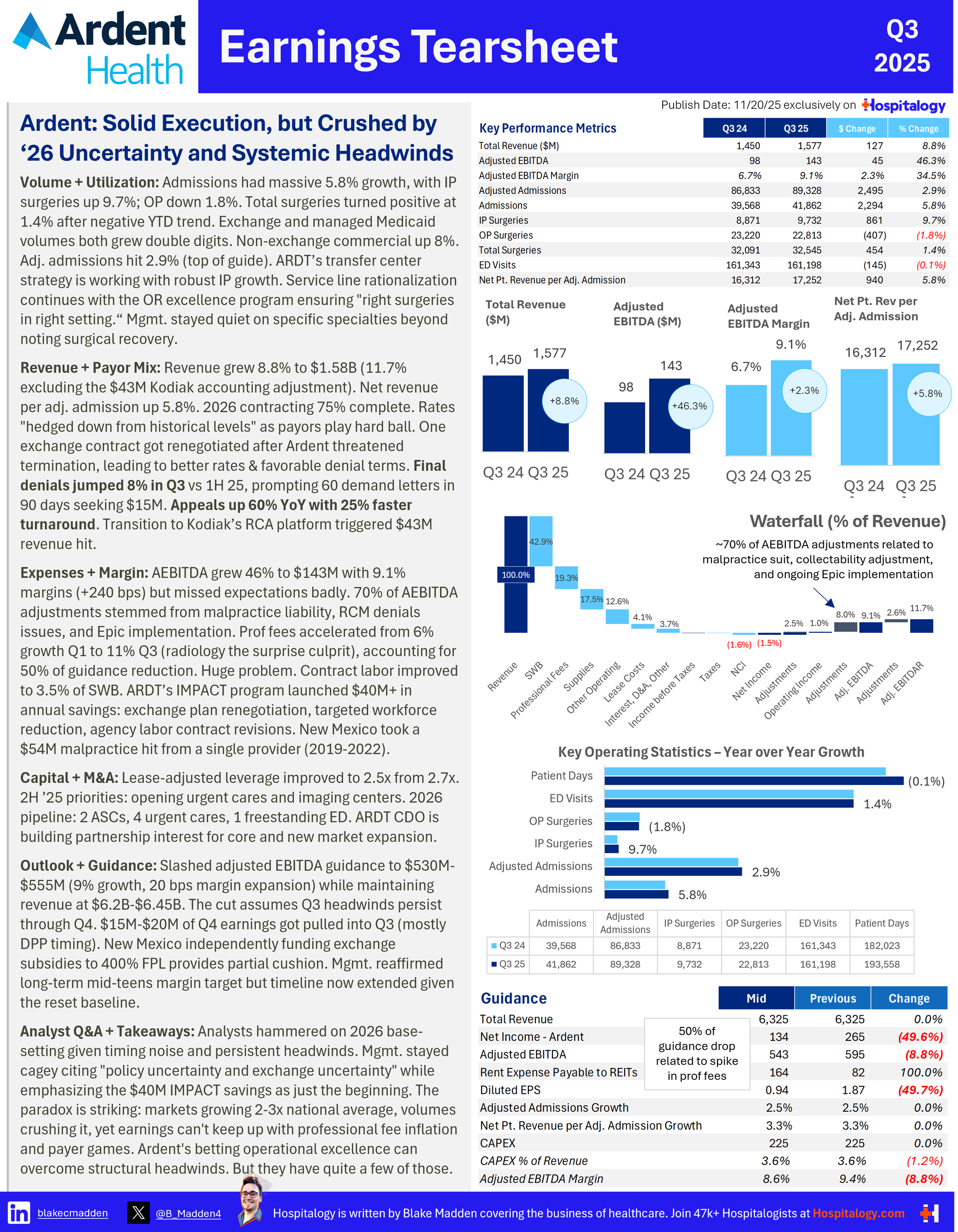

Ardent Health Q3 2025: Volume Can't Save Margin When Industry Headwinds Intensify |

|

|

SPONSORED BY WELLSKY Value-based care only works when your teams, your data, and your network actually work together. A new case study shares how leading ACOs and physician groups are transforming patient care and financial performance through advanced technology, strong collaboration, and dynamic provider networks. It serves as a blueprint, backed by real outcomes, for how other risk-bearing entities can bend the cost curve and move the quality needle. If you're serious about scaling smarter, tighter, more connected value-based care, this is the playbook worth reading.

|

|

|

Recent Hospitalogy community uploads: | |

|

All of this Sherrone Moore stuff happening in real time is crazy. What I'm more concerned with is Michigan's interim head coach, who looks like he'll get his boys ready to play Texas in the Cheez Itz Bowl. Who really is the cheesiest? Biff Poggi is hoping to bring the title home…and then likely gorge on the entire supply himself. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 50,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments