PARTNERED WITH

|

|

|

Happy Thursday, Hospitalogists.

As a Mavs fan, a heartfelt goodbye to Anthony 'Day-to-Day' Davis. You will not be missed. See you guys in 2030 when we're good enough to compete again. |

Alright, enough Mavs trade chatter, let's get down into what you're actually here for: healthcare drama. |

Was this email forwarded to you? |

|

|

Going deeper on an interesting topic, theme, or trend | Healthcare's Dance with Dragons: The Great Payor-Provider Power Struggle of 2026 |

^ this is totally not AI generated. Also, I would never ask for doctors to go into battle! |

If you've been following me for a while, you guys know I love following the publicly traded healthcare titans. To me, it's an extremely important signal to understand where healthcare is headed. This year feels like something has shifted. We're watching something material unfold: the largest health insurer and largest for-profit hospital system in America just reported Q4 results within days of each other, and the contrasting vibes between the two reports was Stark (pun totally intended, RIP Ned. Also Season 8 was a sham). While UnitedHealth Group is preaching austerity and a right-sizing in 2026 (projecting its first declines in growth in…maybe ever?), HCA Healthcare is thriving and basking in the light of peak hospital operations. For the first time in years, providers might actually have the upper hand in the eternal payor-provider struggle for margin supremacy. Welcome to the Dance with Dragons. Alright…sorry. Sometimes I just can't help myself with the epic fantasy metaphors. Let's dive into what actually happened! |

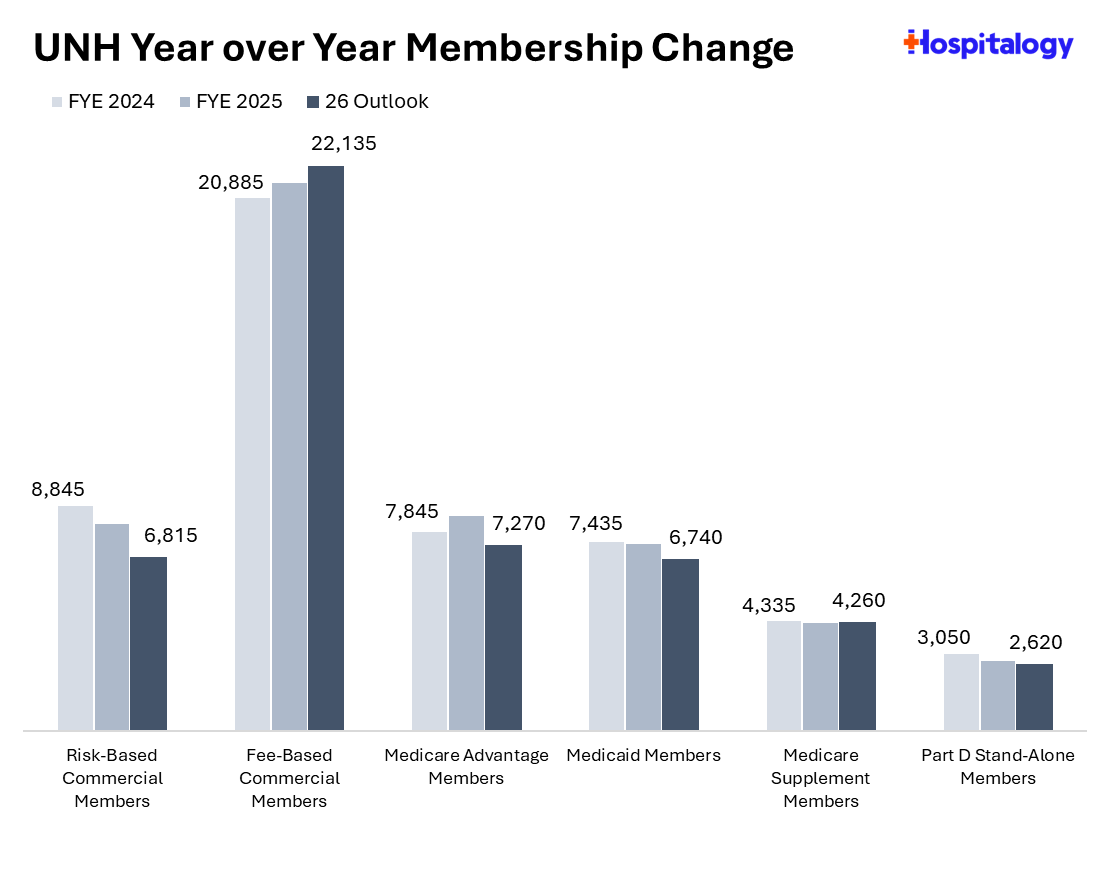

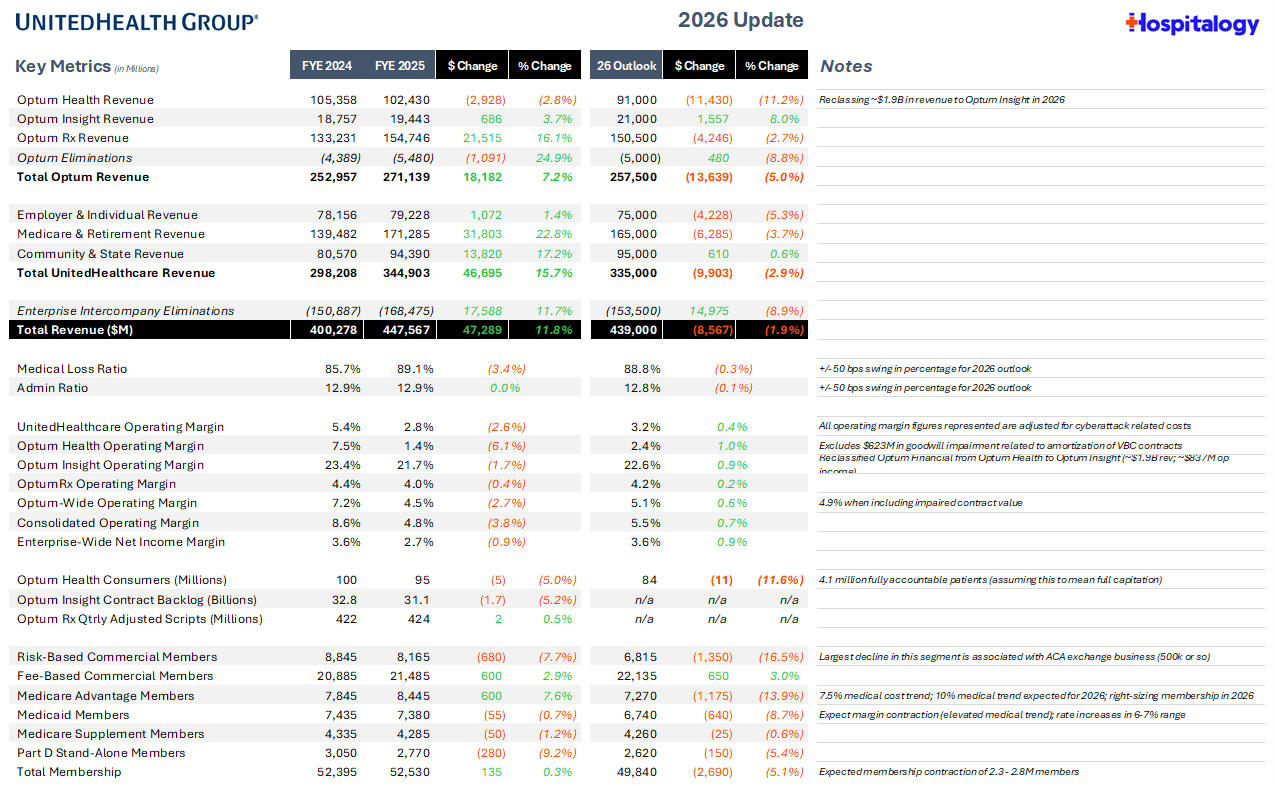

First, I have to give a shout out to UnitedHealth Group for updating their earnings release with a much better, more digestible format including charts!! Credit where credit is due. Great stuff guys. Last week, UNH posted a dismal fourth quarter and 2026 outlook, which included expectations for declining revenue in 2026 (yes, you read that right) as they solve for margin stabilization this year, leading to significant member attrition and some company restructuring. |

On the economic front, UnitedHealth is discussing a reset with language like "measured growth" and "tempered expectations" while HCA is emphatically pronouncing its sustainable margin profile along with prowess about AI as "the Holy Grail" and big data as "the next scalable asset."

HCA is controlled, measured, and ready. UNH is reactive, trying to regain investor trust, and resetting. |

UnitedHealth's Troubles: The Slow Death of the Empire |

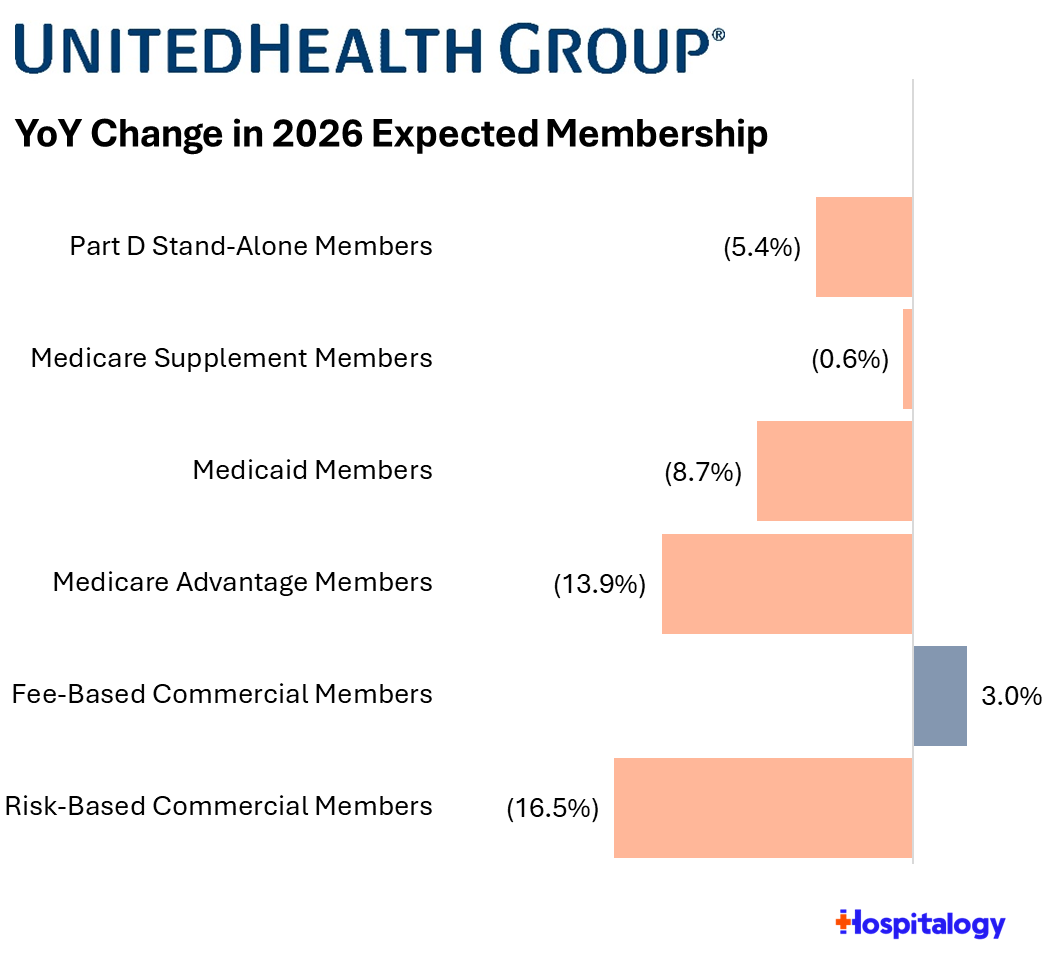

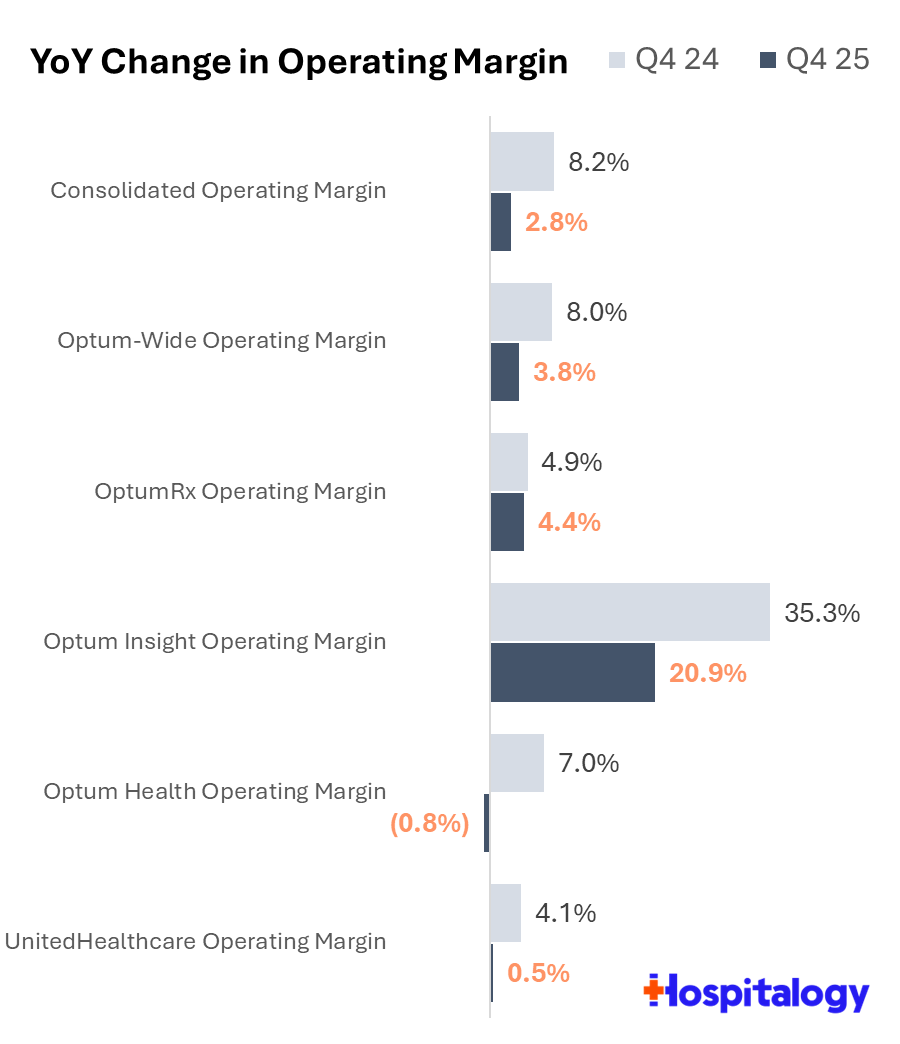

UNH's problems are multi-pronged: Investors are bearish on Medicare Advantage and think it is imploding. Three years of funding cuts totaling $130B+. The 2027 advance notice dropped the day of earnings (brutal timing - probably purposeful tbh) and prompted UNH executives to essentially admit they'll need "very meaningful benefit reductions" and geographic footprint pullbacks if it finalizes. Expected cost trend is 10%, up from 7.5% in 2025. The silver tsunami is here. With the trimmed footprint, MA membership is down 15-17% YoY guidance along with cuts in commercial risk and Medicaid. Then there's Optum. | Optum Health is a mess. Despite ridiculous scale, 100,000+ affiliated providers, and over $100B in revenue, OptumHealth lost money in the quarter and saw significant margin deterioration. The loss contract reserve of $625M for "structurally unprofitable" third-party contracts they can't exit until 2026 tells you they entered poor VBC contracts chasing returns and growth rather than prudence. As a result, they're narrowing the affiliated provider network by 20% (does this mean they're not 10% of physicians anymore?), cutting risk membership by 15%, and consolidating from 18 EMRs to 3. What I want to know is…what took them so long on the whole 'integration' part of vertical integration? |

I sensed lots of shaky commentary around Optum Health and the integrated VBC strategy. My overall read was that they're lost right now on that front and hoping the material changes made will right-size the ship. But to hear UNH management be largely reactive rather than proactive is a major tell. While OptumInsight appears to be the lone bright spot, even OptumRx is under scrutiny given PBM reform talk. Overall, UnitedHealth Group has a ton to answer for investors in 2026 and beyond as it strategically resets from a smaller profitability baseline and invests $1.5B+ in AI and technology initiatives in 2026 alone. For context, health tech received $14.2B in funding altogether in 2025 according to Rock Health. So by my back of the napkin math, that's 10.5% of all healthcare venture investment in 2025. Hemsley cut the fat. Do a word search for 'execution' and it pops up quite a bit from Hemsley throughout the call. "We expect 2026 to be a year of focus and execution, an important one in the history of our company. We have emerged strongly from challenging periods in our past and are committed to that course today. Our team is showing great resilience and energy, and we believe strongly the steps we're taking will pay off." - Stephen Hemsley, UNH Q4 2025 earnings call |

HCA's 2026 Outlook: The Fortress on the Hill |

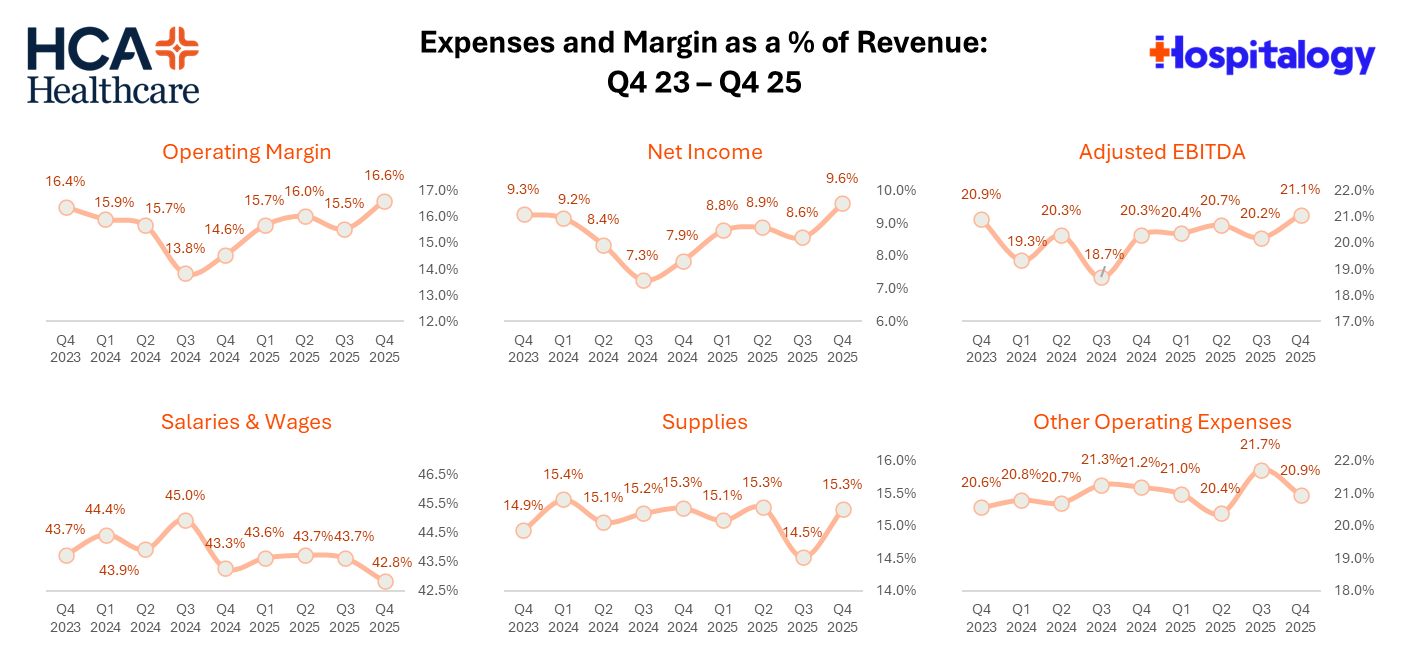

The more healthcare changes, the more HCA stays the same. Operational rigor, prudent capital allocation, and brutal expense efficiency has translated into 20%+ adjusted EBITDA margin as HCA continues to grab inpatient market share from its peers across local markets and expand its ambulatory density (i.e., number of outpatient access points per hospital) over the coming years. |

I noticed a huge tone shift between the two calls. While HCA is increasing capex and noting a robust, emerging outpatient pipeline, UNH is cutting costs, investing in efficiency, and preserving margin. One is investing for growth and the next phase of health system transformation. The other is preserving cash and trapped by its own vertical integration machinations. |

The Structural Shift Away from Payors, and the HCA Advantage |

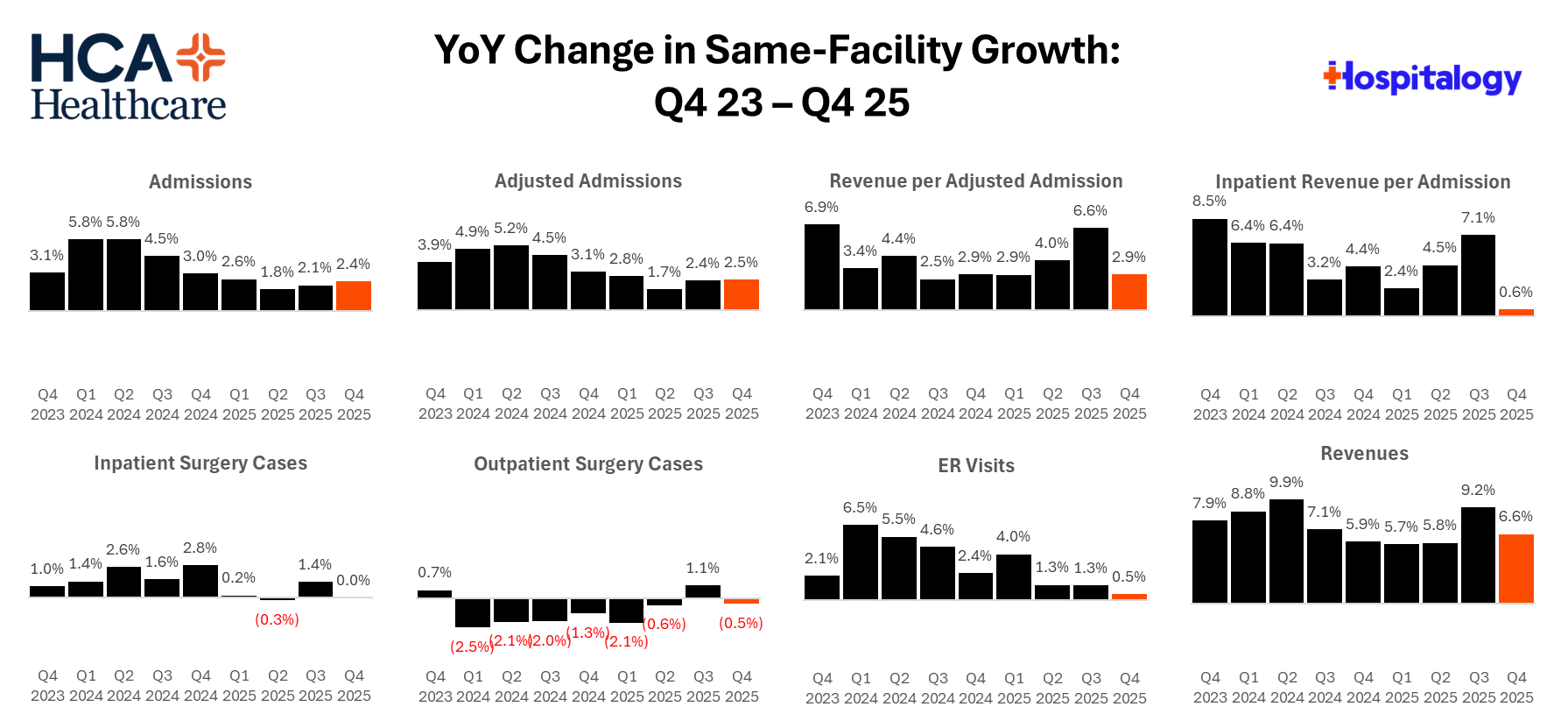

What is playing out in early 2026, Hospitalogists, is a shift of the payor-provider power dynamic to favor providers. When it comes to the titans of the industry, HCA and other price makers are emerging with the upper hand. Here are many points and economic forces in favor of both HCA and hospitals: Density leads to pricing power. HCA notches reimbursement rate increases year after year in the mid-single digits translating to long-term growth of 3-4%. At the same time, they're simultaneously improving working capital through faster claims payment all the while investing in resources like ambient scribing and coding and documentation to code better, faster, and I presume more accurately. Payors are paying up and paying faster. When UNH talks about commercial trend approaching 11%, that money flows directly to provider bottom lines. | HCA sticks to blocking and tackling and a predictable formula. UNH poured billions into Optum Health to own the care delivery apparatus, and their exposure to risk adjustment changes and high utilization trend with member acquisition has led to material decline in performance. Meanwhile, HCA, as always knows its core competencies: run efficient hospitals, suck in more inpatient market share, stay in fast-growing attractive markets, get paid for what you say you do, add outpatient facilities to networks, and assume meaningful value-based care will never happen. Look at the consistent same-facility growth as a result of this playbook: |

Ambulatory Buildout: Hospitals can invest in asset-light ambulatory assets to fuel growth, enter new markets, and accrete margin. HCA has noted that they want to hit 18-20 ambulatory sites per hospital by 2030. This number is up from…I believe 12-13 sites a couple of years ago. I did a quick exercise to math out what that means as far as growth for the organization: |

If my back of the napkin math is right, HCA will add up to 1,200 ambulatory facilities in the coming years as it builds out de-novo hospital sites and likely acquires attractively valued physician and associated assets, acquiring density in its target markets and inevitably gobbling up market share. Favorable Labor Market Environment: At last measure, HCA's contract labor as a percentage of overall salaries & wages was 4.2%. Add to this HCA's significant expense leverage over the last few years (with a caveat for professional fees and acuity-driven supplies growth), and you have a recipe for expanding margins. |

One final, softer point I'd like to make is that despite hospitals' industry reputation as the highest cost care setting, they also have considerable branding goodwill across the country. People remember where they delivered their baby. They usually blame poor consumer experience on the insurance and feel the effects of the healthcare industry most acutely through insurance, when they are denied care. So for that reason, lawmakers tend to invite managed care executives to Capitol Hill to bemoan insurance premiums, PBM practices, and corporatization of healthcare. |

Here's a quick spoiler alert for Game of Thrones: dragons can die, too. Magic dries up. Both payors and providers, uniquely, are facing legitimate headwinds in the coming years: HCA's challenges: - Exchange coverage losses (modeling 15-20% decline in HIX volumes) deteriorating commercial mix

- Supplemental payment uncertainty and associated Medicaid disenrollment threat

- Continued physician cost inflation

UNH's challenges: - Medicare cost trend at 10%, commercial at 11%

- MLR stuck at 88.8% (up 340 bps from 2024's 85.5%) - elevated utilization environment that hits all company segments (save for seemingly SCA)

- Membership contraction of 2.3-2.8M lives across all segments

- 2027 MA rates that "don't reflect reality" but operating in a society that hates your guts

- PBM reform

But here's the asymmetry: HCA's headwinds are policy-driven and potentially reversible (grandfathered CMS approvals, Texas ATLIS reinstatement, Rural Health Transformation Fund), and they have meaningful answers to these challenges. UNH's headwinds are structural and multi-year (utilization isn't going down, funding isn't going up, Optum needs years to fix, vertical integration strategy was a financial engineering farce, PBM reform on the horizon). |

Implications for the Healthcare Industry |

The HCA-UNH dynamic is a microcosm of the broader payor-provider landscape entering 2026: - For hospitals and health systems: Price makers have leverage while everyone else is looking to survive. Meanwhile, paradoxically, payors are struggling with medical cost trends they can't bend coupled with dismal government support. BUCAs are getting attacked from multiple angles between PBM, MA rates, and risk adjustment. Dollars are flowing into specialty drugs. Ambient scribing and CDI AI initiatives give them the short-term upper hand.

- For payors: The vertical integration arbitration game is up. Owning providers doesn't automatically translate to better economics. We're going to see an emphasis on the whole 'integration' part in 2026 (what took Optum so long to pare down to 3 EMRs anyway?). We're also going to see an intense focus and capital deployment on the AI and technology front. Downcoding, prior auth, price transparency, and other levers will come into play in a major way.

- For ambulatory groups and risk-bearing orgs: Watch UNH's Optum Health restructuring. They're cutting 20% of affiliated networks and 15% of risk membership. Where do they go? Independent practices? Competing MSOs? Health systems building their own ambulatory networks? Also, Optum noted its intention to stay out of specialty risk. To me, that's a hedge against rising utilization in at least one part of the company with SCA.

- For everyone: An overarching theme I'm seeing again and again in 2026 is…refocusing on the core. Let's shed the hospitals that we can't support. Get rid of the parts of the network that are higher cost, lower quality, or in unattractive markets. Double down on what's working. Whether you're payor or provider, take lessons from HCA, CommonSpirit, Ascension, UnitedHealth and others, and assess where you actually need to be.

|

Neither side wins permanently in healthcare's eternal tug-of-war. Payors will eventually reprice their way back to target margins. Providers will eventually face volume and reimbursement pressure. Government austerity will rein in specialty drug pricing and cost growth. The pendulum swings.

For now though, 2026 belongs to the providers.

The dragons are dancing, Hospitalogists. And my question is…when does the magic end? And does the patient get burned in the process? |

|

|

You could be an investor in early-stage healthtech startups. This week, we're partnering with Alumni Ventures to give Hospitalogy readers early access to healthcare startup opportunities, including some of today's most exciting healthtech companies like Ōura Ring, Function Health and Pendulum Therapeutics. Co-invest alongside top VC firms like a16Z, Lightspeed, and Khosla Ventures. Access includes: - Curated deal flow of high-potential healthtech startups

- No cost, no commitment to join

- Invest only in companies that interest you

Get the details about the opportunity to join Alumni Ventures Healthtech Syndicate. |

NOTE: This is not an offer to sell, or a solicitation of an offer to purchase, any security. Example companies are provided for illustrative purposes only are not necessarily indicative of any AV fund or investor, and are not available to future syndicate members, except potentially in the case of follow-on investments. Venture capital investing involves substantial risk, including risk of loss of all capital invested. |

|

|

Anthropic ads have taken the internet by storm, taking direct shots at OpenAI and ChatGPT, imagining a (caricaturized) world with advertisements in ChatGPT responses. They are actually hilarious and enjoyable to watch. Like, I just watched 4 minutes of ads from Claude - not only because it is the best AI, but because they are incredibly relatable given the immediate ability to recognize 'AI-speak' from the humans within the ads that are portraying ChatGPT. And to cap it all off, we have Dr. Dre's 'What's the Difference' - a classic, all-time hip hop beat to boot. Chef's kiss, perfection, no notes from me. See you guys at the Super Bowl where I'm sure we'll be getting more spicy ads from the likes of Hims & Hers. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

| |

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 67,600+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments