Happy Thursday, Hospitalogists! 2 things for you today in the intro for you to skip past read: - Nearing last call on registering for my ViVE happy hour. Space is limited so we are intentionally curating it for senior folks who work in ACOs, risk-bearing orgs, payvidors, and hospitals and health systems. Register here!

- I have a 1.5 hour block at ViVE from 2:00 - 3:30 on 2/23 and am looking for interesting folks across the ecosystem to interview. Let me know if you're interested by replying to this email!

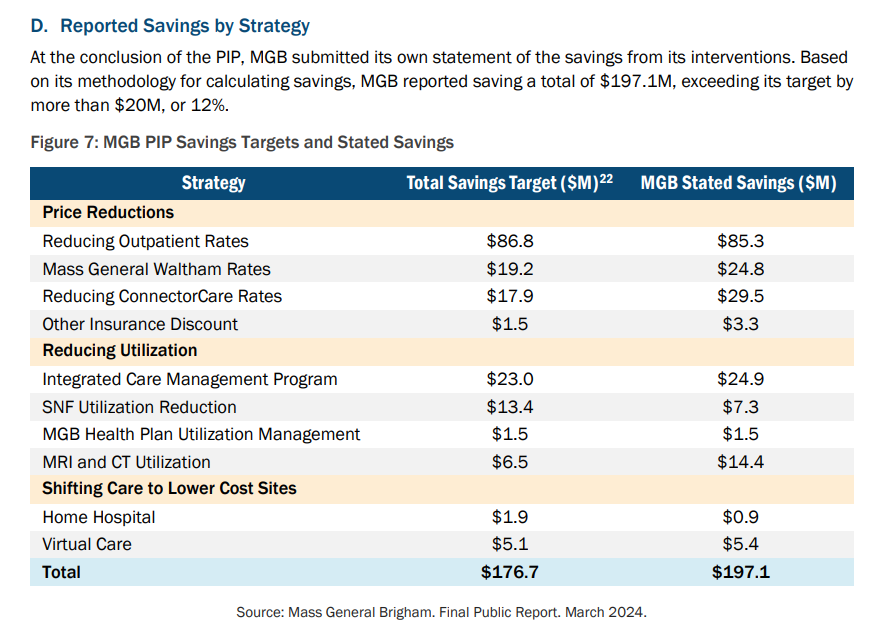

Today we're taking a quick dive into Mass General Brigham since I went down the rabbit hole and couldn't help myself with some analysis of their 2025 performance. If any of you guys are closer to this market or to MGB feel free to drop me a note with your thoughts on the below! |

Was this email forwarded to you? |

|

|

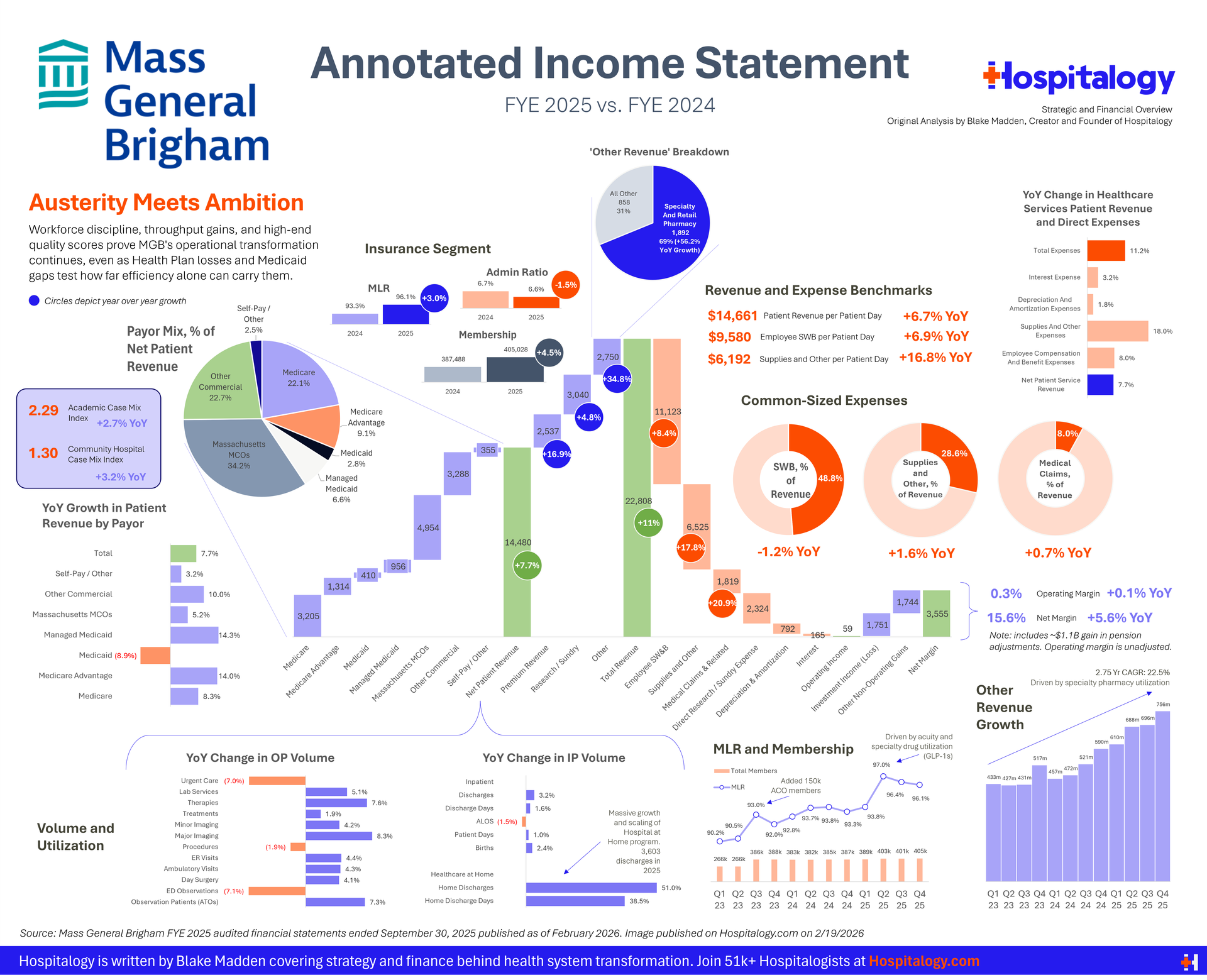

BLAKE'S BREAKDOWN: MGB's 2025 in Charts |

Mass General Brigham (MGB) is massive, with ~10 hospitals, a sprawling footprint, 7,000+ employed physicians, and everything else an academic medical center entails. It is also, for this reason, at the center of a lot of stuff happening in healthcare right now. Off the top of my head, I can think of some of the following issues and themes related to MGB that are more interesting/compelling: - As a premier academic medical center they're trying to maintain access to grants and funding for system wide and public health research initiatives. AMCs in general also are super high cost and a huge resource demand that needs to be justified.

- MGB split from Dana Farber on cancer care and are rebuilding their oncology vertical.

On the AMC note, they are constantly in the state's headlights for regulatory cost review and were put on a performance improvement plan to cut costs (which appears to have concluded). No Massachusetts health system operates under more regulatory scrutiny than MGB. Oversight seems to have intensified rather than relaxed with recent cost containment and market regulation legislation in MA.

|

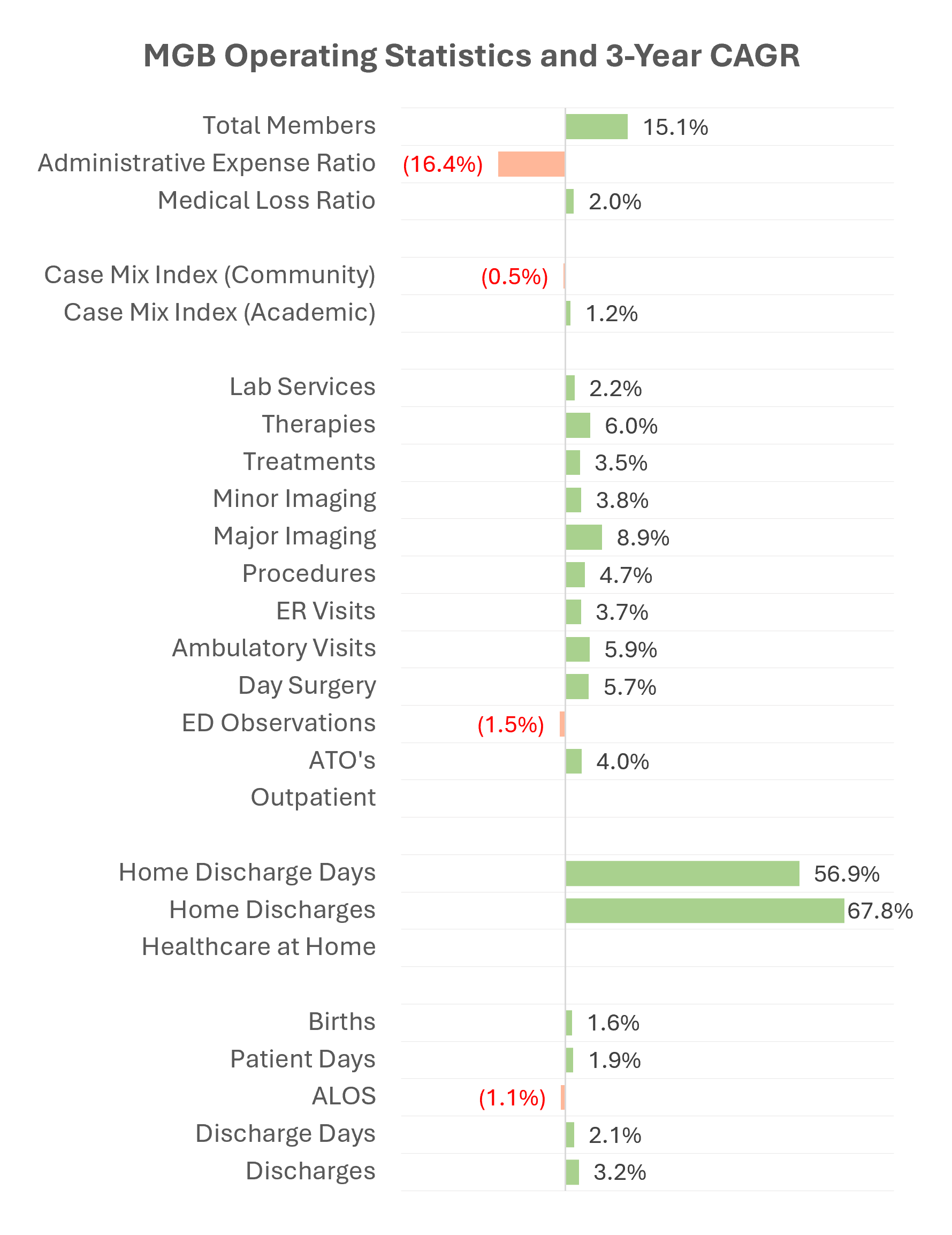

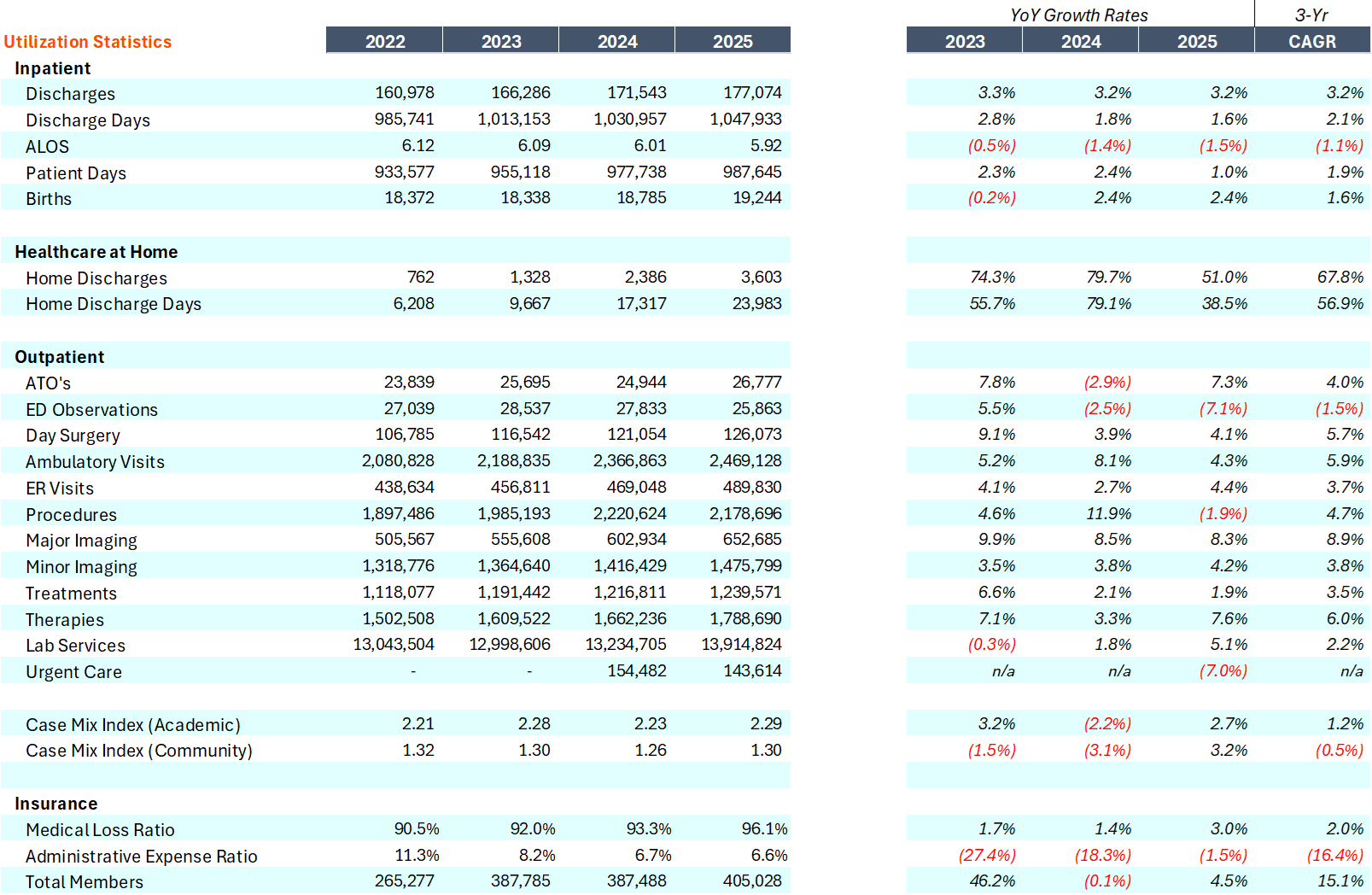

- MGB operates one of the largest hospital-at-home programs in the country with over 3.6k discharges in 2025, noticeable, but still little more than a rounding error on total discharges (around 2%).

- Their provider sponsored plan has seen significant membership growth in recent years - from 265k in 2023 up to 405k in 2025, and a steady upward march of associated medical costs.

- Optum and other formidable players are present in the market.

- Enterprise wide operations are breakeven, and MGB's direct hospital revenues and expenses - at least by my calculation - are heading the wrong direction, serving to compress margin performance further.

- MGB is still in a powerful position given balance sheet strength as market returns and other non operating items have bolstered its financial performance.

|

MGB seems to be a bit in reset mode given the aforementioned dynamics. Despite some headwinds in their plan and breakeven profitability on the operations, MGB has a strong balance sheet on an enterprise wide basis, and their main adversaries are probably more political in nature than anywhere else.

The below should hopefully give you guys a good snapshot as to the economic state of MGB across acuity, payor mix, revenue segments, expense trend, reimbursement benchmarking, and more. I kind of like this 'annotated income statement' waterfall graphic, but if you guys think it's too noisy, let me know: |

In my mind no strategic challenge facing MGB is more consequential than the loss of its Dana-Farber partnership. For nearly 30 years, Dana-Farber Cancer Institute and Brigham and Women's Hospital operated through a joint venture called the Dana-Farber/Brigham Cancer Center. MGB's new oncology strategy centers on the Mass General Brigham Cancer Institute, announced in late 2024. In March 2025, MGB committed approximately $400M over four years to build out capabilities with network leakage and physician alignment challenges to resolve. In 2026, MGB's success lies in ~3 key themes: - Sustaining operational efficiency and improvement in hospital operations (labor inflation and supplies inflation mitigation)

- Continuing to transition its cancer vertical

- Overcoming and navigating regulatory constraints

|

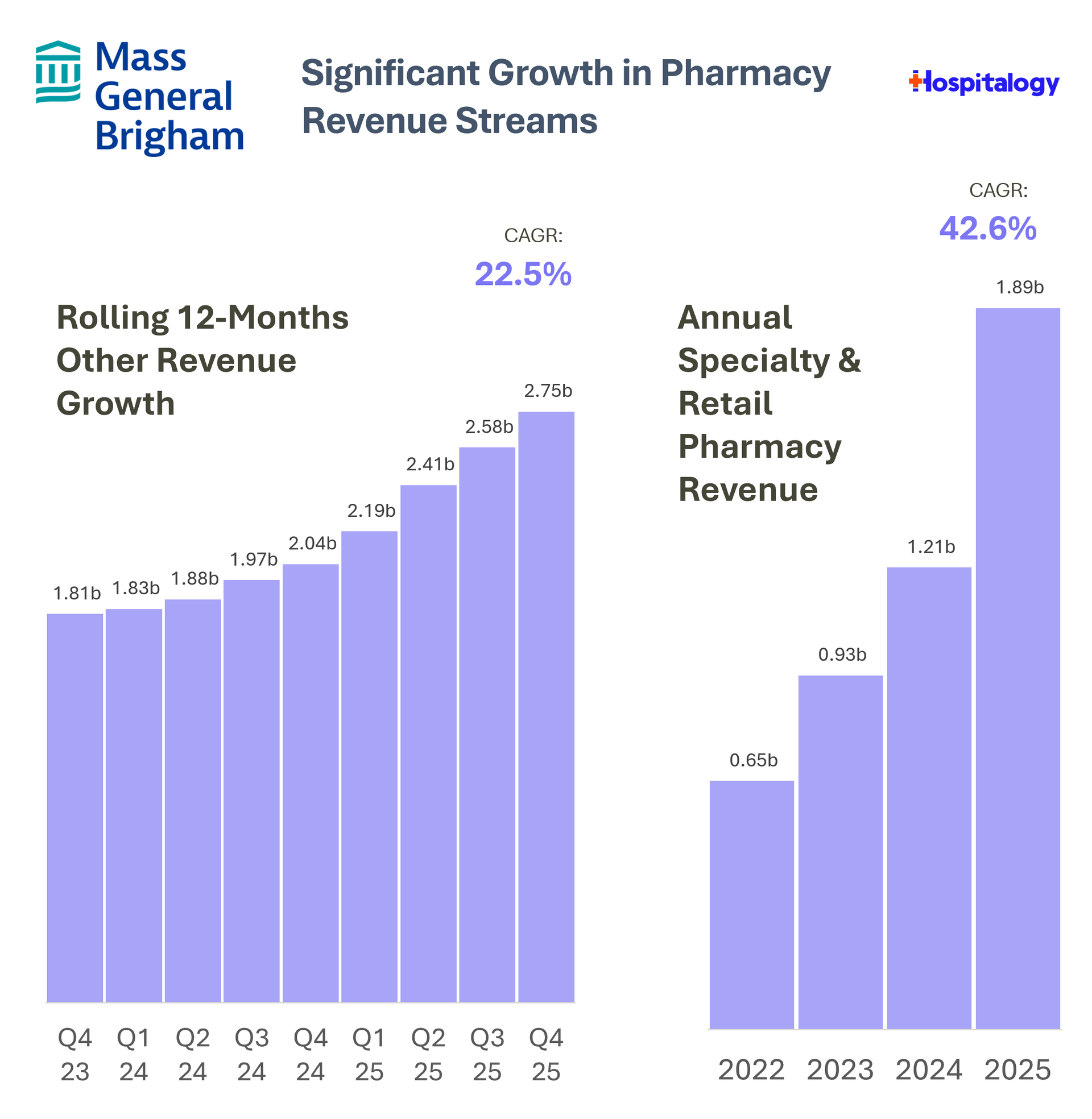

#2 - MGB's Accelerating Growth in Pharmacy |

One of the more interesting trends I found worth discussing - especially given this dynamic seems to be present across a multitude of other health systems (anecdotally, Ascension and Fairview to name a couple) is the acceleration of growth in pharmacy related revenues. On the MGB income statement this line item sits in Other Revenue which is broken out on an annual basis. But the accelerating trend is very clear. Over the past 3 years this revenue segment has increased 43% compounded annually (albeit on a low basis to begin with), coinciding with a rise in specialty drug utilization and, again, without perfect knowledge, what I imagine to be other levers like 340b, pharmacy growth, and service line changes in oncology. |

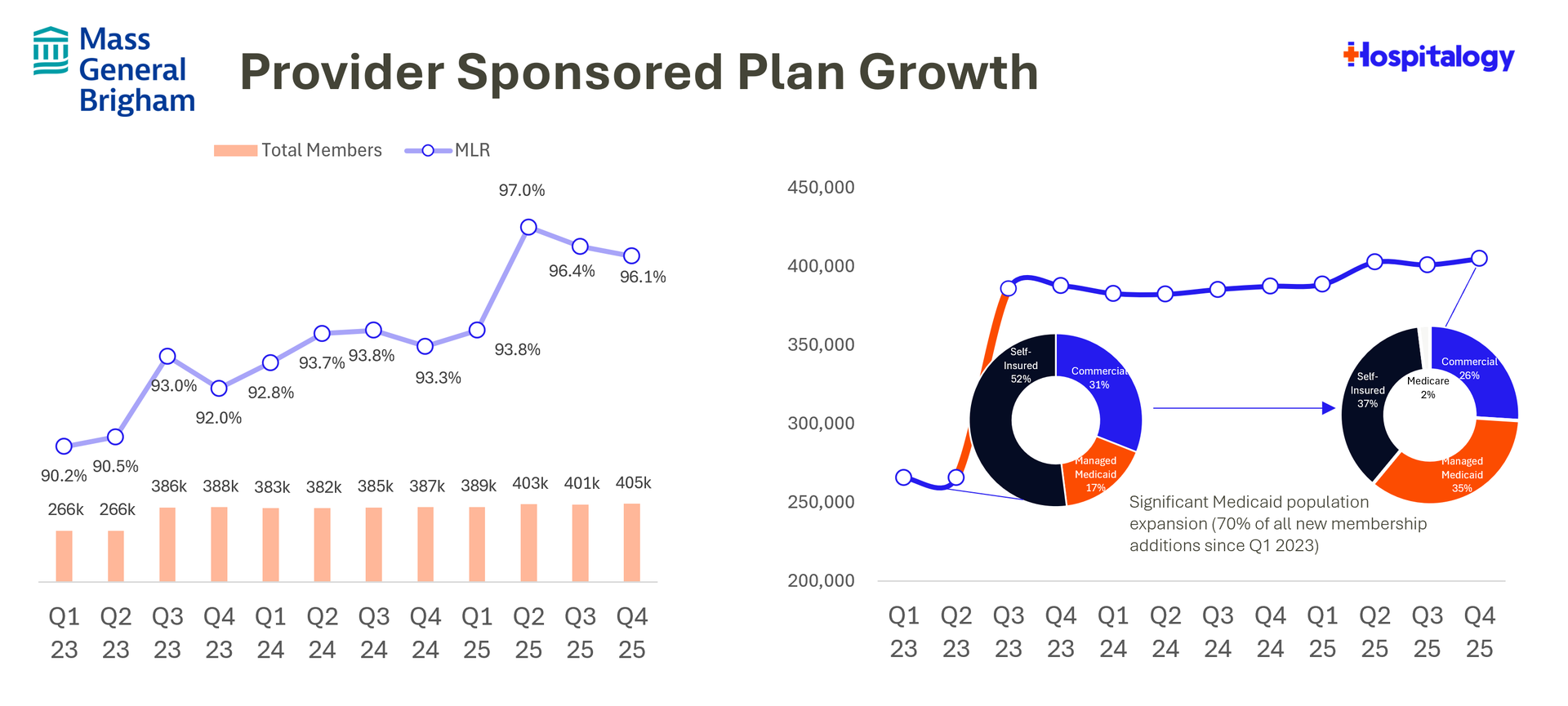

#3 - MGB's Provider Sponsored Plan MLR is Exploding Upward |

Another trend that could be driving pharmacy growth explosion is the rise in plan membership at MGB's provider sponsored plan, and MGB even notes as much in its management discussion, attributing MLR increases to rising acuity and increased pharmaceutical costs (GLP-1s). Since fiscal 2023, MGB has seen over 50% membership growth to just north of 400k members. ~70% of those members enrolled in Medicaid, and the chart on the right shows you the notable mix shift this enrollment created. While MGB's plan has been stellar in managing administrative costs, its medical costs have only grown since ingesting the management function of its ACO through MassHealth, taking on a probably-high-cost population, and dealing with issues that every payor has been dealing with (high utilization and specialty drug spend) despite being sub-scale to the BUCAs. | #4 - Huge Growth in Hospital at Home |

Hospital at home continues to be an interesting and compelling model for the health systems that can pull it off (MGB, Advocate/Atrium, etc.) - while we saw some consolidation and value destruction on the vendor side, health systems can make the program work for them to push less lucrative observation stays out to the home - an increasingly important function given the downcoding and other measures being done by payors in this arena in areas like Medicare Advantage. Overall highlights include better throughput management with ALOS dropping, and solid discharge and ambulatory growth across the board. |

Here's a look at the year over year trends as a bonus: |

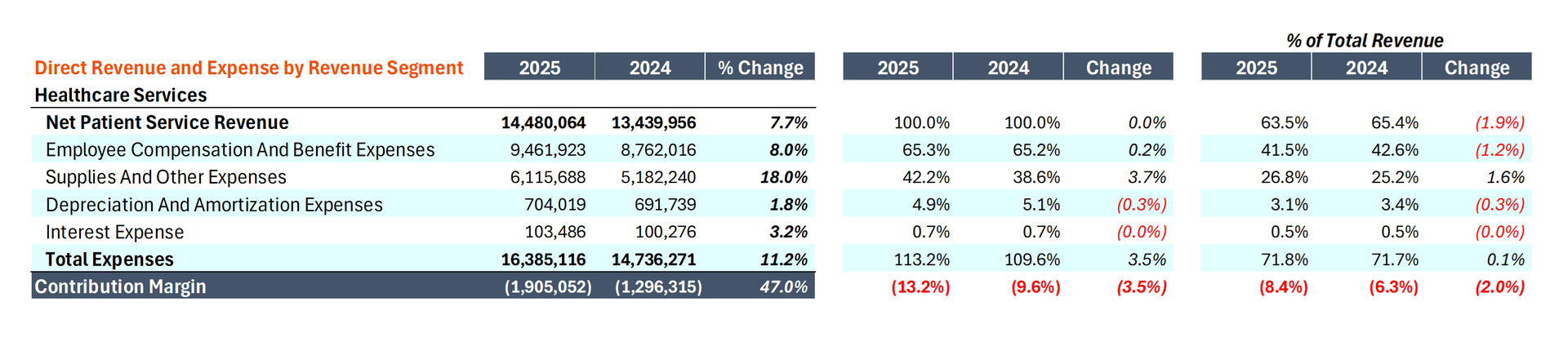

#5 - Things Don't Look Great on the Hospital Segment |

On a pure patient revenue to direct expenses basis (reported as a schedule later on in the audited financials) you can see a couple of the more crucial expense categories growing far and away above patient revenue - labor costs and supplies. My guess is that those supplies cost translate into the other revenue / pharmacy growth, so the delta probably isn't as bad as it looks here. But nonetheless without having inside knowledge, MGB seems to be in a delicate position on the labor front even after layoffs during the year. The workforce restructuring is paired with a broader clinical integration initiative merging 34 separate departments across MGH and Brigham into 18 unified departments. MGB reported a $1.0B in Medicaid and Health Safety Net shortfalls in 2025, up 16% ($141M) from the prior year. For context, that's 4.4% of total operating revenue going to subsidize care for low-income and uninsured patients. Add in the community health ($210M), research ($190M), and education ($300M) investments, and mission-related spending hits approximately $1.7B, or 7% of revenue. This is the AMC paradox in action: MGB's research preeminence and teaching mission generate enormous societal value, but they also create structural cost burdens along with political pressures in garnering top dollar rates otherwise. |

That's it for me on the analysis front. I'm sure there are several of you out there with interesting takes or things to say on the MA market, or things happening within MGB specifically. If that's you, I'm all ears because I'm always keen to learn how I can make my analysis better, or what's happening organizationally as these tectonic healthcare plates shift all around you. Drop a note! |

|

|

SPONSORED BY AMPLIFYMD Just a few days until ViVE! I'm looking forward to discussing and viewing the latest in digital health innovation. I also want to invite you to stop by AmplifyMD's booth #1042 to see why their key message at ViVE is "Deliver remote care faster than in-person needs." By orchestrating the entire consult workflow with AI, automation, and data integrations, AmplifyMD is making new coverage models possible at scale, while saving health systems 50% over legacy program operating costs. Come meet the team.

|

|

|

I am someone whom you would call 'extremely deficient' AKA, dumb, when it comes to cars, and I don't plan to change that anytime soon. But I am also horrible at keeping my car up to date on all of the various things. So about 5 years ago, we ran over a pothole and broke part of the bumper of our Honda Civic and there's now this one part of the bumper that hovers barely over the pavement and scrapes whenever we drive over a low point. Well, the other day I was driving in a rain storm, and driving through the heavy rain and water made the situation worse. Fast forward to today - I got in the car to drive it and immediately heard an excruciating scraping noise…and proceeded to drive all the way to my destination in embarrassing fashion with judgmental stares from fellow drivers.

Anyway after a 5 year hiatus I'm finally taking in the ole beater into the body shop tomorrow. Have a great weekend everyone! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 66,600+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments