PARTNERED WITH  |

|

|

Happy Thursday, Hospitalogists! Tenet reported Q4 earnings this week, and if you've been following the multi-year transformation story here, Q4 was another chapter in what's becoming one of the most compelling operational turnarounds in the hospital sector over the past several years. If HCA is 1a, Tenet is 1b and actively investing in a key growth vector in healthcare: outpatient migration.

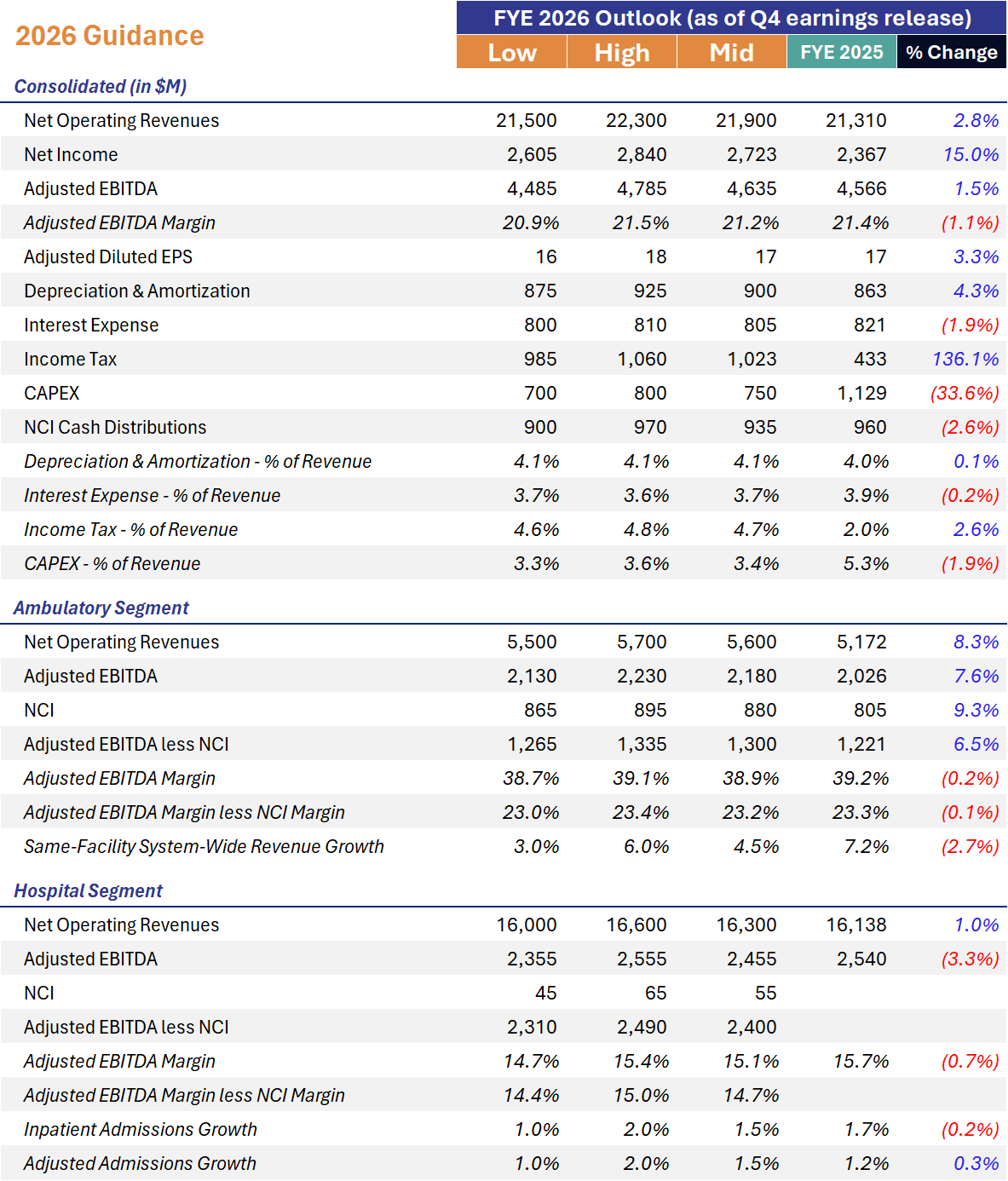

But the 2026 story is where it gets interesting, because Tenet is now navigating a genuine crosscurrent: a powerful organic growth engine running headfirst into structural headwinds in a $250M EBITDA expected hit from the expiration of enhanced ACA premium tax credits, and a pressing need to prepare for choppy OBBA waters in 2028 and beyond.

Let's dive into the deep end. And as always, tell me what I'm missing. That's how I learn, baby. |

Was this email forwarded to you? |

|

|

SPONSORED BY AMPLIFYMD Hospitals still run specialty coverage on workflows that weren't built for modern virtual care. Consults depend on ad-hoc communication, manual routing, and fragmented information, slowing decisions and straining specialist capacity. AmplifyMD replaces this fragmentation with a true operating layer for virtual specialty care. The EHR-integrated platform orchestrates the entire consult lifecycle — activation, routing, communication, documentation, and performance visibility — and assembles relevant clinical data into a single, ready-to-use report. This results in faster consults, 2x remote provider efficiency, lower operating costs, and scalable access to specialty care. Check out AmplifyMD's white paper. |

|

|

BLAKE'S BREAKDOWN: THC Q4 Analysis |

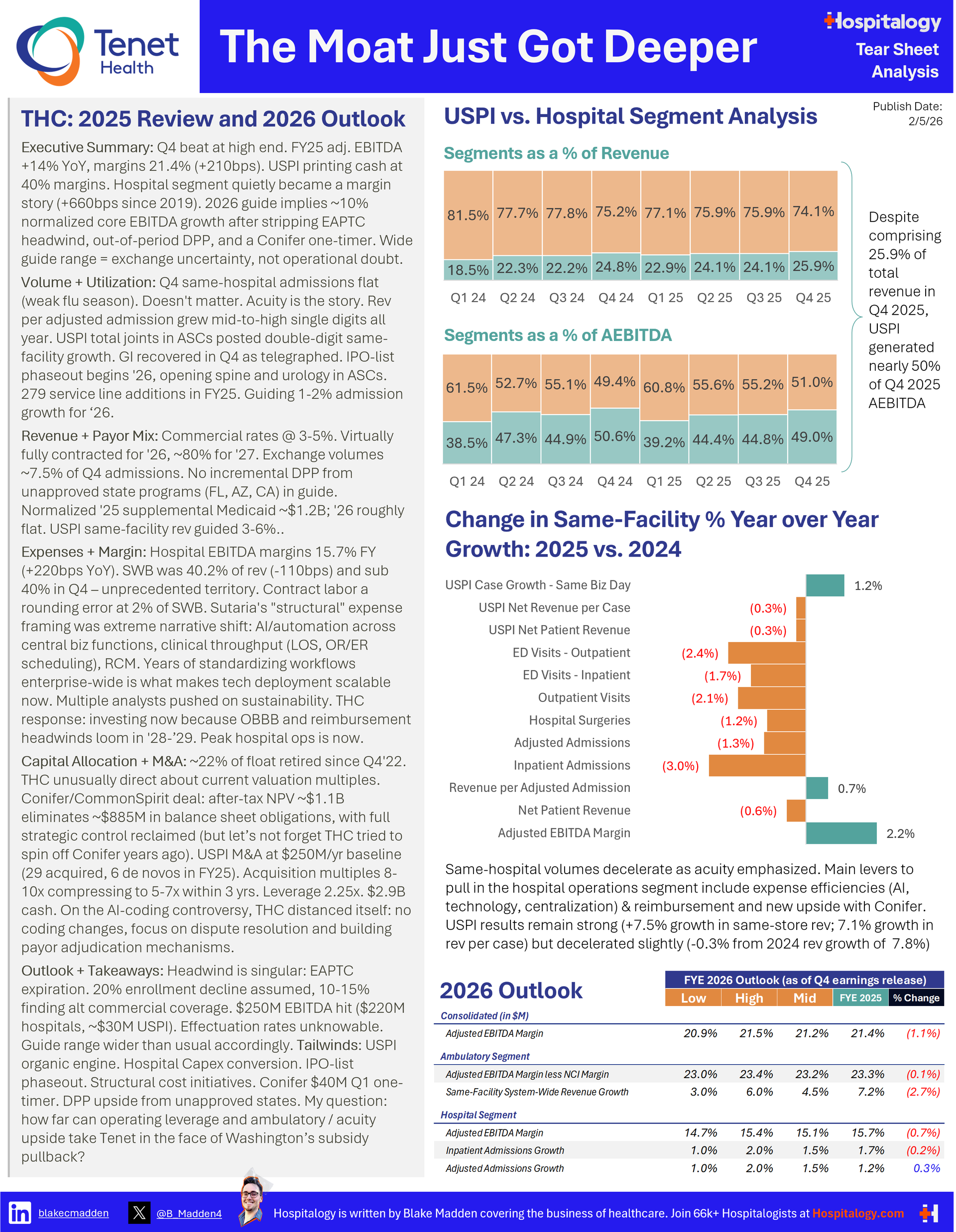

Tenet Healthcare: The Moat Just Got Deeper. |

Executive Summary: Conifer Buyback helps bolster balance sheet. Announced in late January, Tenet acquired 23.8% of Conifer equity from CommonSpirit. Full strategic control of Conifer now sits with Tenet. Still, I can't help but remember when Tenet wanted to spin off Conifer not too many years ago…then decided to retain it ~6 months later.

USPI Remains the Crown Jewel. 12.2% same-facility total joint growth in ASCs. 35 facilities added, 279 service line additions. 2026 guide: $2.13B-$2.23B EBITDA with 3-6% same-facility revenue growth. Inpatient-only list phaseout presents a compelling narrative for a multi-year tailwind in areas like spine and urology. USPI operated 267 total facilities system-wide in 2017. Now in 2025, that number has swelled to 559. I expect to see some further acceleration in 2026 assuming M&A returns to the ASC space.

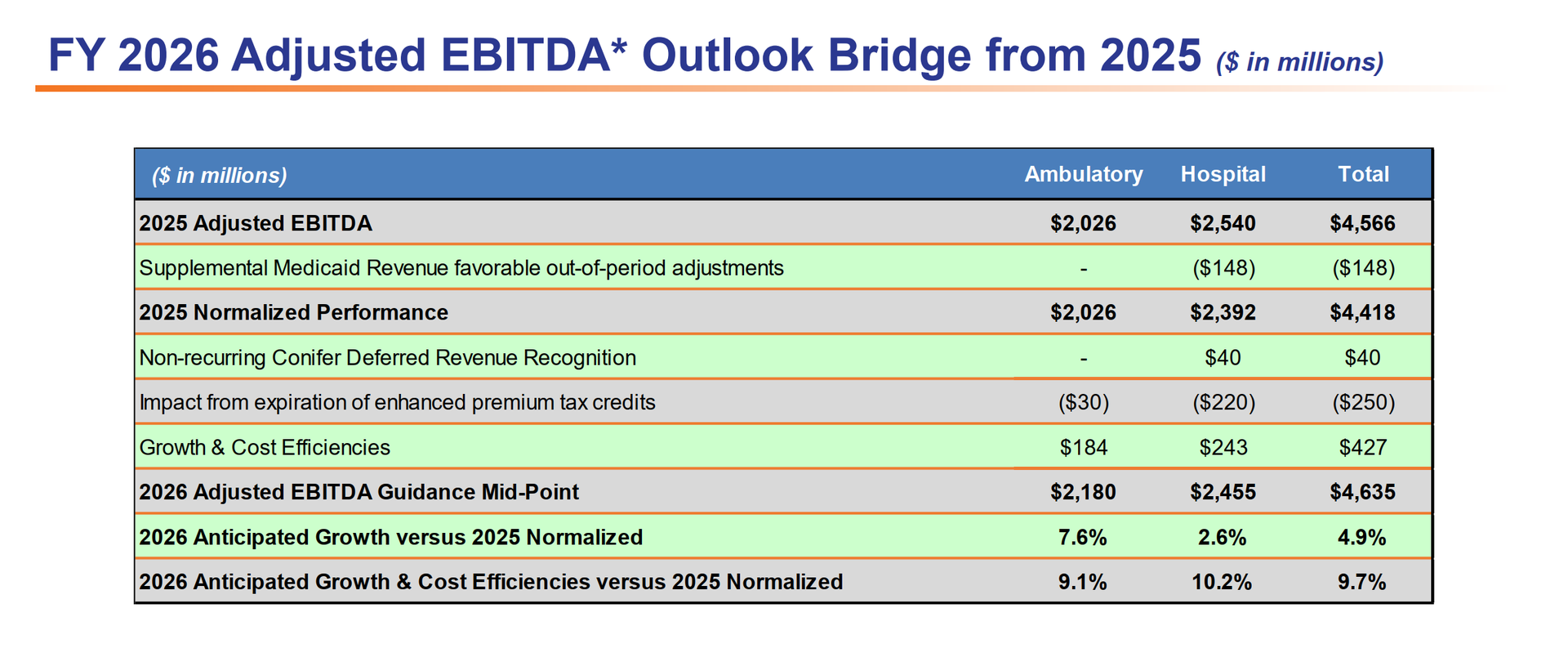

Headwinds include supplemental payments timing and ACA subsidy expiry. Tenet assumes a 20% reduction in ACA exchange enrollment (exposure in AZ, MI, CA), with only 10-15% of those individuals finding alternative coverage (commercial). The $250M hit is split $220M hospitals / $30M USPI. The below slide was helpful to digest both the 2025 adjusted baseline (without Medicaid supp pmts) and walkthrough to 2026 adjusted EBITDA. After normalizing for $148M of out-of-period supplemental Medicaid and the $40M Conifer deferred revenue recognition, core EBITDA growth is expected at ~10% at the midpoint.

I should add that 10% expected growth is pretty rich for a hospital operator in general. Take HCA's guidance for instance. It's expecting ~3% growth in adjusted EBITDA. Big delta. Especially with the dynamics at play and decelerating growth. One might ask at what point does the acuity story and rate escalation from payors end, because volumes don't seem to be growing any faster. |

Levers for growth and operating leverage include Tech + Automation + Offshoring, and focus on acuity. Tenet drew a clear line between traditional annual belt-tightening and a multi-year technology transformation involving AI-driven denials management, automated coding, workflow optimization, and more centralized business office functions. Tenet is prepping for years out when things get extra tight under OBBA, in 2028 and beyond. |

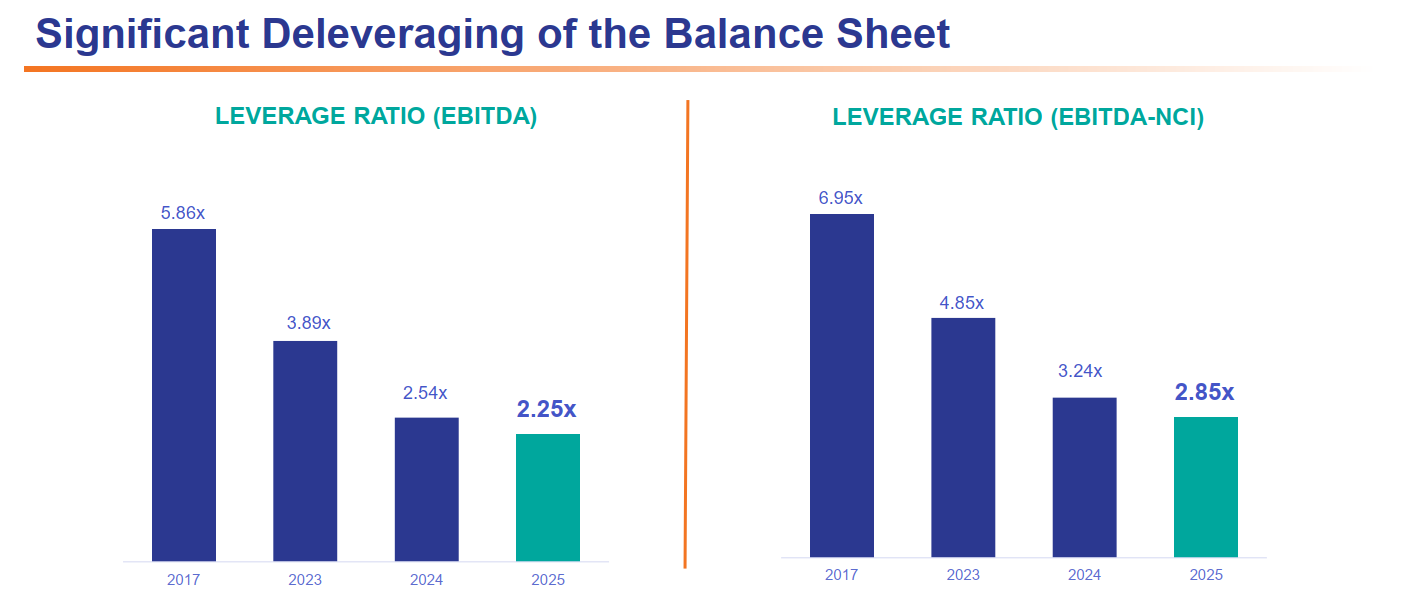

Deleverage means Ambulatory Capital Deployment at Full Throttle. With $2.88B cash on hand and 2.25x leverage, commentary about dismal valuation multiples on the earnings call, expect Tenet to aggressively deploy capital in USPI ($339M in M&A spend in 2025) and on share buybacks to boost profitability. Plus, fewer (47) hospitals means lower capex requirements. - "We attempt to operate and behave like a company that trades at a higher multiple. We will deploy our balance sheet like an organization that recognizes that the multiple has a valuation that's attractive to buy back shares."

|

Starting with the Conifer Transaction: The Wildcard |

Conifer serves as a potential catalyst for Tenet and a foot in the door into the health IT world. Obviously this was the big transaction for Tenet and held a large section of the call. Conifer has been providing RCM services to CommonSpirit since 2012 under a contract that ran through 2032. CommonSpirit held 23.8% equity in Conifer. Tenet hadn't made cash distributions from that JV in the last decade, which caused a massive buildup of redeemable NCI and other liabilities on the balance sheet. The deal mechanics: - CommonSpirit pays Tenet $1.9B over 3 years ($540M in Q1 2026, then $453M annually in Q1 2027/28/29)

- Tenet pays $540M to CommonSpirit to eliminate the capital account and redeem the 23.8% equity stake (effective 1/1/2026)

- The Q1 2026 cash flows net to $0 ($540M in, $540M out), but the subsequent $1.359B comes in free and clear over 2027-29

- ~$100M annual NCI expense reduction in 2026 (because Tenet now owns 100% of Conifer)

- ~$1.65B of revenue from contract termination recognized on the income statement (excluded from adjusted EBITDA)

- Some tax considerations and some adjustments to the balance sheet as a result of the above.

A brief note is that Tenet now has full strategic control over Conifer's investment roadmap. Sutaria was careful not to throw shade at CommonSpirit as a JV partner ("I don't want to leave the impression that one party was constraining the other") especially since CS seems to have its own aspirations in RCM, but the message was crystal clear: decisions around AI investment, offshore expansion, and client growth strategy will now move faster without needing consensus from a JV partner with different strategic priorities. |

USPI: The Growth Engine That Won't Quit |

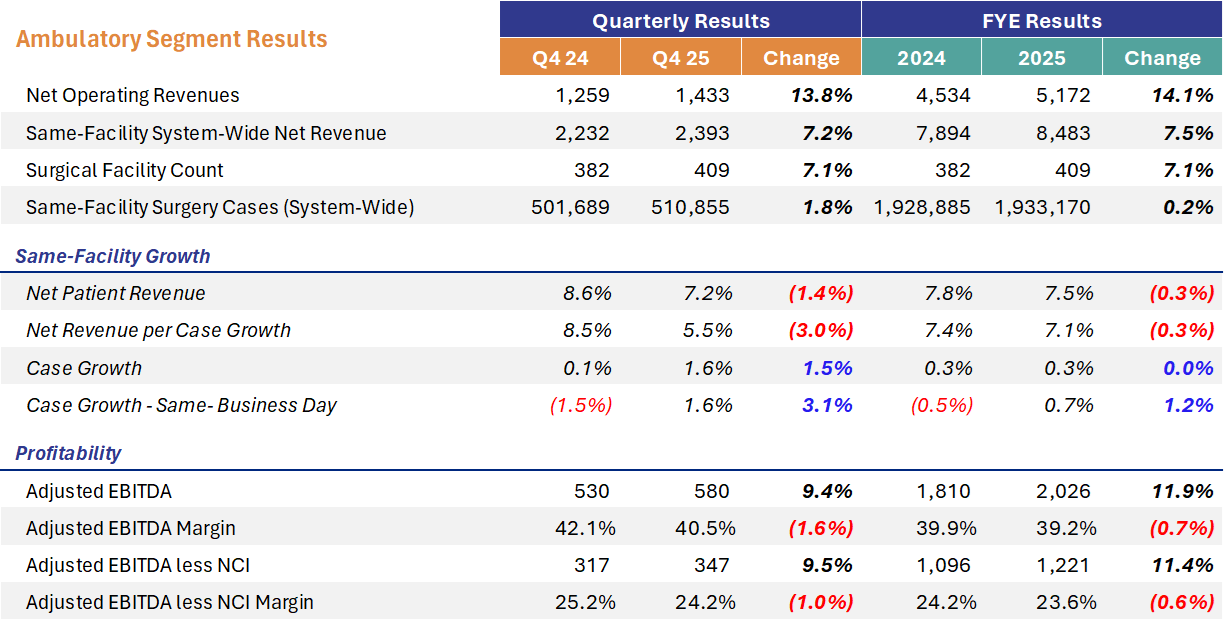

USPI continues to be the best story in ambulatory care. Here's the Q4 and FY 2025 rundown: |

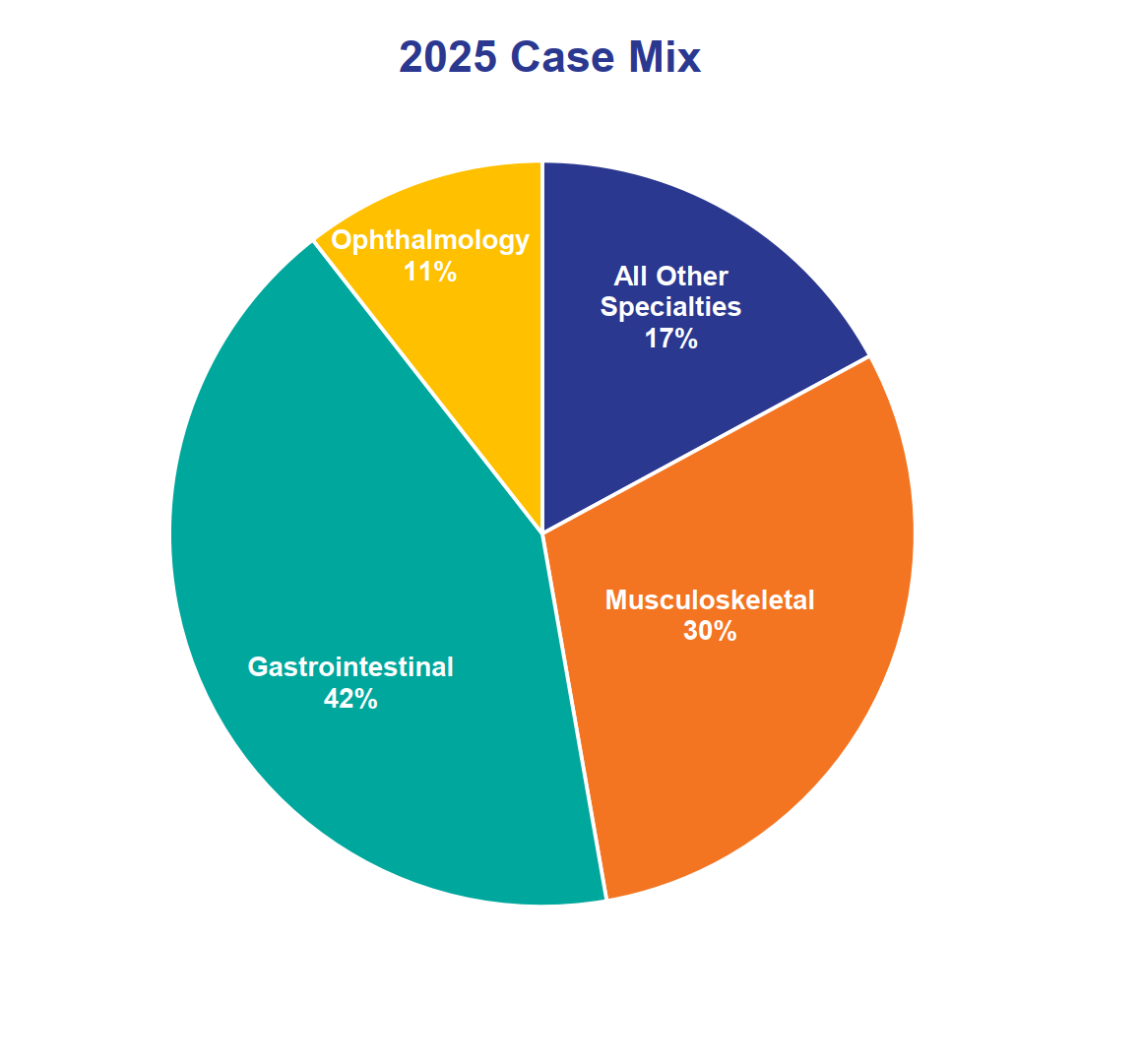

USPI's 2026 guide implies ~7.6% growth at the midpoint versus 2025 normalized performance, or ~9.1% when you add back the $30M exchange headwind. The deceleration from FY 2025's 11.9% growth is partially a comp issue (Q1 2025 benefited from Covenant and CPP acquisition synergies that won't repeat), and partially the more conservative 3-6% same-store revenue guide versus the 7.5% they actually delivered in 2025. Still, softening volume will remain a narrative and something I'm watching moving forward. The inpatient-only list phaseout is the emerging tailwind with significant runway. CMS is beginning to phase out the IPO list in 2026, which means certain procedures currently required to be performed in inpatient settings will become eligible for ASC reimbursement. Sutaria specifically called out high-acuity spine and urology as the first-year opportunity areas. He described this as a "gradual tailwind that will play out over several years." USPI is investing in robotics capabilities to capture these cases and has "detailed tactical plans" to operationalize for 2026. Case mix in 2025: GI at 42%, musculoskeletal at 30%, ophthalmology at 11%, all other specialties at 17%. Sutaria noted Q4 had a "nice pickup in GI case recovery," which was an important volume driver. USPI's patient experience score hit 96.7 in 2025. |

M&A returns profile: Tenet had some nice commentary on post-transaction multiples in the ASC space. Initial acquisition multiples of 8-10x compress to an effective 5-7x within ~3 years post-acquisition through service line diversification and acuity mix shift. De novo effective multiples come in below 2.0x. $250M annual M&A target, and the pipeline, as always, is 'robust.' |

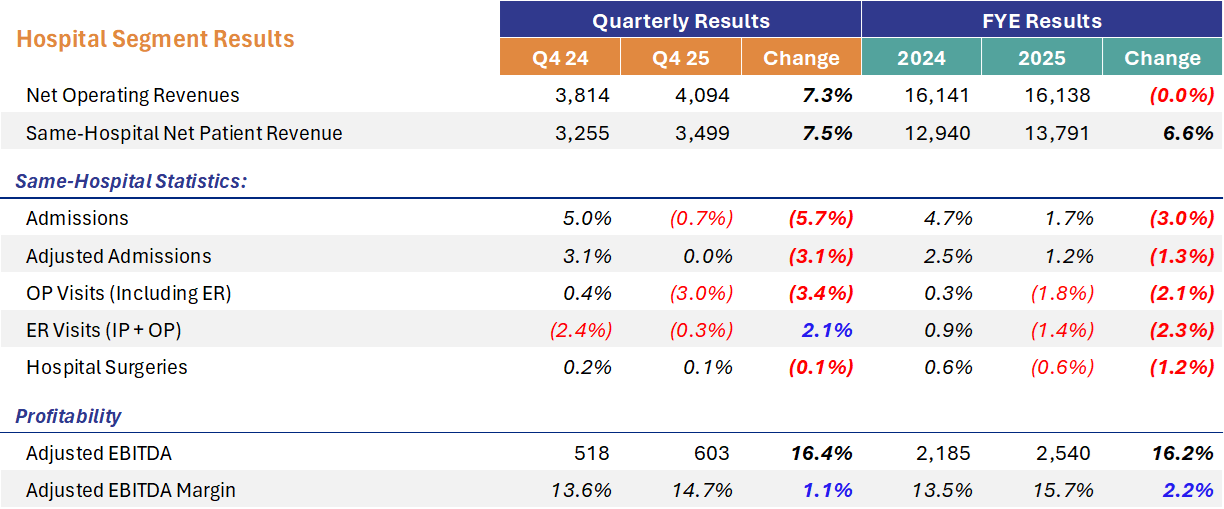

Hospital Segment: The Margin Expansion Story Meets Headwinds |

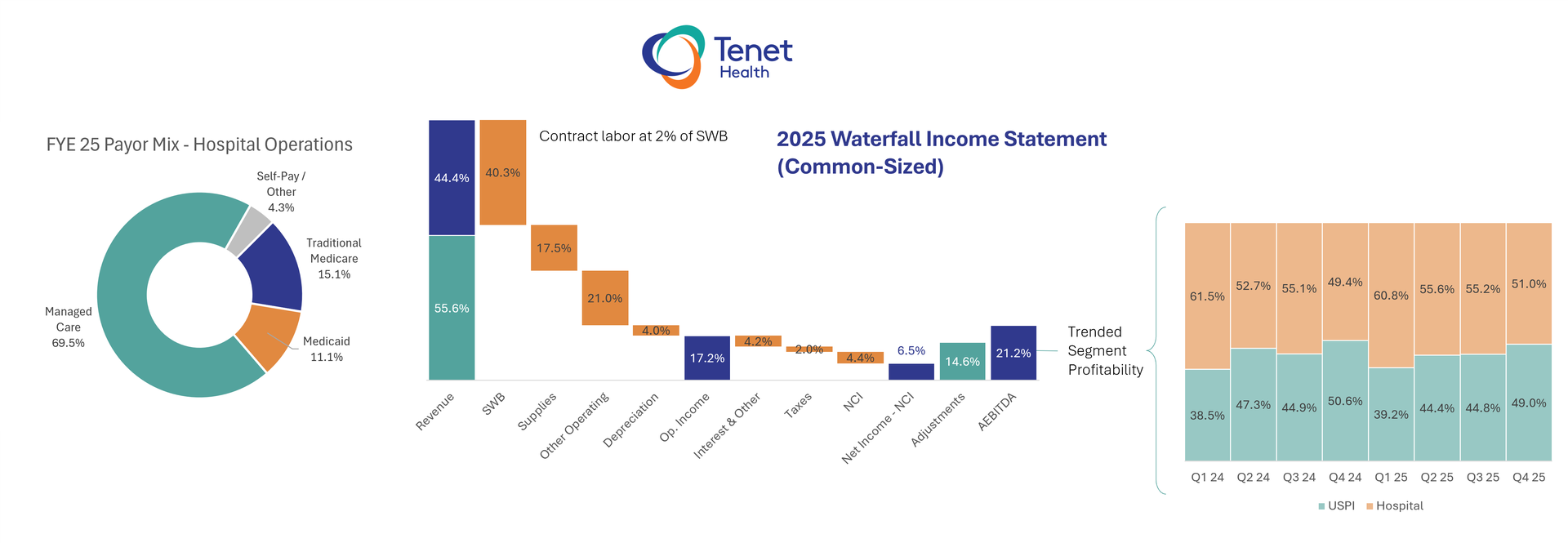

The $250M exchange headwind breakdown: $220M hospitals, $30M USPI. Management assumes 20% reduction in overall exchange enrollment, with significant exposure in Arizona, Michigan, and California. Only 10-15% of individuals losing enhanced subsidies are assumed to find alternative coverage (including employer commercial). For context, Sutaria noted UHS assumed 0% migration to employer commercial, while another peer assumed 15-20%. Tenet's 10-15% sits in the middle. Seems reasonable enough and a significant swing factor. The DPP/supplemental Medicaid picture: FY 2025 run-rate (excluding the $148M out-of-period) was ~$1.2B. 2026 guidance assumes a "pretty consistent number" with the 2025 normalized baseline. Importantly, no incremental contributions from pending supplemental Medicaid programs in states like Florida, Arizona, and California are included in the 2026 guide. Any approvals would represent pure upside. Good rate escalators: Rates in the 3-5% range from payors is consistent with a scaled hospital operator. Virtually all of 2026 is contracted (high 90s%), and ~80% of 2027 is already contracted. Interestingly Tenet isn't experiencing meaningful change in contracting dynamics. Tenet's value proposition to payors includes USPI as part of the overall package, which gives them negotiating leverage 'we are a lower cost option.' Volume Softness: You can see the deceleration in growth in FYE 2025 which Tenet shrugged off as a focus on acuity and a soft respiratory season. Despite the solid topline, similar to outpatient this trend is worth watching. |

Operating Leverage and the Structural Cost Play: AI, Automation, and the GBC |

There was some interesting commentary about technology deployment and AI, and continued expense leverage for Tenet. Here were some highlights noted below: 1. Technology deployment across the enterprise: - AI-driven denials management (improving speed and "veracity" of dispute resolution with payors)

- Automated coding (converting scribe-based notes into appropriate claims)

- Advanced analytics powering workflow automation (sorting millions of claims more efficiently)

- Robotic process automation across revenue cycle functions

2. Global Business Center expansion: - Tenet's offshore operation continues to scale and will expand further in 2026

- The combination of workflow automation + AI + offshore creates a compounding cost-to-collect reduction

3. Clinical throughput optimization: - Length of stay management using technology

- Throughput improvements in high-value hospital real estate (ORs, ERs)

- These create structural capacity improvements without incremental capital spend

Why is now the right time? Tenet spent years standardizing processes, workflows, labor standards, and supply standards across the organization. That standardization is the prerequisite for deploying technology at scale. "It's much harder to do those things when every market is doing something very different versus having established those standards." While Tenet didn't state a specific number or margin accretion from these efforts, they did bake it into the EBITDA bridge I pasted above. Slide 5 of the earnings presentation shows $427M of "Growth & Cost Efficiencies" at the consolidated midpoint. That $427M encompasses both revenue growth initiatives (capital investments, physician recruitment, service line expansion) and the cost efficiency programs. In general, I do think we start to see AI make a meaningful impact on margins in the near future, and this will start to differentiate forward-thinking organizations. |

Capital Allocation: Deploying Like a Higher-Multiple Company |

Tenet's balance sheet and cash generation are in the best shape they've been in, arguably ever, with historically low debt leverage and free cash flow. Mgmt was explicit about capital deployment philosophy: 2026 capital deployment priorities (in order): - USPI M&A (~$250M annual target) and de novos

- Hospital growth CapEx (technology, robotics, higher-acuity service line expansion)

- Share repurchases (balanced approach, but clearly a priority at current multiples)

- Debt retirement/refinancing as opportunities arise

| Capital Allocation: Deploying Like a Higher-Multiple Company |

The bear case is that Conifer is a wildcard, 10% core growth is a peak, that the exchange headwind could be worse than $250M, and that technology-driven cost savings are harder to realize than management implies. It is hard, given recency bias and the streak of success, and the industry talk around hospital headwinds, along with rising healthcare costs in general, that this growth trajectory is sustainable. Hospital volume comps also get harder. FY25 same-hospital admissions grew 1.7%, but that was against a strong '24 (+4.7%). Outpatient visits have been declining (down 1.8% same-hospital in FY25), and ER visits were down 1.4%. Those trends suggest some structural volume pressure beneath the acuity story.

The bull case is that USPI is a secular growth story with multiple years of IPO list tailwinds ahead, that the hospital segment has real margin expansion runway with technology deployment / efficiency gains, and that Tenet's capital return program is meaningfully accretive at current multiples. Plus, capital invested in Capex at hospitals and the large M&A cohort at USPI will pay dividends in volume growth and more in 2026 and beyond. |

The Macro Backdrop: Implications for Healthcare |

Tenet's Q4 and 2026 setup is a microcosm of the forces reshaping the hospital and health system landscape: 1. The ACA subsidy cliff is the 2026 story for hospitals. Whether you're THC, UHS, HCA, or a not-for-profit system, the expiration of enhanced premium tax credits is the single largest identifiable headwind this year, with wide potential variance in outcomes. Tenet's 20% enrollment reduction / 10-15% alternative coverage assumption gives you one framework, but the actual impact depends heavily on geography, state Medicaid programs, and how aggressively systems use revenue cycle tools to get patients enrolled in alternative coverage. 2. Supplemental Medicaid remains a wild card. $1.2B normalized for Tenet alone, with pending programs in FL, AZ, and CA not yet baked in. Across the industry, DPP and supplemental Medicaid programs have become a massive revenue lever - and perhaps one that will be getting oversight in the future. The political durability of these programs, especially in a DOGE-driven federal cost reduction environment, is something every system should be wary of. 3. The shift to ASCs is accelerating. The IPO list phaseout beginning in 2026 is a structural, multi-year catalyst. Tenet/USPI is positioned as the leading platform to capture it given their scale (559 facilities), robotics investment, and physician partnership model. Not-for-profit systems that haven't invested in ambulatory strategy are falling further behind. If you've read Hospitalogy recently you guys know I've been hammering it into the back of your skull. 4. Revenue cycle is becoming an AI arms race. Tenet's Conifer strategy, fully owned, with AI/automation/offshore investment, is a call option in a red hot space chock full of AI use cases and automation, with lots of buyers and a consolidating M&A environment. But the flip side is the payor pushback narrative. Tenet comments about denials management friction and the need for adjudication mechanisms reflect the escalating arms race between provider revenue cycle operations and payor utilization management. Both sides are deploying technology. The tension isn't going away. 5. Cost structure transformation is the new imperative. Tenet's "structural" cost management language signals a recognition that traditional cost cutting won't be enough to sustain margins against potential future reimbursement pressure (OBBB, site-neutral, etc.). The Manila GBC expansion, AI-driven workflow optimization, and clinical throughput improvements are all part of a playbook that larger, more sophisticated systems will need to adopt. |

Hospital Segment: The Margin Expansion Story Meets Headwinds |

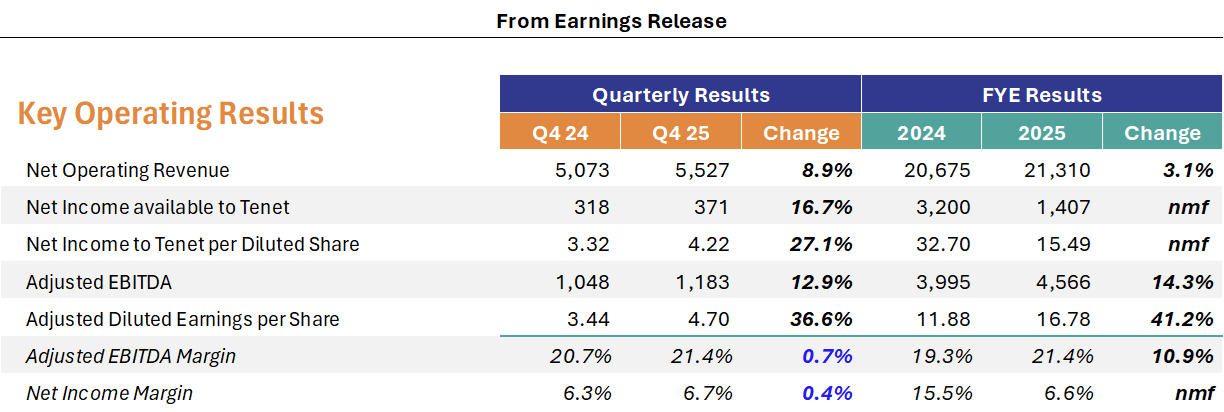

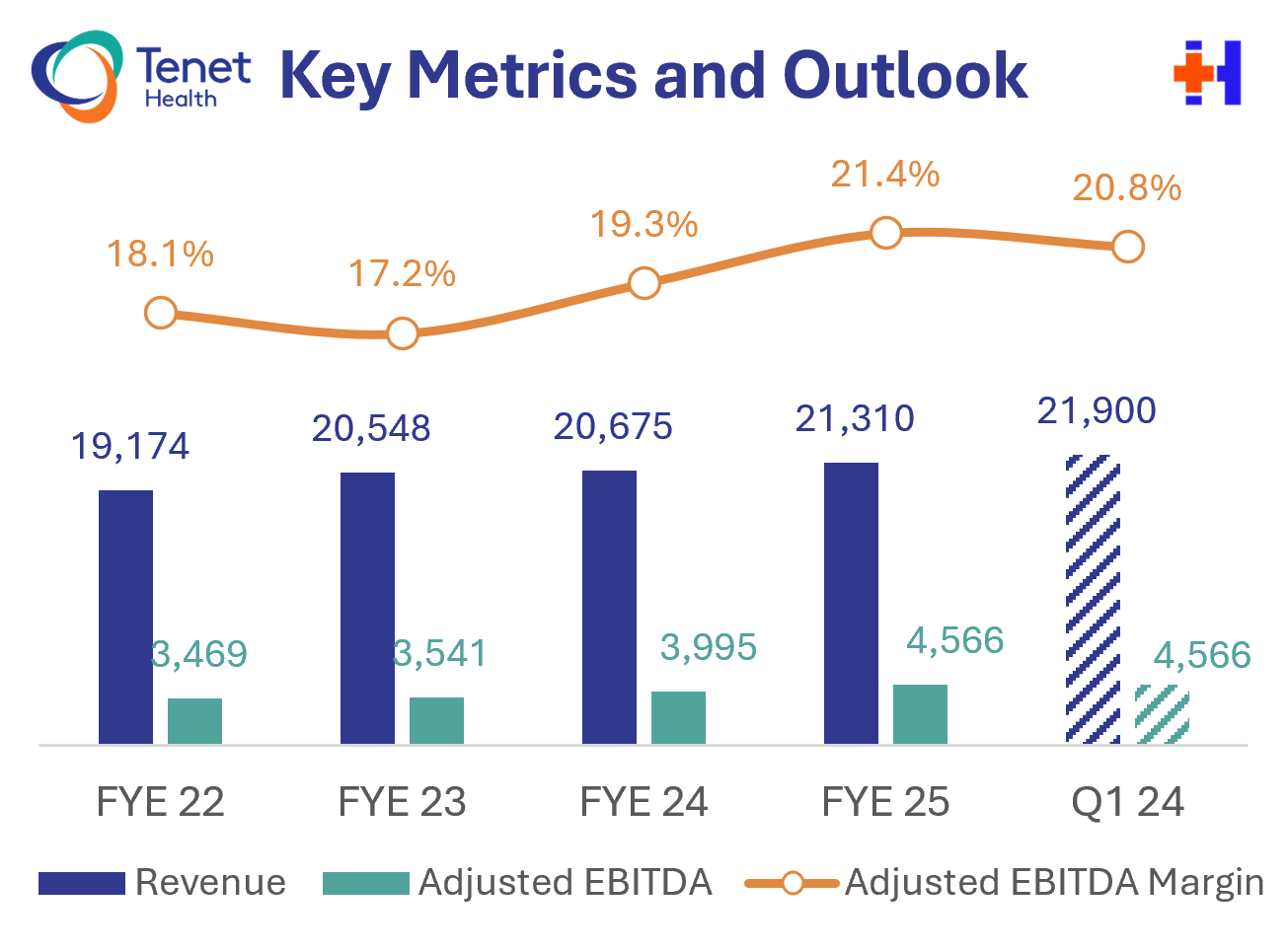

Tenet just put up 14% EBITDA growth in 2025, guided to ~10% core growth in 2026 despite a $250M exchange headwind, unlocked ~$1.1B of incremental value from the Conifer deal, and has nearly $2.9B of cash on a balance sheet leveraged at just 2.25x. Hella impressive.

This is not the Tenet of five years ago. That aircraft has been completely rebuilt, and both engines are running full throttle. | |

|

SPONSORED BY WEAVER Outpatient imaging demand is accelerating, but not evenly. Routine modalities like X-rays and ultrasounds are projected to increase in line with population trends. But PET, CT, and MRI volumes are expected to surge beyond population growth, driven by earlier detection and care complexity. These diverging trends carry important implications for valuation and capital planning, as some modalities are becoming strategic assets and others are turning into margin traps. Analysis from national accounting and consulting firm Weaver breaks down how shifts in imaging utilization are reshaping capital decisions, competitive positioning, and deal economics.

|

|

|

Is it just me or have Super Bowl commercials become way less...funny and edgy? What happened to the Bud Knight? Dilly Dilly? The kid in the darth vader costume lifting up the tailgate with the force? There were some...alright ones this year but none that stuck with me. What a sad state of affairs. And the game was arguably worse. Congrats to Sam Darnold though. That takes serious self confidence to persevere through 5 teams, then to win a Super Bowl. Are we in a creative recession?! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 66,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments