Hospitalogists,

As is customary fashion today we're diving into key themes and outlook from public for-profit hospital operators to start 2026.

TL;DR - every management team is navigating the same macro headwinds - ACA subsidy expiration, Medicaid uncertainty, professional fee inflation, the OBBA - but the strategies, financial positions, and operational playbooks vary.

Hopefully you find this valuable!

Let's get into it. |

Was this email forwarded to you? |

|

|

BLAKE'S BREAKDOWN: 2026 Outlook and Key Hospital Themes |

Going deeper on an interesting topic, theme, or trend |

Readying the Warships: The Calm before the Storm |

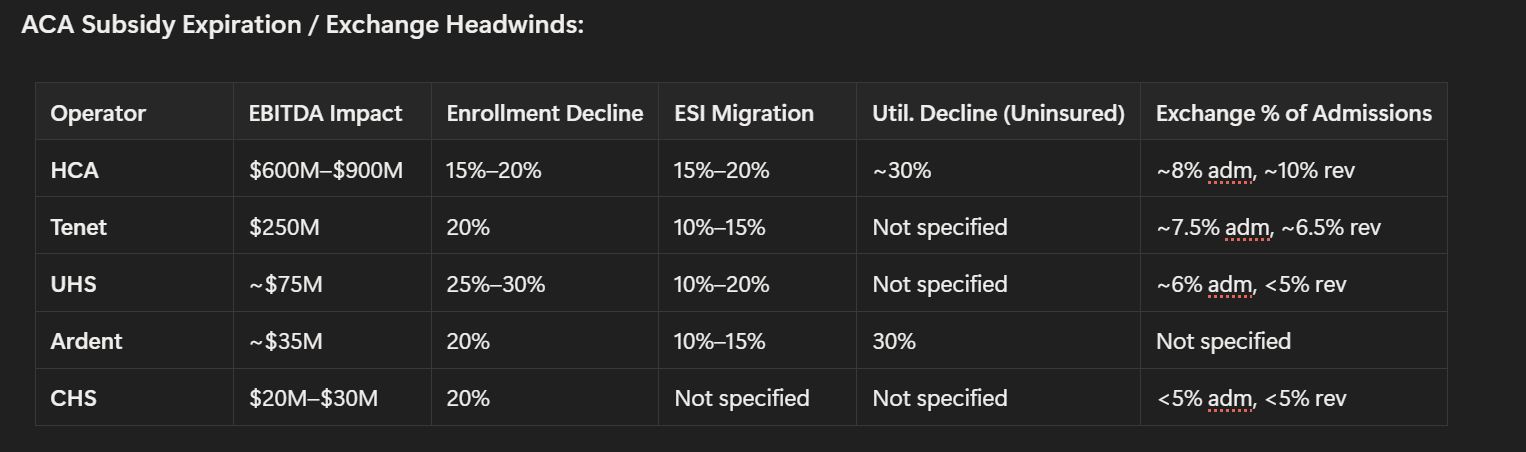

Executive Summary - Everyone bracing for ACA impact, and we finally get some numbers: HCA sized the exchange headwind at $600M–$900M to EBITDA while CHS estimated just $20M–$30M. Common assumptions include enrollment declines of 15% - 30%, conversion rates to commercial insurance of ~10% to 20%, and volume declines of ~30% for newly uninsured.

- Readying the warships before upcoming cuts: The public operators are bolstering up their margin defense (cost reductions, centralized planning) ahead of looming cuts in the years to come, and the ones with standardized tech stacks (Ardent's single-instance Epic, HCA's data platform) hold a structural advantage.

- Professional fees are the cost line nobody has answers for. Every operator flagged at minimum high-single-digit growth in physician costs, driven by radiology and anesthesia shortages (particularly affecting CHS and Ardent), and nobody is projecting meaningful improvement in 2026…this is the one expense category (AKA, highly skilled labor in shortages) where AI or technology hasn't penetrated.

- Labor Market Bottom. Ardent hit 2.6% of SWB (lowest since 2019), Tenet clocked 2.1%, HCA settled at 4.2%, and UHS at 2.4%. Rounding errors.

- The M&A and capital deployment picture is bifurcating hard. HCA has $7B in approved capital projects and just authorized $10B in buybacks. Meanwhile CHS is still selling hospitals to de-lever. Competitive moats among are widening among the have's and have not's across the health system landscape, as has been the case for some time.

Market Snapshot: |

Thematic Cross-Operator Analysis |

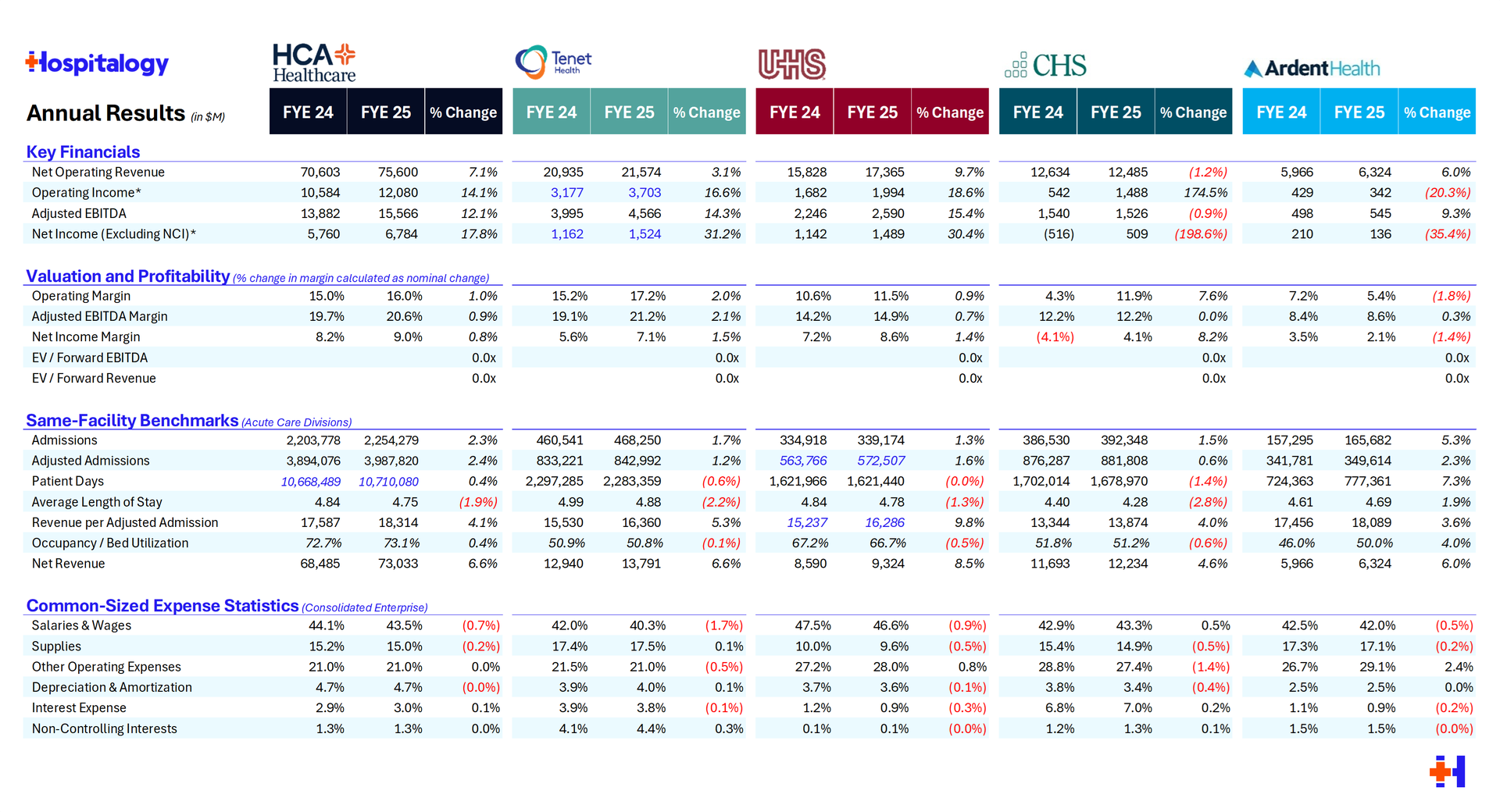

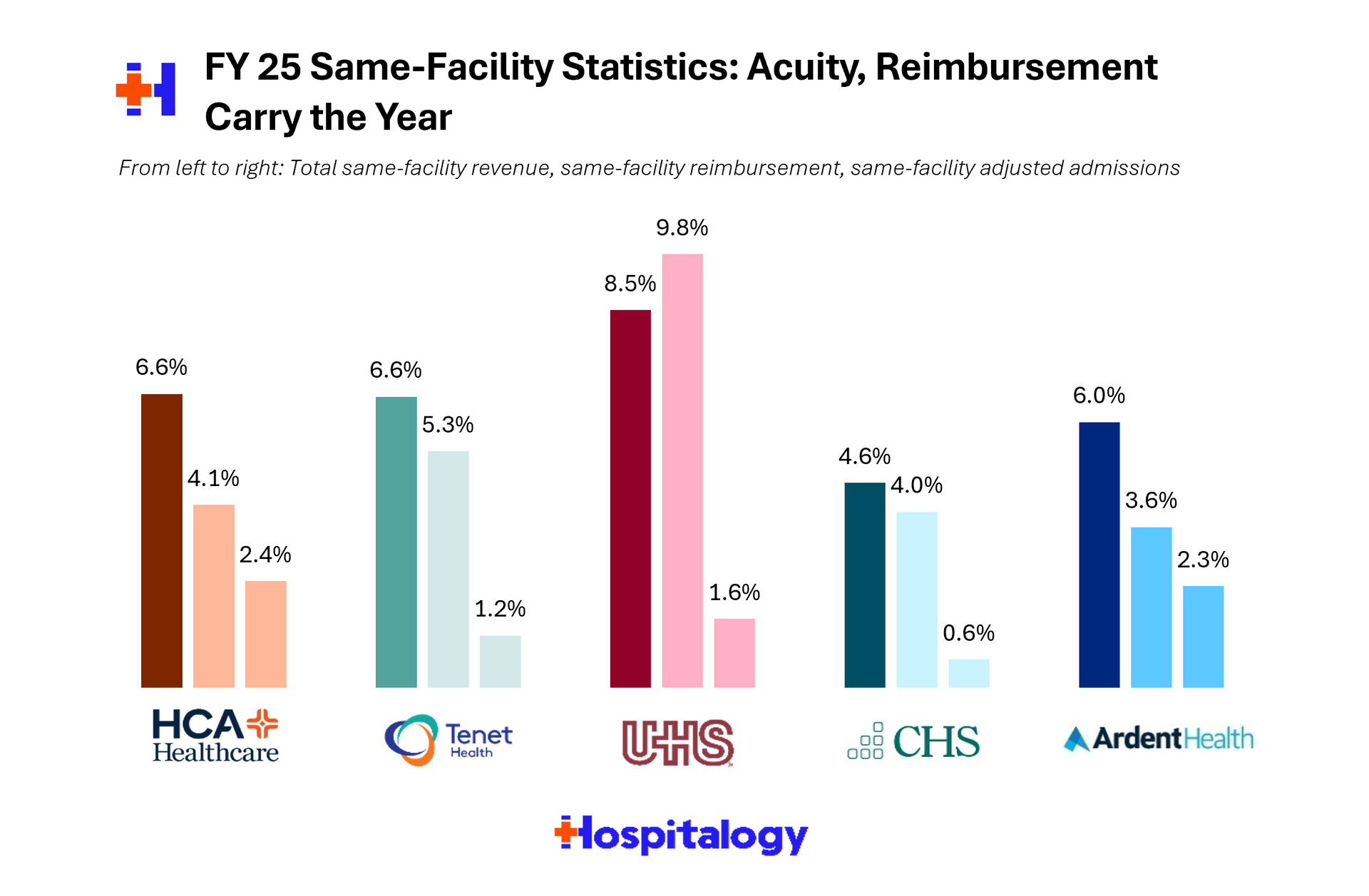

Volume Trends: 2 - 3% Consensus, with Caveats Every operator except CHS is expecting 2-3% adjusted admission growth this year. HCA came in at 2.5% adj admission growth in Q4 2025, Tenet's hospital admissions were flat but adjusted admissions up 2%, UHS acute care was flat to +1% (excluding Las Vegas), Ardent grew admissions 5.3% and adjusted admissions 2.3% for full-year 2025, and CHS was slightly negative on a same-store basis. Volumes are bifurcating as ambulatory expansion and health system transformation continues to shift outpatient. Everyone is discussing OP access point expansion including urgent cares, freestanding EDs, ASCs, physician clinics (and micro hospitals, etc.) as the primary growth vector. HCA now has ~2,700 outpatient facilities and is targeting 18 - 20 per hospital if you recall from my HCA Q4 writeup. Tenet added 30+ USPI facilities in 2025. UHS opened double digit Thousand Branches outpatient behavioral locations. And Ardent is opening new urgent cares, hospital-based ASCs (HOPDs? In this economy?), and a freestanding ED in Texas. Specific service lines receiving attention included the usual suspects. Cardiac/EP at HCA, total joint replacements at USPI (double-digit same-store volume growth), women's services at CHS, heart surgery at CHS Longview (up 16%). Reimbursement: Rate Tailwinds Holding, Acuity Driving Revenue Per Unit Rate increases continue to carry the day. Acuity, coding, reimbursement from inflation, however you characterize it, it's up and to the right. The middle number in the chart below corresponds to same-store revenue per adjusted admission growth for 2025 over 2024. Pretty strong across the board: |

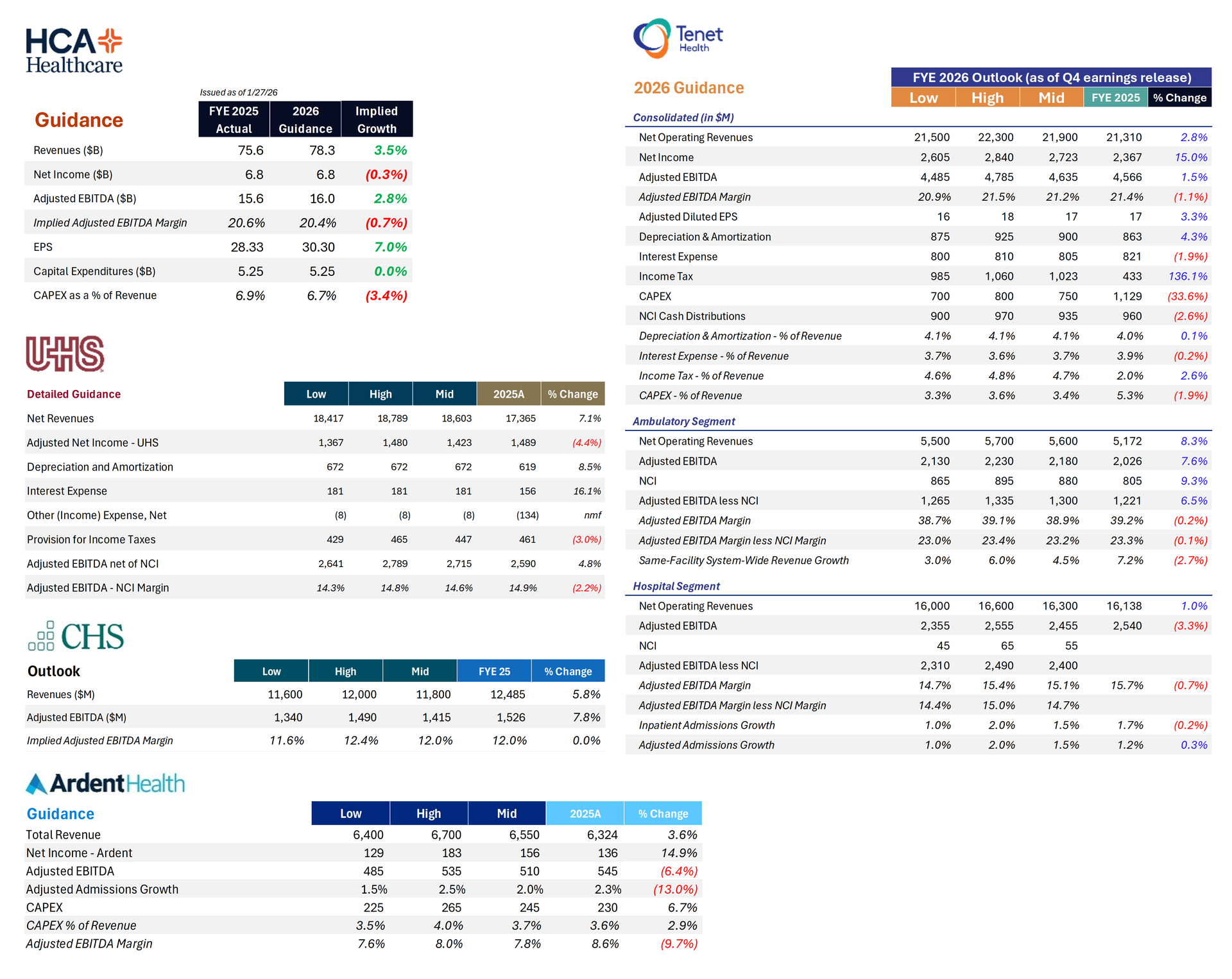

- HCA: Net revenue per equivalent admission +2.9% in Q4; expecting similar trajectory in 2026

- Tenet: Revenue per adjusted admission +5.3% full year at hospitals; USPI net revenue per case +5.5% in Q4; commercial rates 3%–5%

- UHS: Acute care pricing guided to 3%–4% in 2026 (in line with 10-year average); behavioral pricing guided to 2%–3% (moderating)

- Ardent: Net revenue per adjusted admission trending positively; commercial contracts yielding 4%–5% rate increases with ~90% contracted for 2026

- CHS: Net revenue per adjusted admission +2.4% in Q4; core rate assumption of 2.5%–3.5% growth; Medicare inpatient rate of ~4% in 2026 (highest in memory per Hammons)

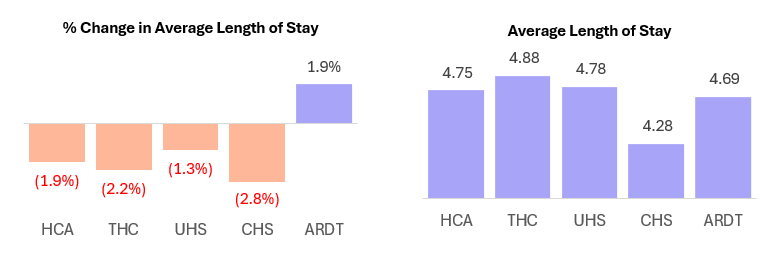

Acuity is a universal tailwind. Case mix index continues to rise across peers, driven by sicker patient populations and deliberate strategic focus on higher-acuity service lines. HCA, Tenet, and Ardent all cited growing acuity as a key revenue driver. UHS noted acuity-adjusted LOS is actually below pre-pandemic levels. CHS highlighted inbound transfers for higher-acuity care as a growth vector. |

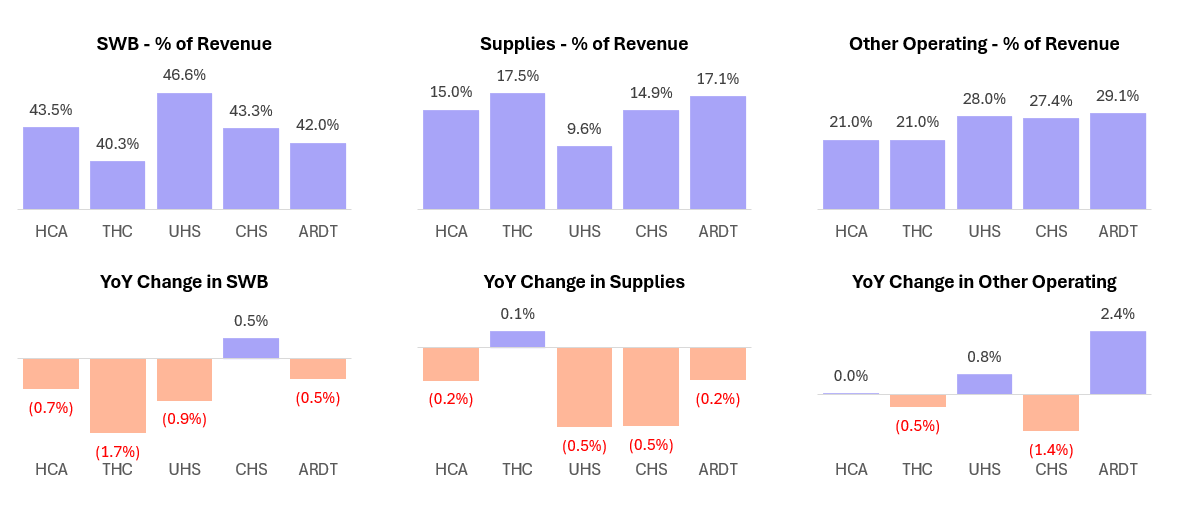

Cost Pressures and Operating Leverage Where hospitals are winning: Contract labor is at or near post-pandemic lows across the board. Supply chain management is well controlled. SWB as a percentage of revenue is declining at most operators. These are the categories where standardization, scale, and technology investments are delivering clear operating leverage. |

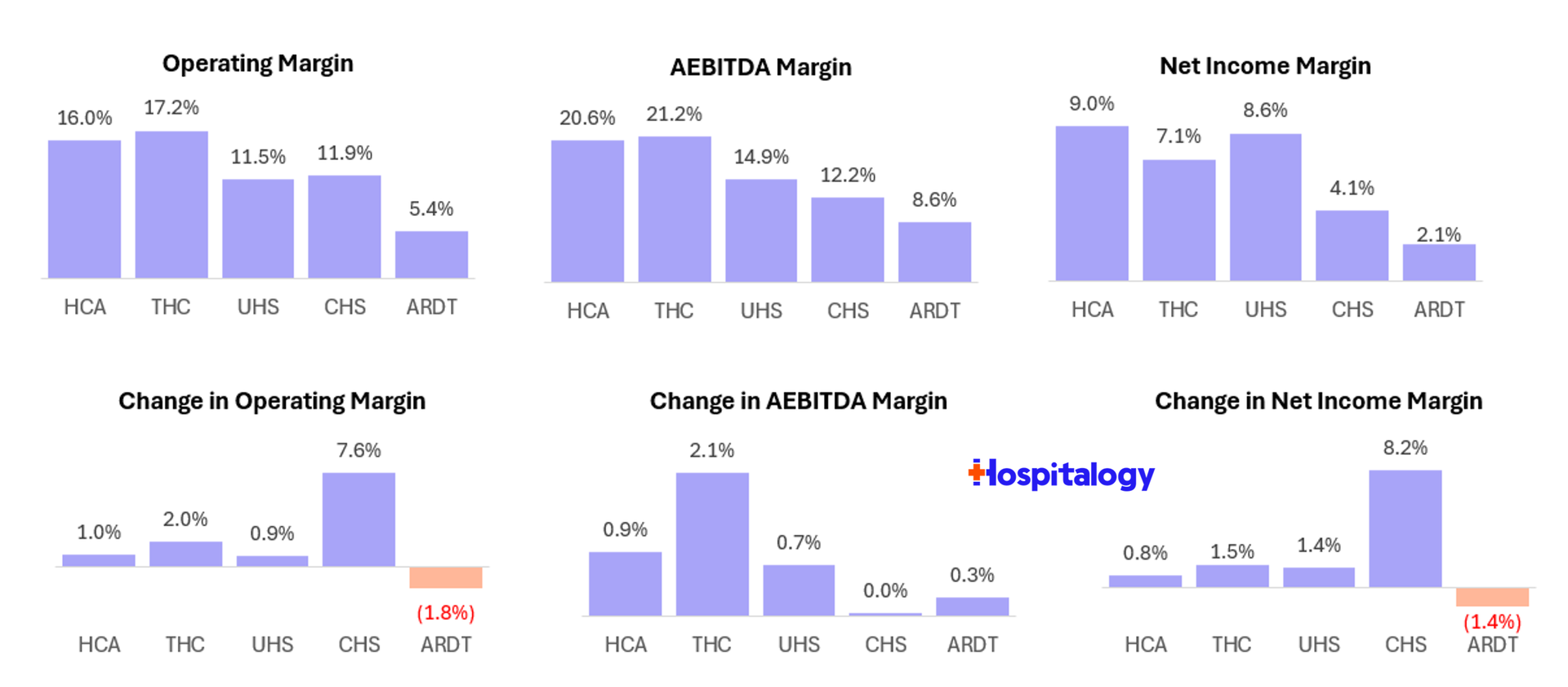

Where hospitals are losing: Professional fees and medical specialist costs are the universal pressure point, with every operator flagging high-single-digit growth driven by radiology and anesthesia shortages. CHS specifically guided to 5%–8% growth. Nobody projects improvement here. The structural issue is physician scarcity in procedural specialties, and the only mitigation strategies mentioned were insourcing (CHS) and strategic recontracting (Ardent). Margin trajectories: - HCA: Guiding to margins slightly above 20%, consistent with 2025, despite exchange headwinds—a testament to the $400M resiliency program

- Tenet: 21.4% margins in 2025 (+210bps YoY); normalized core EBITDA growth of ~10%

- UHS: Acute margins expanded 150bps to 15.8%; behavioral margins stable despite staffing investment

- Ardent: 8.6% EBITDA margins (+20bps); significant room for expansion as IMPACT program ramps

- CHS: 12.7% Q4 EBITDA margin; sequential improvement, but still lowest in the group

|

M&A, Capital Deployment, and Growth Capital allocation landscape is as bifurcated as I've ever seen it: - HCA is in full offense mode: $10B new share repurchase authorization, $5B–$5.5B in CapEx, $7B in approved capital projects, 73%–74% occupancy creating organic expansion opportunities. Seeing a stronger outpatient acquisition pipeline than in recent years. No compelling hospital M&A yet.

- Tenet is deploying aggressively at USPI ($250M annual M&A target, 35 facilities added in 2025) while buying back 22% of its float since 2022. USPI remains the "preferred acquirer and developer" of ASC assets. Hospital-side capital is focused on growth CapEx in high-acuity capabilities.

- UHS is maintaining maximum balance sheet flexibility (leverage at the low end of 2–3x target) with active share repurchases ($899M in 2025). De novo pipeline includes two behavioral hospitals (264 beds) and the new Palm Beach Gardens acute care hospital. Outpatient behavioral expansion through the Thousand Branches brand.

- Ardent is focused on disciplined capital deployment in core markets—urgent cares, hospital-based ASCs, freestanding EDs, OR optimization. Balance sheet has improved to 2.5x leverage with $710M in cash. Not an active M&A story at this stage, but well-positioned financially.

- CHS is still in divestiture mode (Huntsville closing Q2 2026), but shifting toward reinvestment. Added 500–600 beds to core hospitals over the past 3–4 years despite selling 35% of the portfolio. Pipeline for further divestitures is "dwindling" per Hammons.

Technology and AI: Where the Rubber Meets the Road The AI commentary across the five calls ran the full spectrum from visionary to practical. Here's what stood out: - Ardent. AI scribe at 85% adoption, 35% documentation time reduction. Medical wearables reducing mortality by 15% and LOS by ~0.3 days. Virtual care expansion to 2,000+ rooms. The single-instance Epic platform is the enabler and I can remember this being called out as a strategic advantage to the org in its S-1.

- Most ambitious strategic vision: HCA. Three-domain framework (administrative, operational, clinical). The "holy grail" of clinical AI using HCA's proprietary database for pattern recognition to support physician decision-making. EHR transition to standardize datasets. $400M resiliency program leveraging digital transformation.

- Most practical near-term deployment: UHS. Hippocratic AI partnership for agentic AI in post-discharge care. Revenue cycle AI for claims appeals. Behavioral health intake/referral AI. Patient safety technology for behavioral settings. Filton acknowledged difficulty in precise quantification but cited reduced headcount and improved readmissions.

- Most transformative (maybe?) infrastructure play: CHS. Oracle ERP generating ~$50M in savings in Year 1. Single item master across the enterprise. Quarterly AI functionality updates from Oracle cloud. AI in claims appeals, autonomous coding, prior authorization. Also deploying AI-augmented virtual patient sitters and ambient listening.

- Most "structural" framing: Tenet. Sutaria described technology-enabled expense management through global business centers and clinical throughput optimization. Emphasized this is "modernization" not traditional cost-cutting. Separately, digital integration with payers for electronic data exchange and administrative simplification is driving working capital improvements.

|

Policy & Regulation ACA Subsidy Expiration / Exchange Headwinds: |

Medicaid / Supplemental Payments: HCA expects $250M–$450M decline in net benefit (Texas ATLAS pause, Virginia retro, Tennessee timing). Tenet reported $1.34B in 2025 supplemental payments and expects roughly flat normalized levels. UHS expects $1.36B in supplemental benefit (+$23M YoY), with Florida ($45M–$50M) pending. CHS excluded unapproved programs. Ardent excluded the Rural Health Fund from guidance. Rural Health Transformation Fund (OBBA): HCA: ~15% of hospitals qualify; rural/rural referral center designations; active engagement with states. Ardent: up to one-third of hospitals could qualify; Texas and Oklahoma received largest allocations. UHS: small percentage of facilities carry designations; not expecting material benefit. CHS: states still finalizing program design; not included in guidance. OBBA Medicaid Cuts (2027–2028 horizon): Every operator is positioning for this. HCA's $400M resiliency program is explicitly framed as multi-year. Tenet's "structural" expense management is about being "well prepared." UHS's outpatient behavioral expansion naturally hedges against Medicaid DPP reductions starting in 2028. Ardent's IMPACT program is described as "multiyear and durable." CHS's ERP and AI investments are building infrastructure. Professional Fee Inflation: Universal pressure, universally acknowledged, universally unsolved. High single digits across the group, driven by radiology and anesthesia shortages. |

Key tailwinds across the group: Continued volume growth in fast-growing markets, commercial rate increases of 3%–5%, acuity growth driving revenue per unit, contract labor normalization, technology/AI-driven efficiency gains, IMPACT/resiliency programs, potential Rural Health Fund upside. Key headwinds: ACA subsidy expiration (the elephant), professional fee inflation, supplemental payment timing and declines, OBBA Medicaid cuts on the horizon, consumer confidence and economic uncertainty, weather disruptions (Winter Storm Burn impacted Ardent's Texas/Oklahoma markets; HCA's Nashville area). Verdict In 2026, the warships are readying for murky, treacherous waters ahead and we're seeing leading health systems preparing for looming cuts ahead. While we got some answers on certain fronts (ACA cuts, supplemental payments) there is more bad than good that can happen in 2026. |

|

|

SPONSORED BY URSA HEALTH What's powering Cityblock Health's quality engine? The Ursa Core Data Model.

To build a smarter, more adaptive quality engine to support complex Medicare and Medicaid populations, this VBC organization turned to Ursa Health to enable: Integrated, unified claims, EMR, clinical data feeds, and payor gaps-in-care reports Flexible, configurable HEDIS, PQA, and Medicare Stars measure logic Custom engineered nightly data refreshes that feed downstream point-of-care workflows An extensible data foundation to power future AI enhancements and continuous innovation See how this improved accuracy and accelerated time to insight across populations and programs.

|

|

|

Tonight, the nay-nay (pacifier) fairy comes to whisk away all of my toddler's pacifiers, never to be seen again, in exchange for some wonderful toys (excavators, dinosaurs, et al) wish us luck putting him to sleep tonight. Godspeed! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 66,600+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments