🏥 Atrium-WakeMed Commentary

|

||||||||

|

||||||||

|

|

||||||||

Welcome to Thursday, Hospitalogists! Atrium has been in the North Carolina news quite a bit over the past week given its impending bid for WakeMed, so we’re doing a quick dive into that announcement and what I find notable. Next week will be a dive into Advocate’s financials followed by a hospital Q1 overview on Thursday! Was this email forwarded to you? Sponsored by Ursa Health Not all population health opportunities are created equally. Not all AI analyses stand up to clinical and analytical scrutiny. And the difference between signal and noise can have real downstream financial and clinical consequences. Atrium-WakeMed: Merger AnalysisFirst, a bit on the proposed combination between WakeMed and Atrium (Advocate). From what I’ve gathered, the deal has been under talks for several years (just rushed to the finish line). Competitively, WakeMed is the #3 player in its broader area, which means they’ve largely been the managed care punching bag and getting competitively squeezed by Duke and UNC Health (and part of what makes UNC's competitive position so formidable is structural: it is the only public medical school in the state, giving it unique protections and institutional incentives that no private competitor can easily replicate). Complicating matters further is the infamous inter-county rivalry within the Triangle. Wake County (Raleigh), Durham County (Durham), and Orange County (Chapel Hill) have a long history of animosity toward one another and rarely cooperate. Wake County's primary political instinct is self-preservation - keeping Duke and UNC from encroaching on its territory - which shapes every aspect of how the WakeMed deal must be structured and communicated. The press release between the two caught my attention on a few different fronts discussing the positive effects of the merger. Simply put, WakeMed has an infrastructure crisis. It needs capital, and it doesn’t have capital to invest in needed changes to its facilities. So Advocate/Atrium is shoring up WakeMed with $2B in the coffers to invest in upgrades, new capabilities and transformative assets to meet the demands of population growth in its operating footprint. Within the announcement WakeMed also discussed expansion of virtual care capabilities and specialist access - creating North Carolina’s ‘largest virtual care network’ and creating more convenience access for specialty care closer to home, expanding financial assistance including more mental health and residency slots - all initiatives the state can get behind. Whether the deal goes through or not at the state, the points emphasized are pretty compelling, but some sort of oversight and reporting will likely be included with any approval.

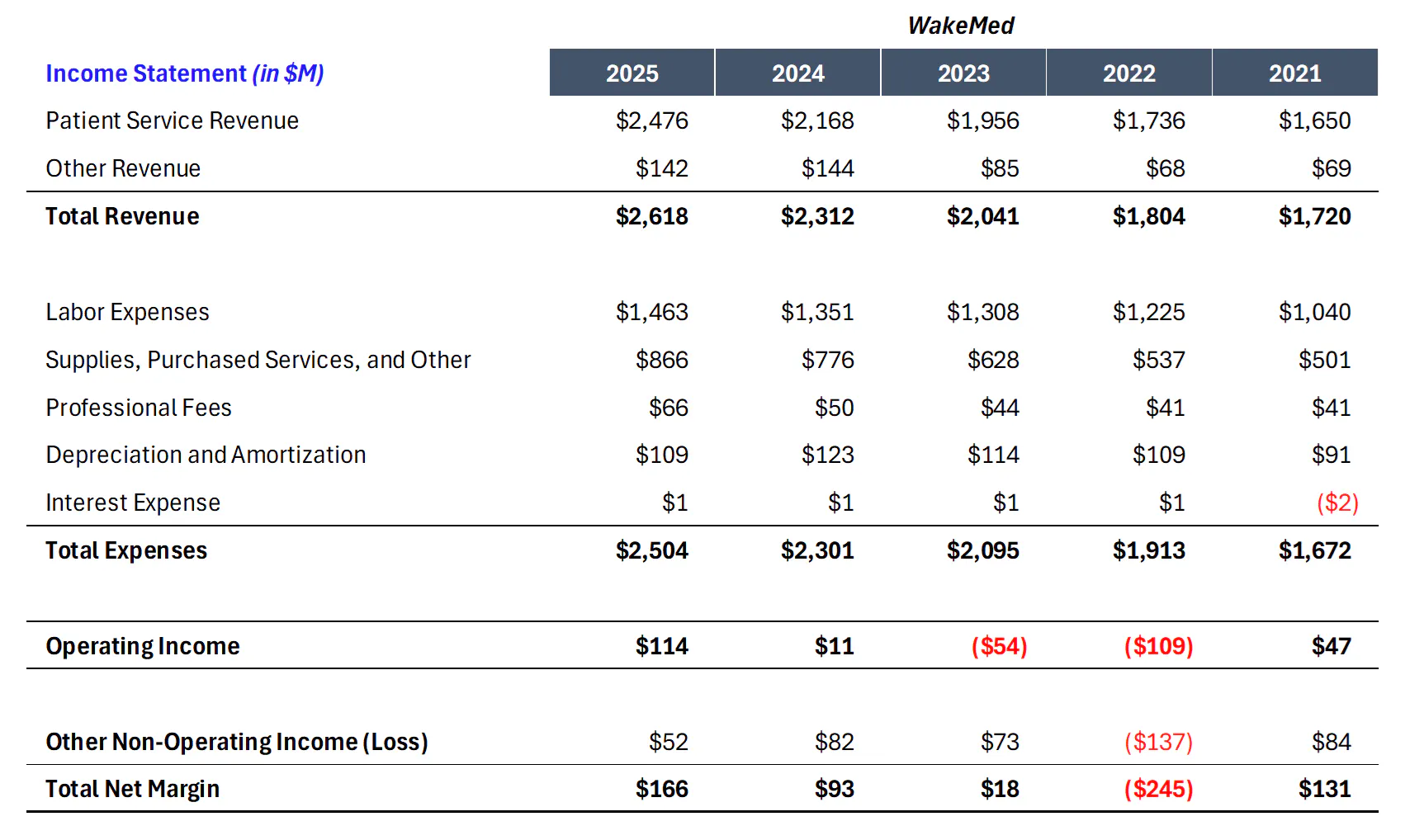

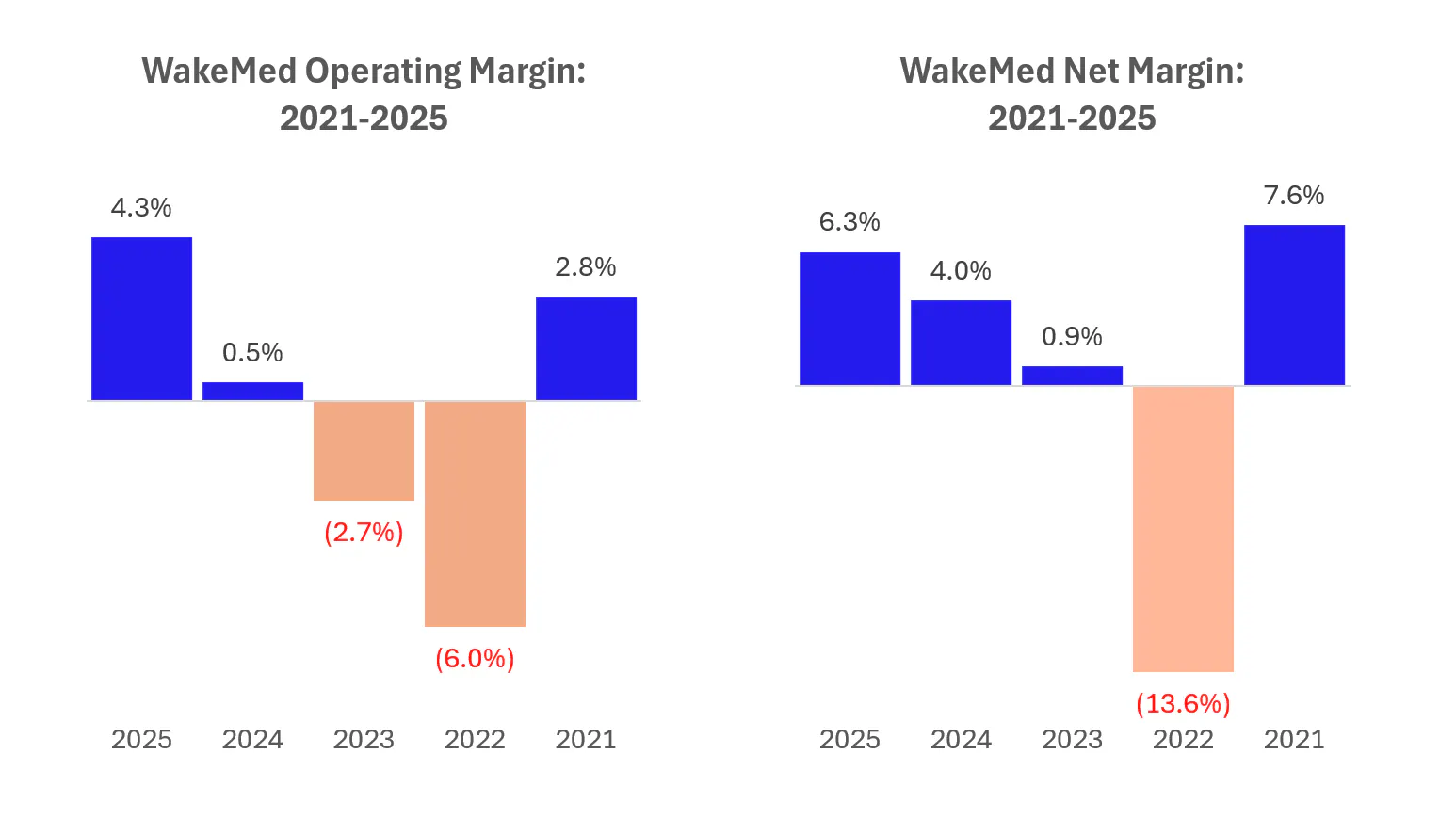

From a financial position, WakeMed is in a bit more of a stable position compared to 2024, rebounding from breakeven operating margin. The system as a whole operates 3 acute care hospitals (with its flagship in Raleigh) aligned with 542 physicians, nearly 13k employees, and $2.6B in revenue as of its fiscal year ended September 30, 2025.

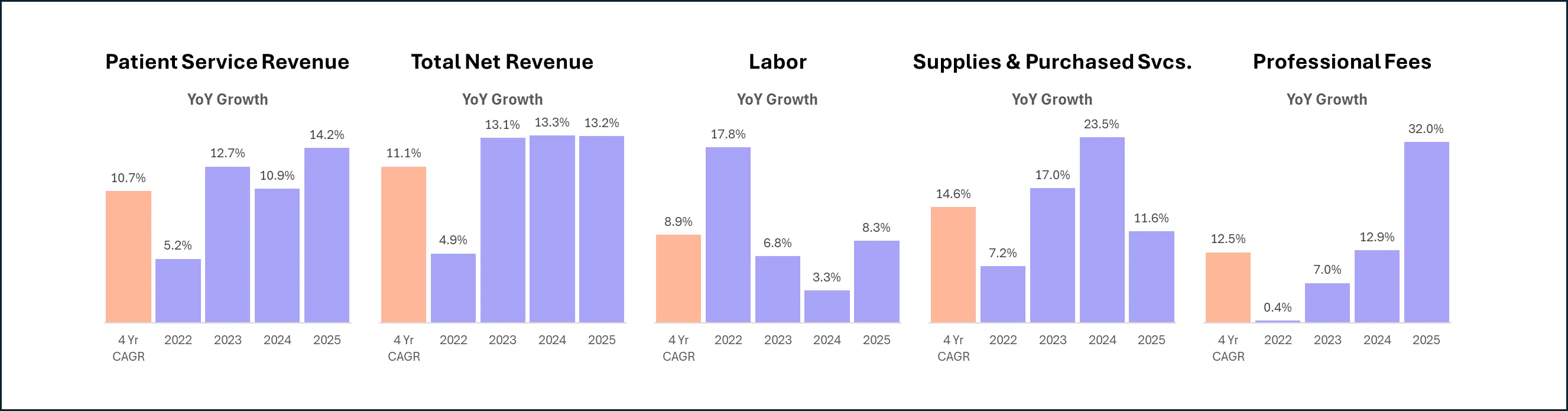

Over the past several years, WakeMed has fluctuated between relatively healthy operating margins and pretty poor performance in 2022 and 2023:

What’s interesting about WakeMed given all of this context is a somewhat contrarian truth: a hospital can possess a large geographic footprint, operate in a demographically attractive and growing market, and still function at sub-scale. This dynamic is precisely what has happened to WakeMed, and the suboptimal performance illustrates how the relentless competitive encroachment of academic medical centers gradually strips standalone systems of the high-acuity volume they need to remain financially viable. As lower-acuity procedures migrate out of the hospital setting entirely, these systems are left without the high-acuity backstop that once cross-subsidized community care. Those who are discussing this merger or lumping it in with other antitrust cases (Mission Health) not framing this correctly. In many of those instances, the state or community was selling a monopoly with 10%+ EBITDA margins to a private institution in exchange for capital or other commitments. Though antitrust considerations will of course be brought into question given Atrium-WakeMed combined, the facts and circumstances are materially different in a competitive metro market. Atrium Health is hoping to unlock WakeMed’s full potential, to compete on the same level as its fellow academics, and they have the balance sheet to do so. MISCELLANEOUS MADDENINGS Happy Mothers Day to all the mothers reading this! I hope you are remembered and celebrated this weekend. I see firsthand the sacrifices and energy given to raising little ones day in and day out. Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

||||||||

|

No comments