Over 150 providers have already been approved to participate in ACCESS, the Medicare experiment that will test out paying health tech companies to take care of enrollees with chronic conditions like diabetes, hypertension, and chronic muscle pain. Notably absent from the list of participants published last month were Hinge Health, Omada Health, and Teladoc Health, prominent digital health players that collectively care for over 3 million people with chronic conditions.

Hinge and Omada offfer virtual musculoskeletal care and Omada and Teladoc have programs for diabetes, hypertension, and weight loss. All primarily sell to employers and commercial health plans but have designs on Medicare.

Hinge CEO Daniel Perez told me that "diplomatically" he applauded CMS' willingness to innovate on payment models. But he didn't mince words on his assessment of the current ACCESS model:

"It will not improve outcomes, it will not improve the experience, and it will most certainly not reduce costs. And the way it's been structured, digital health companies have to basically remove any sort of clinical human oversight. And we are not talking about an employer population. We're talking about a Medicare population that is a full generation older than [the] employer population, one of the highest risk patient populations in all of America. And it's been structured in an intentional way to remove any sort of clinicians in the loop. And we don't think that's safe."

Omada president Wei-Li Shao wrote in an email that he supported the idea of fees aligned to outcomes but that “the payment levels don't cover the cost of delivering the high-quality, evidence-based care Medicare beneficiaries deserve.”

Kelly Bliss, president of U.S. group health at Teladoc said in a statement that she is encouraged by the broader policy conversation that ACCESS is driving and that the company is exploring ways it might support the program such as by “engaging with early cohort participants who may need additional provider support to hit their outcome targets.”

Much has been made of the program's payment rates, which were intentionally set low by Medicare regulators to incentivize the heavy use of technology to provide care at lower cost. Perez's view above offers the commonly raised counterpoint.

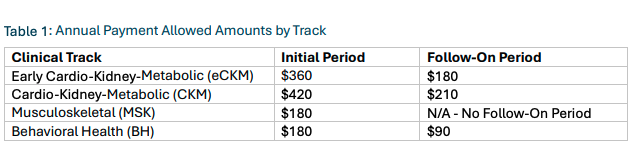

Given these decisions were driven by economics, I wondered how much lower the ACCESS payment rates were than what the companies might earn from a typical patient. In the chart above I calculated the average revenue per user based on year-end 2025 revenue and member counts from Hinge and Omada. It's interesting how those numbers measure up against potential earnings in the schedule of payment amounts below from CMS. ACCESS participants are only paid a fraction of fees if their patients do not hit outcome targets. And payment rates for the second year of management are significantly lower.

Note: Teladoc does not break out revenues attributable to its 1.2 million chronic care members. Hinge publishes a metric for billings over the last 12 months which it says accounts for seasonality of revenue. Using that metric, it billed $857 per member in 2025.

I'll have more to say on ACCESS soon. Open to perspectives.

research

The AI device house of cards

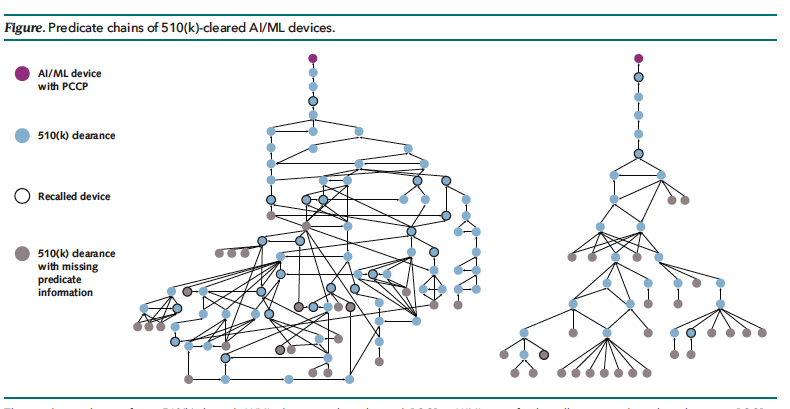

The image above isn't a couple of wild new AI-designed molecules — it describes the chain of Food and Drug Administration predicates behind a pair of AI-enabled medical devices. It's taken from a new analysis in the Annals of Internal Medicine that argues the common 510(k) regulatory pathway could pose real risks as more AI devices go through the agency. Brittany Trang had an excellent interview with authors Kyra Rosen and Ken Mandl earlier this week in her AI Prognosis newsletter.

Most medical devices authorized by FDA come to market via the 510(k) process under which manufacturers only need to show that their products are "substantially equivalent" to devices that have been cleared before. This usually doesn't require clinical evidence. As devices are cleared upon devices upon devices, you end up with a regulatory game of telephone where the originally cleared product might not look anything like the most recent one.

No comments