🏥 The Hospital Bear Market?

|

|||||||||

|

|||||||||

|

|

|||||||||

Hospitalogists, HCA recently announced a preview of its Q2 earnings results, and I wanted to dive into the broader context around why things are worse than expected on the ACA front along with macro themes at play for providers nationwide. Let’s dive in, and as always, drop your thoughts in the replies. I recently got hit with a ton of spam bots which made it nigh on impossible to read actual replies…but we are so back now, baby. PS - Who's going to the Vizient Connections Summit in Sept? I'm thinking of hosting a happy hour. Let me know! Was this email forwarded to you? Sponsored by Motivosity One of the biggest influences on patient experience is how your caregivers show up for work. A new report shows it’s not just long shifts and heavy emotional lift that are contributing to caregiver burnout. It’s also feeling invisible inside their own organizations.

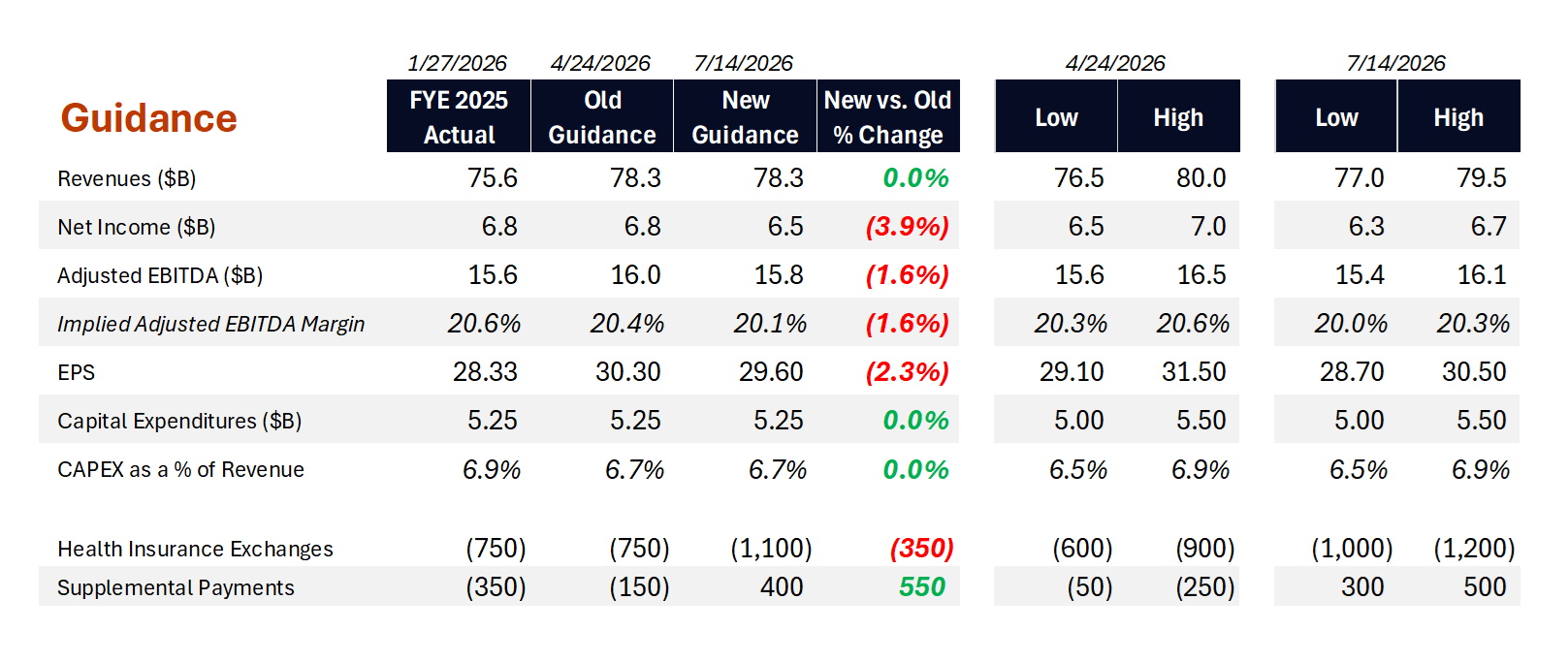

There’s a gap between showing up and feeling seen, and it’s fueling turnover. Discover what the orgs closing this gap are doing right in the 2026 State of Workplace Culture & Connection: Healthcare report from Motivosity. Shifting Tides: HCA’s Yellow Card?Somewhat unexpectedly (almost as unexpected as England losing that game to Argentina with 15 minutes to play), HCA provided a preview of its Q2 results along with updated guidance detailing the following:

Context: heading into 2026, HCA expected an adverse impact on adjusted EBITDA of between $600M and $900M, with $150M impact in Q1. From the advance Q2 update provided this week, the disenrollment trend has accelerated in Q2. HCA is bumping this number UP to between $1B and $1.2B. So the expected negative impact to adjusted EBITDA is ~$400M higher than anticipated. HCA noted they expected disenrollment to accelerate in Q2, but impossible to exactly quantify. Hence the Q2 pre-update. The total impact is as follows, with some slight hits to profitability in 2026:

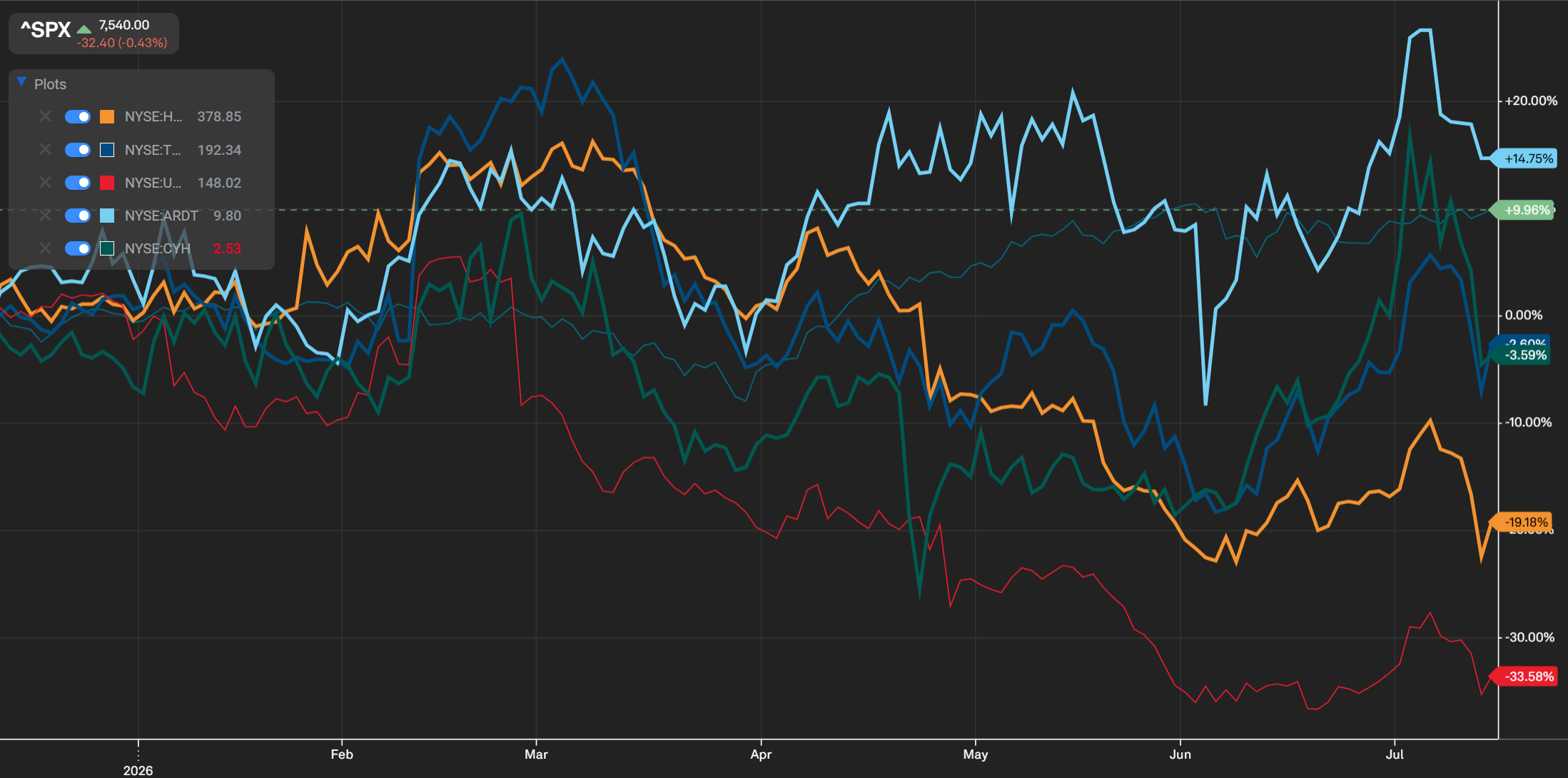

On the week, HCA is down ~5%, and as much as 10% when this news dropped:

More broadly, most publicly traded hospital names are underperforming the S&P 500 index with HCA and UHS being the biggest laggards. Forward looking as they are, markets are generally bearish on hospitals year to date.:

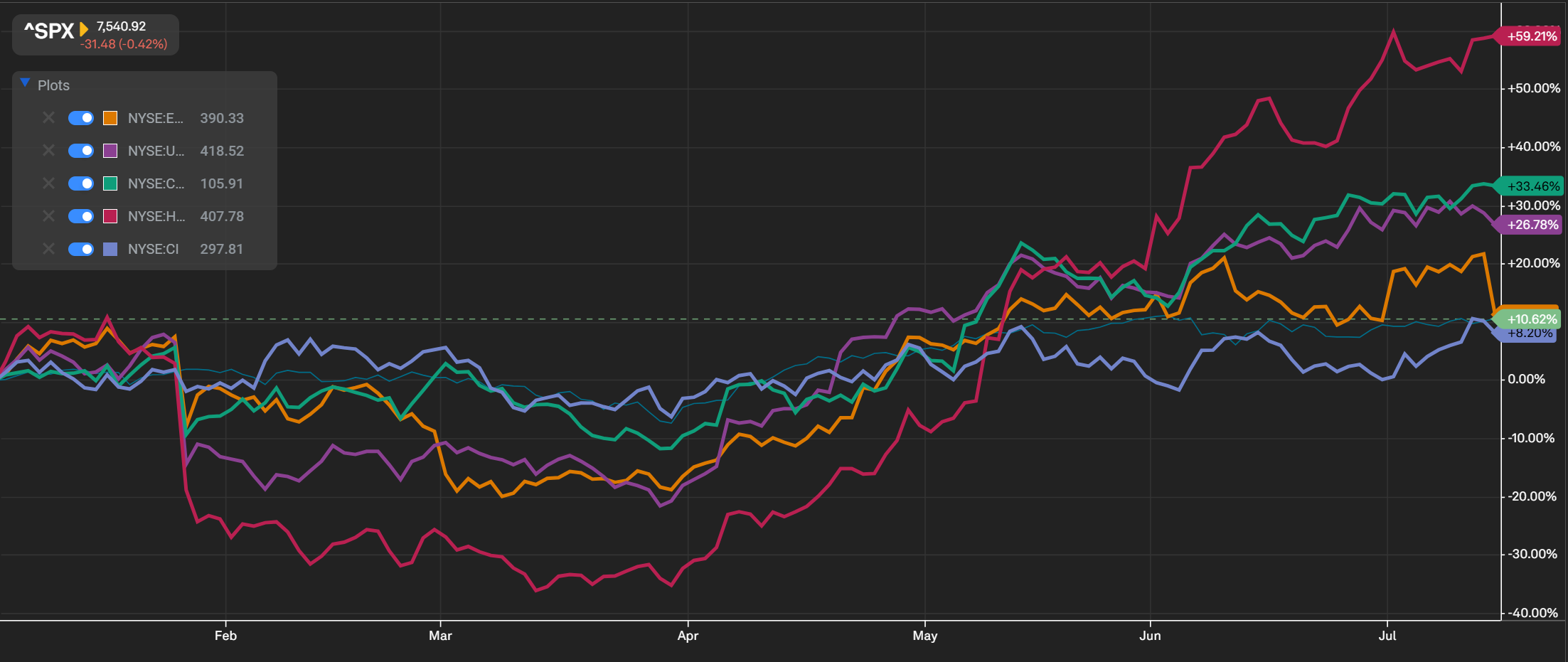

We’ve seen a definite shift in investor sentiment since Q1 between provider organizations and managed care names. Now compare public hospital performance to the managed care giants, and you can see where investor expectations lie, particularly since April, or Q1 readouts:

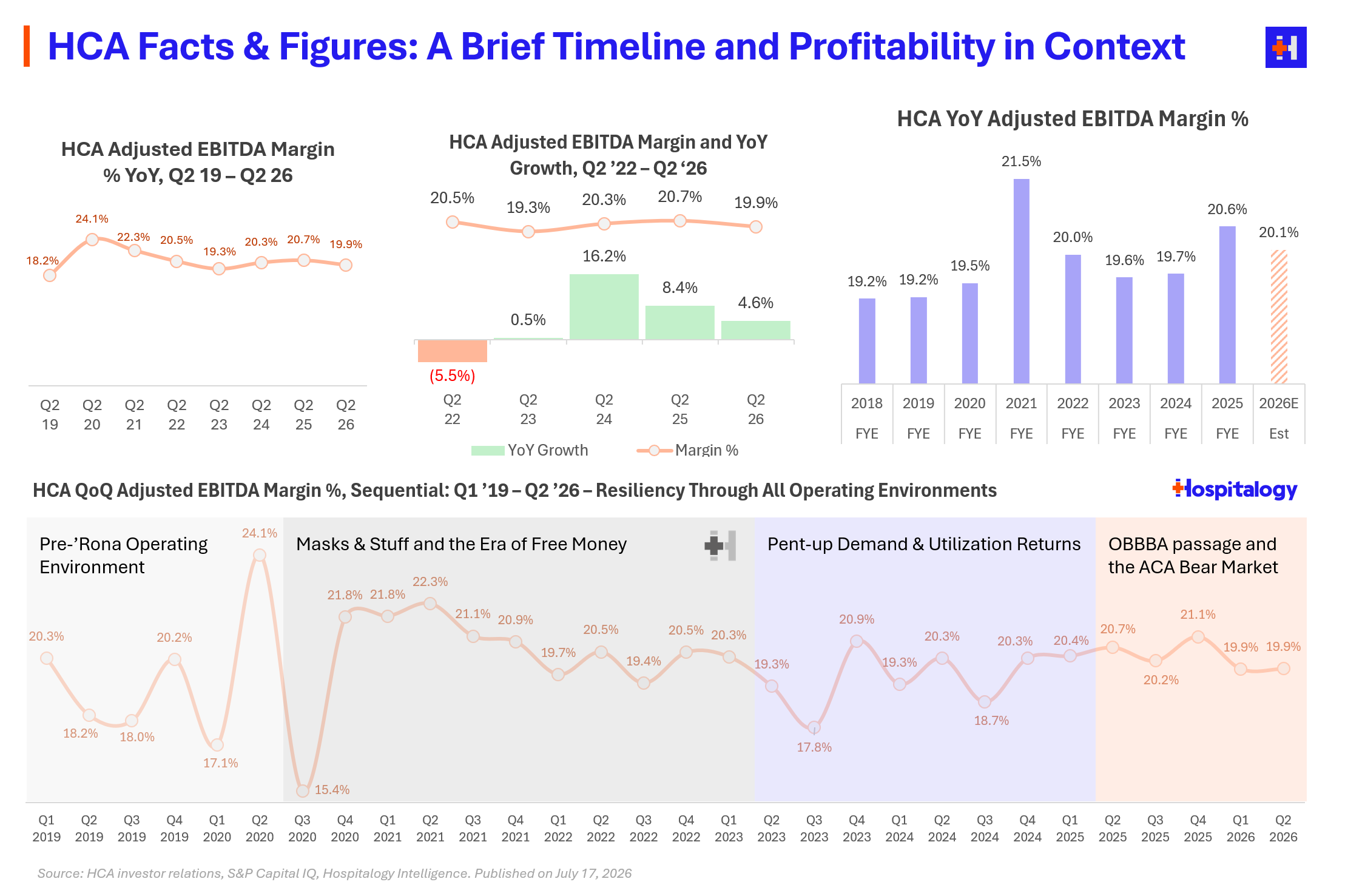

So here’s a breakdown of the dynamics at play for HCA, trying to connect some datapoints along the way. If history is any indication, HCA can operate profitably through any operating environment.

Its core thesis has always remained intact: operate in growing, attractive markets, solve for density, and invest in what feeds the bottom line. Do so as efficiently as possible. This thesis is still in play in 2026 despite largely ignoring popular conversations around value-based care or other policy initiatives. HCA will play ball with the waxes and waning of the national conversation, but they’ll continue to invest in the fee for service bread and butter, standing up de-novo facilities and buying urgent care and freestanding ER footprints. And they’re spending ~$5B+ a year to do so - inpatient bed expansion, ER capacity expansion, and outpatient network expansion (ASCs, urgent cares). Most headlines around hospitals and health systems have been policy focused. OBBBA, Medicaid cuts, potential reforms in site neutral payments and 340B, ACA dis-enrollments. And all of these (and more) are extremely valid headwinds for health systems. The hubbub may lead you to believe ACA as the primary catalyst to HCA’s underperformance when in reality any signs of decelerating volume trend is much more impactful to HCA’s business and hospital economics at large. HCA’s entire estimated impact to ACA dis-enrollments in 2026 is offset by other favorable, unknown outcomes in supplemental payment programs including grandfathered approval of the Georgia program, reinstatement of the ATLIS program (another fun acronym I just learned today) in Texas, and the YoY benefit from the Tennessee program, in addition to the approval of the Florida program (timing expected in Q2). This section is the part of the report I found the most notable:

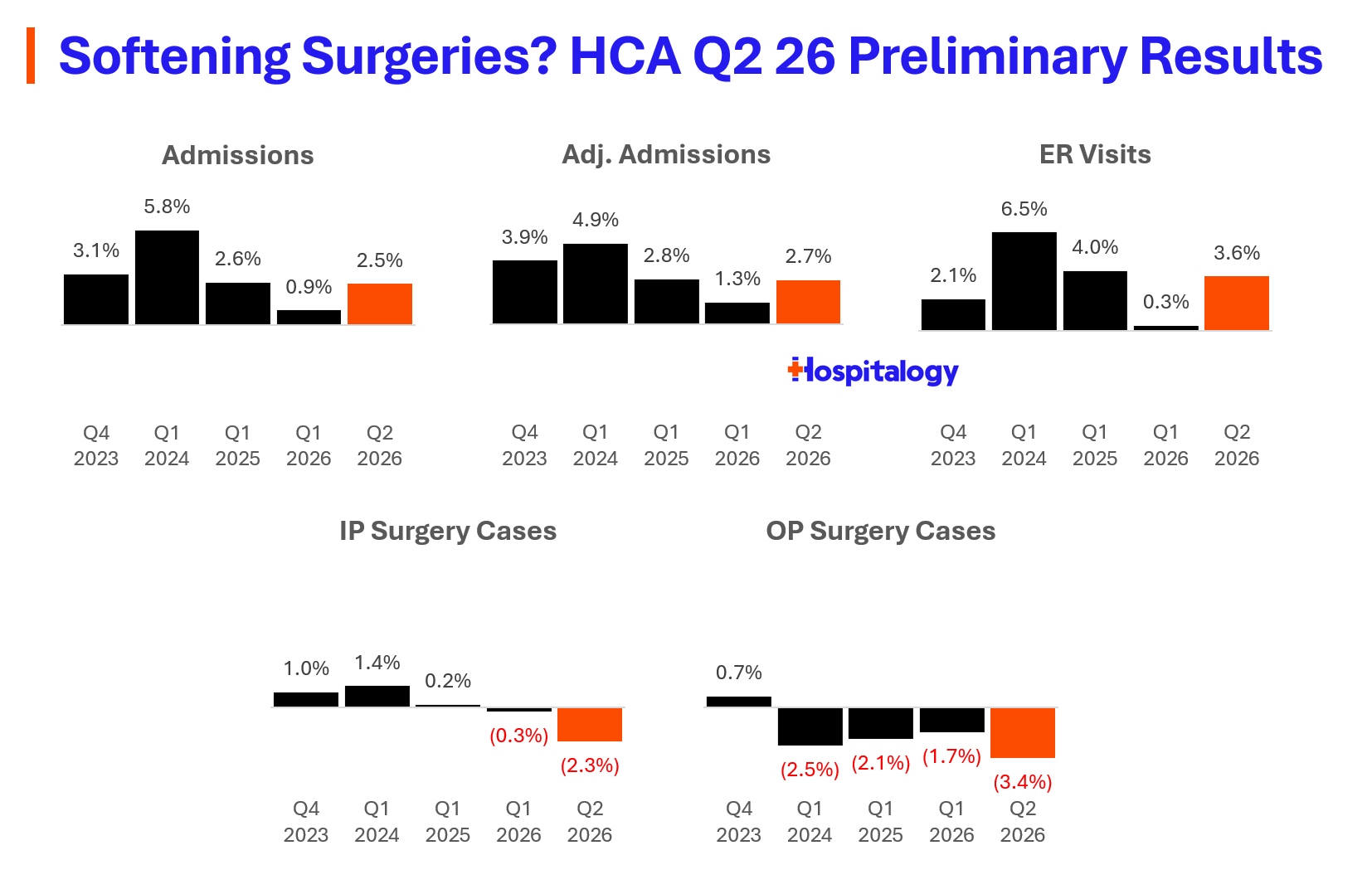

HCA has been dealing with outpatient surgical volume attrition for some time now (self diagnosed as attrition in Medicaid and uninsured populations), and makes up for it on the back end with reimbursement and acuity. But the past 2 quarters have also seen inpatient surgery declines stemming mainly from a weak respiratory season and storms. Recent commentary from HCA noted some weakness in hospital-based IP ortho procedures and low acuity service lines in ASCs like ophthalmology and ENT. So the question is whether these are structural weaknesses in demand or blips on the radar. Perhaps the emerging explosive diarrhea cases will stymy the volume softness flow (sorry, can’t help myself, but you have to admit that was a great multi-layered one). Bottom line: markets are pricing in expectations for 2027, and the bearishness is palpable. Which leads me to wonder whether we’re seeing an overreaction or if things are about to get significantly worse. Everyone is expecting the hospital shoe to drop (AKA, the poor operating environment starting in 2027). What do you guys think? And how are you preparing for next year? Reply with your top strategic priorities and how you’re addressing them. I’ll put together any responses in part 2. Part 2 next week will dive into recent managed care commentary, assess the current state of the ACA and enrollment dynamics, and dive into implications from OPPS, MPFS, and rural health transformation Sponsored by Navvis Participating in TEAM? Benefit from:

Get a complete framework for success in TEAM. HOSPITALOGY READS & RESOURCES

MISCELLANEOUS MADDENINGS Pray for us. This weekend begins potty training boot camp where we're locked in for the next 3 days with a naked hoodlum reining terror (and pee) everywhere he looks. It's gonna be fun! Also, reply with your picks on who will win the Open Championship. My pick is Cameron Young. He's had a great year and would be awesome to see it culminate in a major win. Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|||||||||

|

No comments