PARTNERED WITH  |

|

|

Happy Tuesday, Hospitalogists! Today's newsletter is a hodgepodge of stories I think you'll find highly relevant, interesting, and useful. This one took...a while so if you could forward it along to your colleagues and spread the good news of the wonderfulness of Hospitalogy I would greatly appreciate it! By the way...I need a favor from you guys. If you're tracking the weird mood swings of the healthcare economy (one day full-speed on M&A, the next a screeching halt), then do I have a webinar for you!

I'll be joining Unlock CEO Brandon Edwards to unpack What's Trending in the Business of Healthcare on May 15th. We'll be talking shop in an interactive format. It'll be a blast. You, me, Brandon, and healthcare hot takes. What's not to love?

Join us by registering here: https://go.unlockhealthnow.com/wbnr-051525/ |

Was this email forwarded to you? |

|

|

SPONSORED BY NAVINA AI that earns physician trust is rare. AI that reduces burnout? Even rarer. Phyx Primary Care studied one that did both. Phyx Primary Care (an independent innovation lab spun out of AAFP) set out to study Navina's AI Copilot across 120 physicians and 19 practices.

The findings were striking: a 40% drop in chart review time, a 32% decrease in burnout, and a 1.9-point lift in STAR quality scores.

When AI is built for clinicians - not just around them - it doesn't just promise impact in value-based care. It delivers. 94% said it was easy to use. 92% trusted its insights. Download the full Phyx report to learn more.

|

|

|

Omada Health is next up on the public markets, files its S-1 |

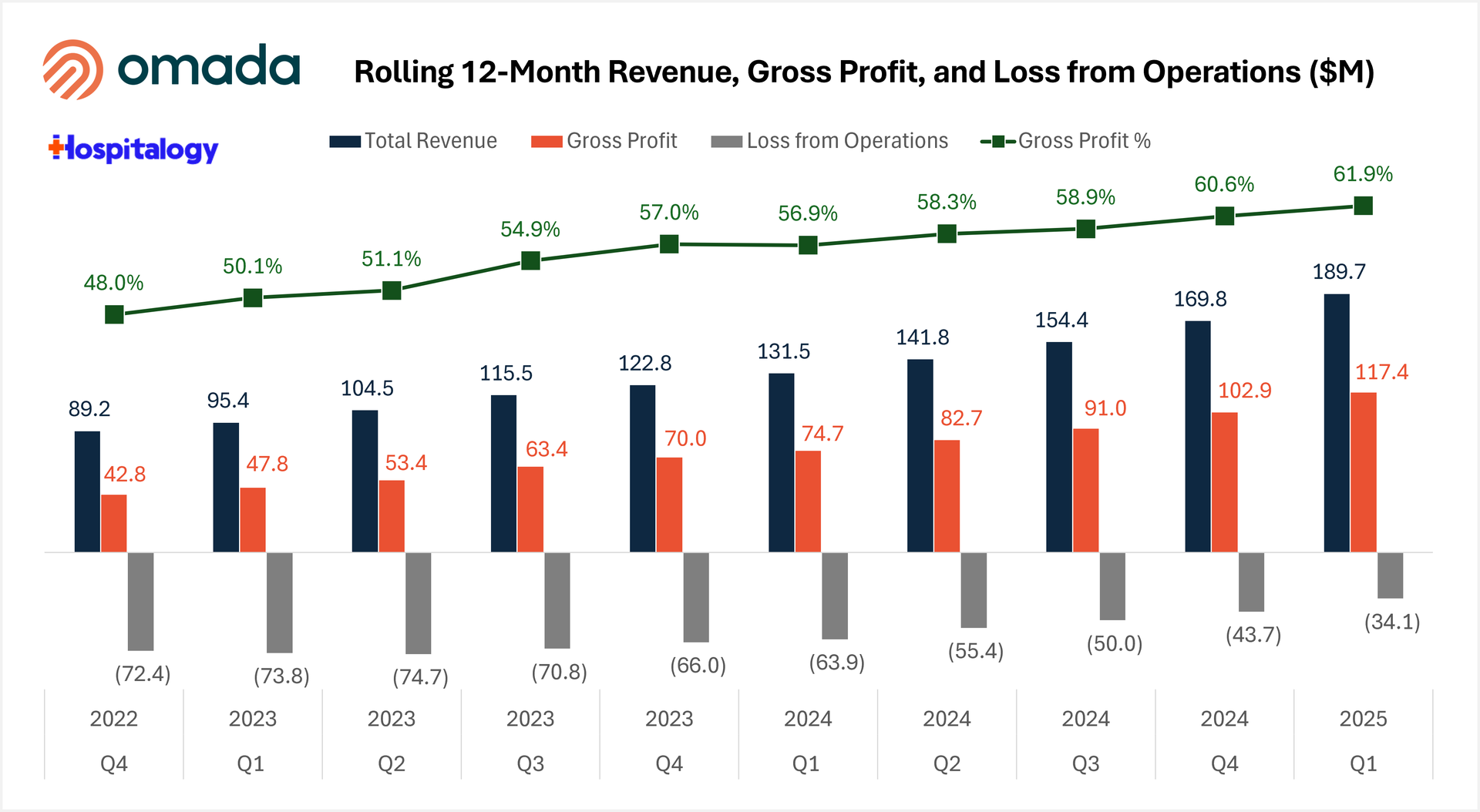

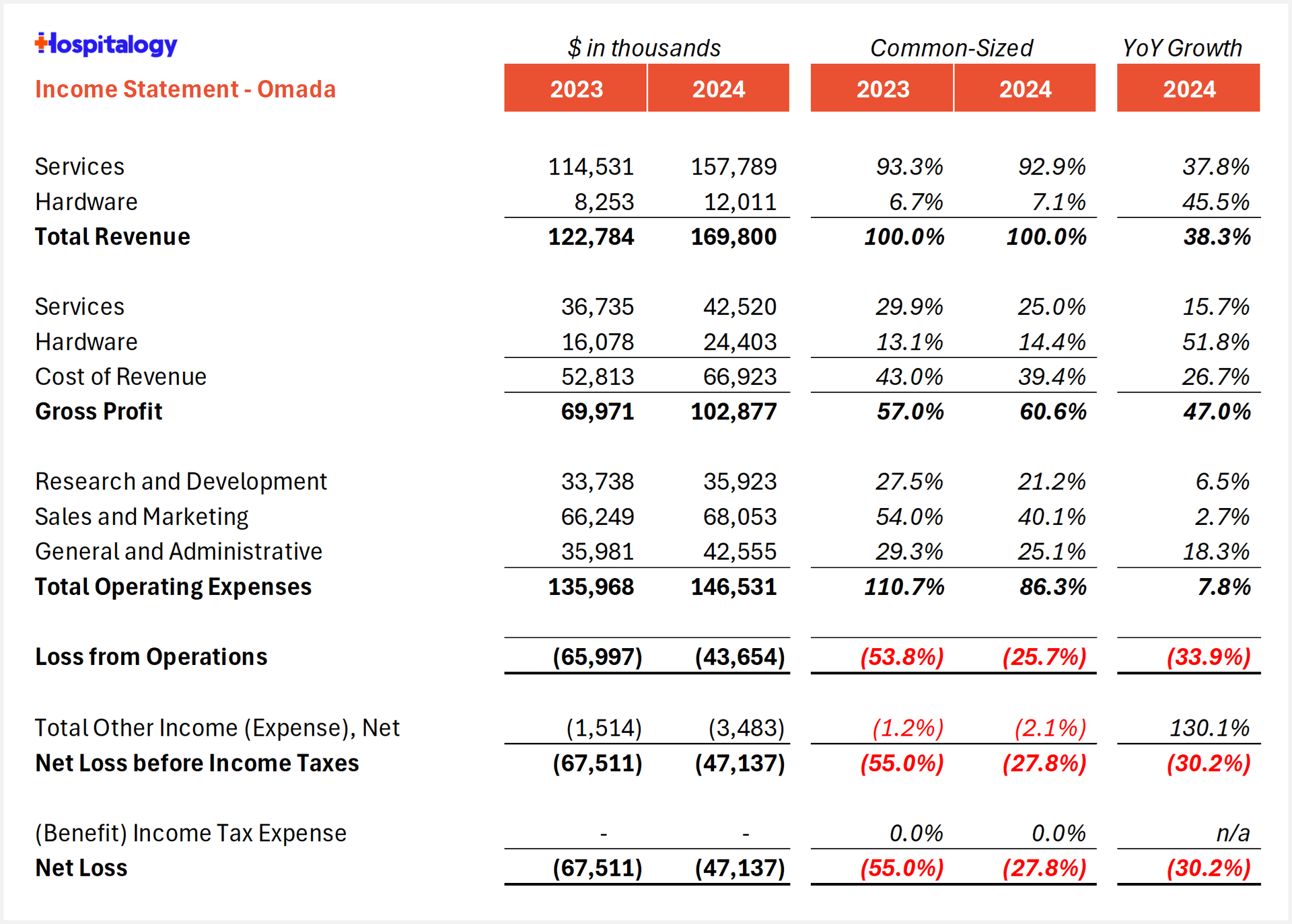

Omada filed its S-1 (linked here in all its glory) on Friday, and I've included some highlights below for you guys. For Hospitalogy community members, you can watch my conversation with Omada's founder Sean Duffy here - probably one of his more recent interviews prior to their filing, so very timely and diving into current, trending topics with the firm. A more robust dive will probably come in the next week or so. Following Hinge, Omada serves a similar employer and payor demographic (with some key partnerships with PBMs) and runs cost-saving, high quality chronic disease management programs across areas of high need and spend including hypertension, diabetes, MSK, and of course, obesity. In the filing Omada touts its effectiveness as a full-stack virtual platform. Financials: In 2024, Omada generated $169.8M in revenue (38.3% YoY growth) and $102.9M in gross profit (60.6% margin), while its losses totaled $43.7M - substantial but shrinking quickly. More to come from me on Omada in the near future! In the meantime, hit me with your first impressions. |

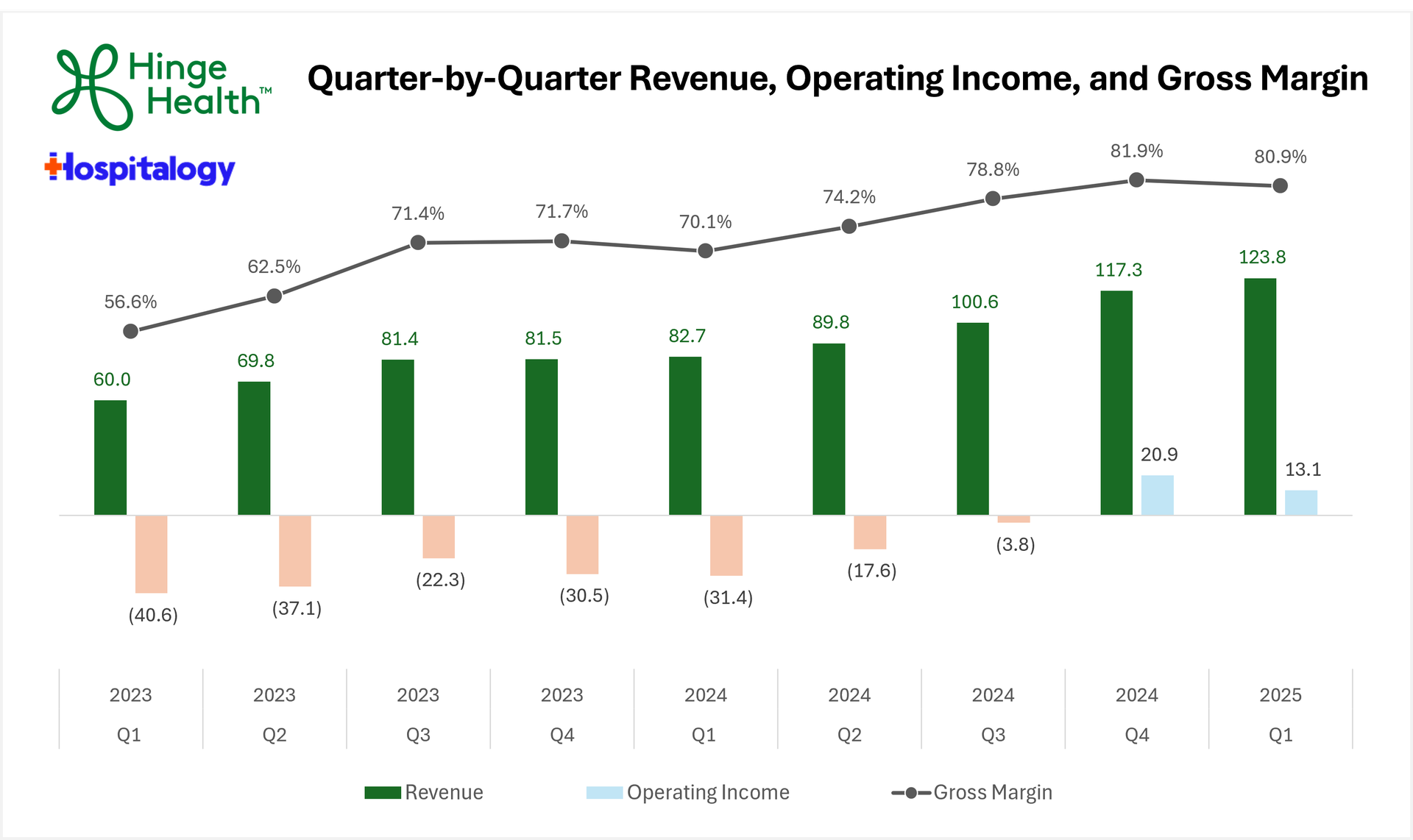

Hinge Health Aims for ~$2.4B Valuation in updated IPO Filing |

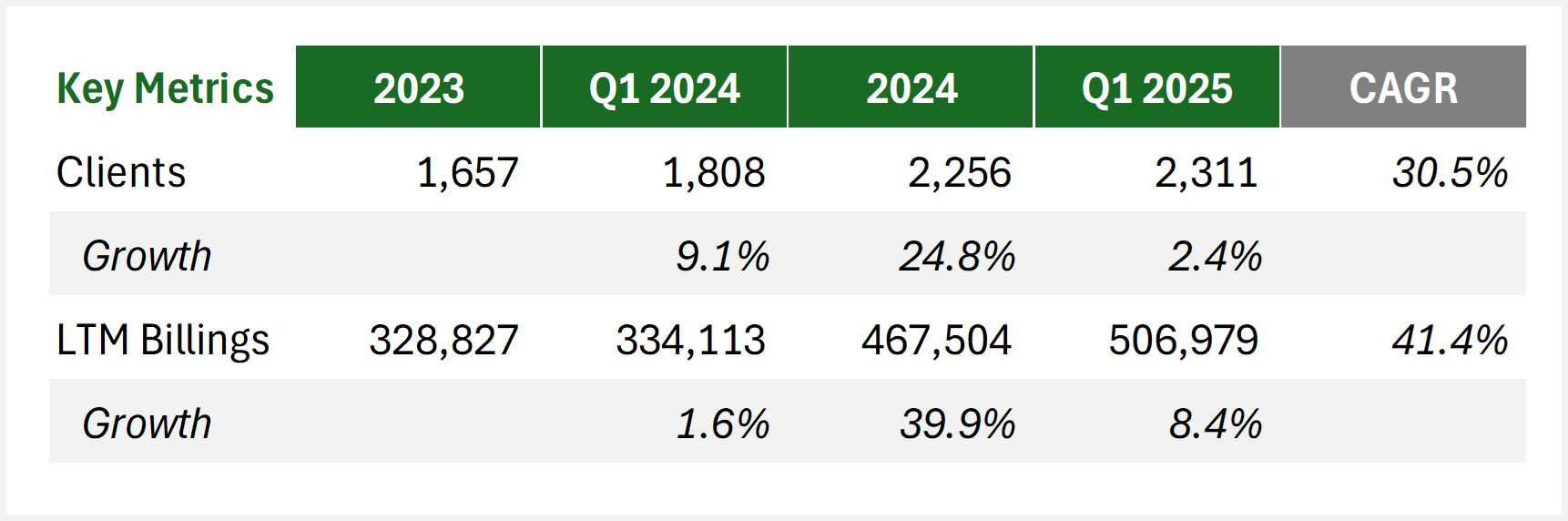

At the implied midpoint, Hinge would be publicly valued at around $2.4B. It looks as if Hinge's investors got the memo, as the company is taking quite the haircut to its last reported private valuation of ~$6.2B, if memory serves. Like I laid out in my Hinge S-1 analysis and my thoughts on its invest-ability, it's the right move. And now…it's sure to entice some folks into the tech-enabled space. What about you? And based on this haircut, I have to wonder what valuation Omada will aim for.

For instance, as a quick thought exercise, if Hinge hits around $500M in 2025 revenue (their Q1 25 calculated billings being $506M), a $2.4B valuation implies around a 5x forward revenue multiple. So I'm pleasantly surprised.

In Omada's case, assuming 40% revenue growth in 2025 and applying a similar multiple gets you to ~$240M in forward rev and an implied valuation of ~$1.2B. That sounds…not crazy and reasonable upside for what you're paying for? Someone check me on that. Health tech valuation practicality? |

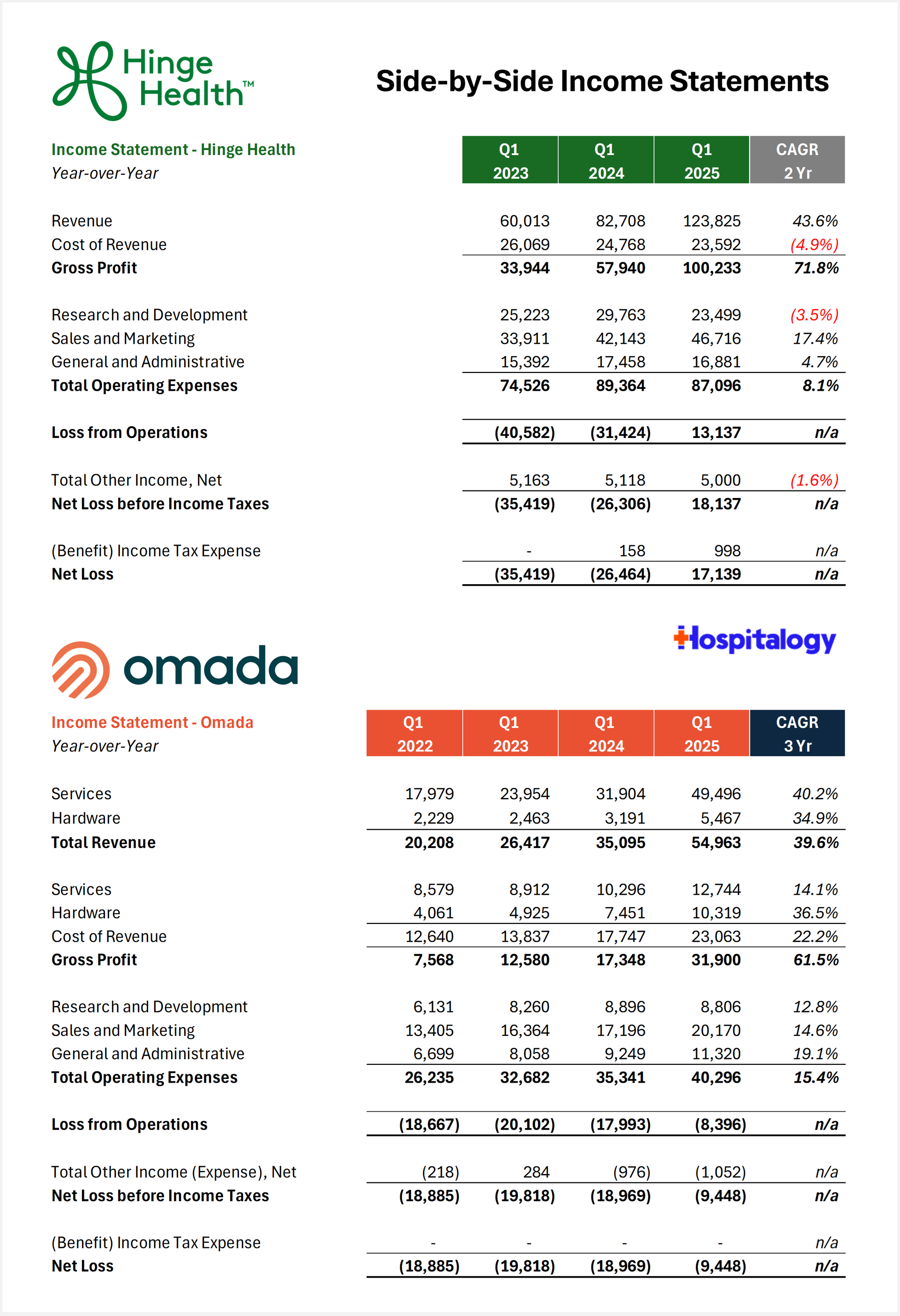

Here's a side-by-side comparison of Hinge and Omada income statements in their most recent quarters. Hinge turning a nice profit. Omada working toward that goal fast-like. You can see the year-over-year trend (and yes, I know it says net loss even though they're making money. I'm too lazy to fix it at this point). Omada was even nice enough to give us an extra set of four quarters back in 2022 - something they weren't required to do. Revenues are growing, and gross profit is increasing even faster than revenues, displaying some impressive operating leverage from both soon-to-IPO firms. The question is whether that's sustainable into the future, but for now it appears to be working out. And both Hinge's and Omada's Q1 '25 results are impressive as hell. 49.7% and 56.6% revenue growth over Q1 '24, respectively: |

UnitedHealth Group's CEO Andrew Witty steps down |

One of the more shocking headlines so far in 2025, UnitedHealth Group's Andrew Witty is stepping down after perhaps the Empire's managed care titan's worst Q1 print ever, including its first earnings miss since 2008 (I broke down their Q1 in plenty of detail here if you want to learn more). Someone needs to take the blame for UnitedHealth's woes in both Optum and Medicare Advantage - across severe v28 transition challenges, way higher than expected utilization, and poor engagement with new members - and it appears as if Witty is the scapegoat for the job. Don't worry about UnitedHealth Group, though. Replacing Witty is Stephen Hemsley, who knows his business when it comes to the company - he's an OG, joining in 1997 and running the firm from 2006 thru 2017. As I heard from a third party…"you don't bet against Stephen Hemsley." For now, UNH stock is down 40+% on the year, and investor questions arise around United's full capitation strategy with Optum including the all-in pivot to value-based care, something Witty set in motion over the past decade in building Optum's physician base. |

Trump signs new executive order on drug pricing, reinstitutes 'most favored nation' policy. Plus, CMMI's new strategic vision |

In an executive order scant with details beyond triumphant nice-to-have's, the new administration established its goals to reform drug pricing in the U.S. Here's a good breakdown of the context of the executive order from Politico. Citing other developed nations drug prices and the profit levels in the U.S., the executive order seeks to create a 'most favored nation' policy within Medicare, something Trump tried to implement in his first regime but was ultimately bogged down by…the swamp? Big Pharma? However you want to characterize his antagonists, things didn't pan out. Still, between that and calling out enabling direct-to-consumer sales to Americans, the takeaways here are clear: this administration is focused on the consumer, and trying to find pockets where it can create competitive forces in healthcare. The executive order is unclear on the…execution of its policies, but stakeholders squarely in the spotlight here include pharmaceutical manufacturers and PBMs, since the DTC programs potentially seek to disintermediate them. Meanwhile, in theory, lower drug prices would benefit patients and payors (lower medical spend). - Also, a quick note on something I found hilarious. In a recent presser, Trump seemed to allude to a certain 'neurotic billionaire' (Elon Musk) paying $88 for 'fat shot drugs' in London while paying $1,300 in New York. The video is something else. What timeline is this again? (Oh yeah. The most insane one, since Lizzy Holmes' new partner seems to have raised $20M and formed a new BLOOD TESTING company. You really can't make this stuff up. )

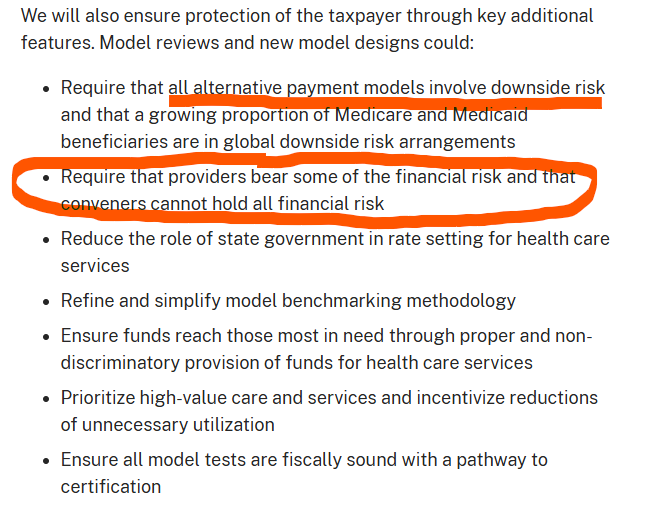

CMMI's New Strategic Vision: Today CMMI held a virtual event to unveil its new strategic direction under the helm of Dr. Oz. centered around 3 key pillars in the MAHA movement, and nothing unexpected: - Promoting evidence-based prevention

- Empowering people to achieve their health goals

- Drive choice and competition

Obviously these sound great, but the actual implementation of these policies will ultimately decide the future of healthcare under the new regime. So some of the specific mechanisms mentioned included reforming state certificate of need (CON) requirements and requiring independent providers to participate in downside risk arrangements (AKA, conveners or enablers can't take the downside risk burden from their contracted physicians if I'm interpreting that note correctly) so that's somewhat notable. What else did you guys find in the announcement? Hit me with your thoughts. |

|

|

SPONSORED BY STELLAR HEALTH Primary care is evolving fast. Are payors evolving with it?

On May 22, Stellar Health and Fierce Healthcare are hosting a webinar: Solving the Primary Care Conundrum. They'll dig into how payors can build smarter networks and design incentive models that actually work, for both providers and health plans. Can't join live? No worries. Register anyway and get the full recording to watch whenever it works for you.

No one's bridging the plan-provider gap like Stellar Health, the only microincentive solution built for both.

|

|

|

More Large Health System Patient Revenue Analysis Stuff since I can't help myself |

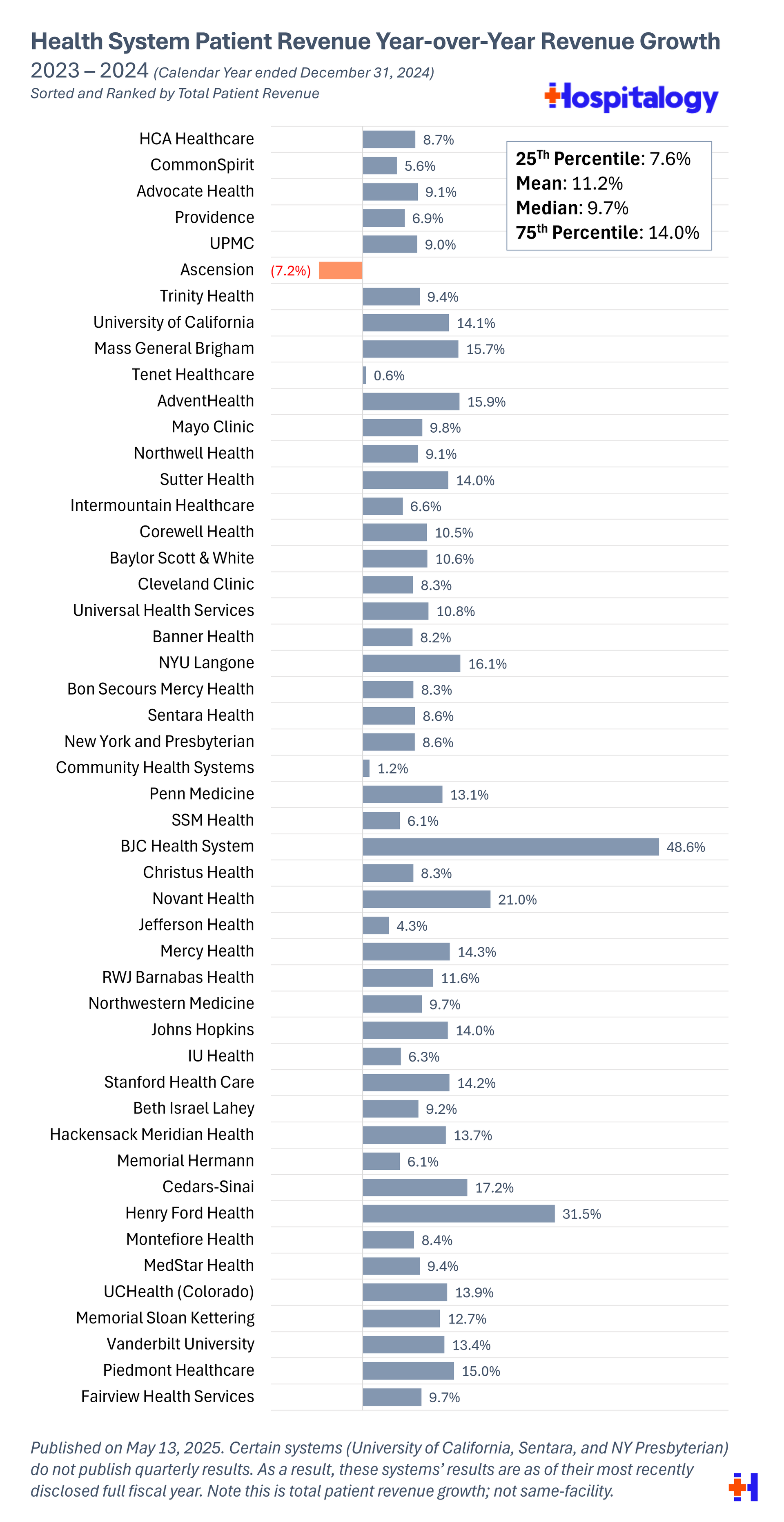

Health System Patient Revenue Growth Analysis: Here's a nice, clean graphic you all can steal from me add to your internal presentations on health system performance. It lists the top 50 hospitals and health systems by total patient revenue, and the bar graph shows 2024 patient revenue growth over 2023 - as of this calendar year. Median patient revenue growth for 2024 was 9.7%, so pretty solid for the large for-profit's and nonprofits as utilization returned in a big way. It's why we've seen a decent amount of margin recovery and expansion in 2024. 2026 will be a different story with ACA enhanced subsidies expiring. |

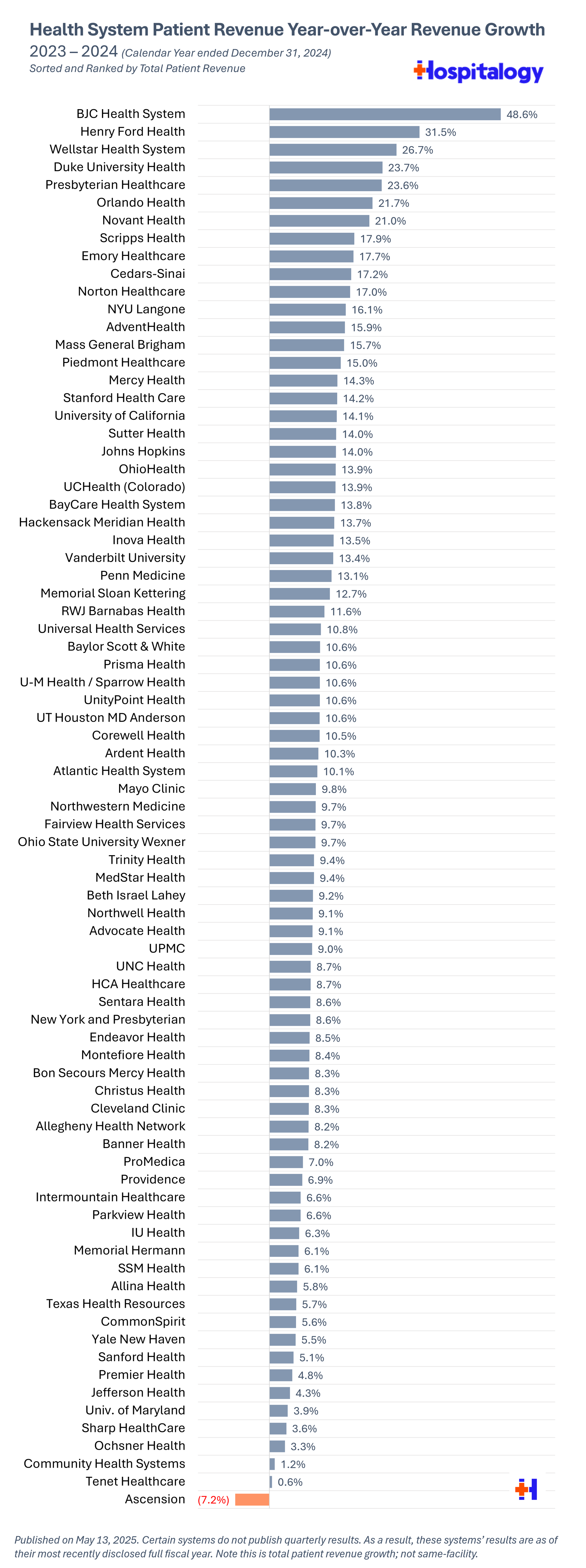

And here are the top 80 health systems (for the most part, anyway. I probably missed some names) sorted by patient revenue growth, with the biggest jumps at the top coming from M&A (note that this isn't same-facility growth - it's total growth): |

My favorite reads & resources from the week |

*This read is brought to you by one of my brand partners who help make this newsletter possible! |

|

|

Random personal anecdotes and musings from me |

How about them Mavs?? I loved seeing all of the memes of Nico Harrison as if he's Littlefinger from Game of Thrones. As if the dude is smart enough to think that far ahead. No, we're just lucky that God himself is looking out for the good 'ole Dallas Mavericks with a 1.8% chance to snag that #1 draft pick. Welcome to Dallas, Cooper Flagg. We needed this. The PGA Championship at Oakmont...who are you guys picking? On paper, this course seems to have Rory written all over it. I could see it, honestly. But I wouldn't be surprised to see someone like Aberg winning. He's been playing solid all year. Of course I'll always hope for the best for my boy Spieth. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

.png) | Share Hospitalogy, Earn Rewards | Have friends who'd love Hospitalogy too? Click the link below to share Hospitalogy with your friends and earn awesome rewards! | |

|

PS: You have referred 0 people so far | | Share Hospitalogy! | |

|

|

|

|

Get your brand in front of 43,000 executives and healthcare decision-makers. |

Hospitalogy Membership - the best value in healthcare |

I'm building an exclusive community for top healthcare strategy and corp dev professionals. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments