Happy Thursday Hospitalogists,

As we mourn the loss of college football (congrats to Indiana; we're coming for you next year), I thought, "what better way to distract my readers than with some heavy hitting healthcare analysis?"

So without further ado, here's an incredibly information dense newsletter covering all your need-to-know's from January. If I missed anything, you're wrong (kidding, please let me know!)

Let's dive in. |

Was this email forwarded to you? |

|

|

BLAKE'S BREAKDOWN: JPM 2026 |

Going a bit deeper on an interesting topic, theme, or resource |

The annual pilgrimage to San Francisco delivered exactly what you'd expect: management teams putting their best foot forward, guidance ranges that leave room for "beat and raise" narratives, and enough strategic buzzwords to fill a bingo card. But buried in the presentations were genuine signals about where healthcare is heading in 2026 and beyond. The Great Specialty Pivot Every publicly traded healthcare company at JPM25 is telling you the same thing: commodity businesses are dead. specialty is the only margin story that matters. McKesson, Cencora, and Cardinal are all racing to own the physician relationship through vertical integration. Carrier vertical integration is dead. Long live drug distributor vertical integration! MSO investments include areas of key specialty drug cost / utilization growth like oncology, autoimmune, and retina. Control the point of prescribing, lock in contracts and drug margin and everything else follows. McKesson's USON touches 20% of U.S. cancer patients. Cencora accelerated full OneOncology acquisition to capture synergies immediately. Cardinal's chasing the 80-90% of specialty physicians who remain unaffiliated. The white space in multispecialty, oncology adjacent areas represents the next frontier now that oncology is maturing. Meanwhile, data moats are separating AI winners from also-rans. Tempus is building 400+ petabytes of multimodal data and claiming to be "AWS, GCP, and Azure in one company." Waystar's uniting 7.5B payment transactions with clinical data through iodine. The competitive advantage isn't the LLM itself but access to proprietary organized information. As underlying technology becomes increasingly fungible, differentiation lies in platform-ization, expertise, data sophistication. V28 did exactly what CMS intended: separated companies built on coding arbitrage from those focused on genuine care delivery. Both Alignment and Astrana saw RAF scores increase post-implementation, indicating the advantage of conservatism in a rapidly shifting payment and policy environment, and distinct advantages while competitors got crushed. The oral GLP-1 transition is flipping from headwind to tailwind across distribution as refrigeration and special handling burdens diminish. Eli Lilly management claims leading GLP-1 companies now control ~80% of global manufacturing capacity. Medicaid under structural pressure with state-specific chaos. Acadia's quantification of New York's out-of-state Medicaid prohibition and California staffing ratio requirements creating material headwinds for Medicaid-indexed businesses. Other great reads and overviews: What's the most underappreciated theme you're tracking from JPM? |

White House Releases the Great Healthcare Plan With a Great Lacking of Detail |

Trump released a health policy framework calling for HSA subsidies instead of ACA premium support, prescription drug pricing codification, and expanded price transparency requirements for hospitals, physicians, and insurers. Scant on specifics, but lofty goals that policymakers will have to sort through. |

|

|

EXECUTIVE SUMMARY: JANUARY 2026 |

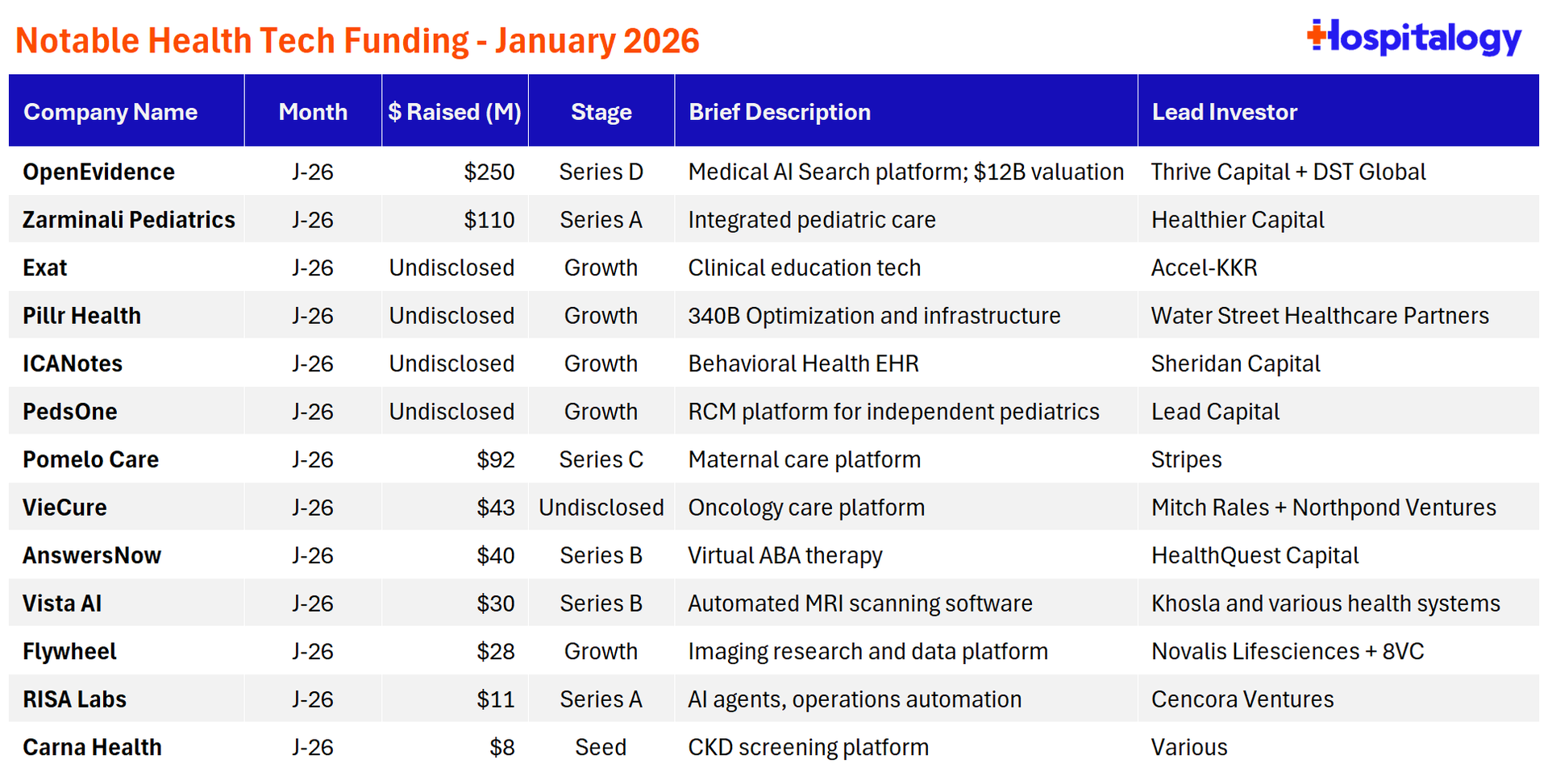

OpenEvidence raised ANOTHER $250M tranche at a $12B valuation - and they're proclaiming themselves as 'the most valuable healthcare AI company in the world.' Sure buddy, on paper. To date OpenEvidence has raised $700M+ and is used by more than 40% of physicians on a daily basis - so, a bit over 400,000 if you assume the number of MDs has stagnated at around 1-1.1M. I also enjoyed this podcast from the Heart of Healthcare and OpenEvidence's CTO Zack Ziegler from November. Boston Scientific will acquire Penumbra for $375/share or $14.5B. The deal values Penumbra at roughly 6.5x trailing revenue. For health systems watching robotics and interventional cardiology converge, this deal signals where medtech capital is flowing: high acuity, procedural volume plays.

Kaiser agreed to pay $556M tied to aggressive MA risk adjustment coding practices, including using addenda and other mechanisms to increase submitted diagnoses. Which health insurer HASN'T been caught with their pants down in upcoding practices?

Amazon released an agentic Health AI companion for One Medical members, latching themselves on to the growing consumer and longevity trends. ONEM's health assistant will provide ongoing health guidance and copilot your scheduling, labs, and other patient-facing activities.

Healthier Capital closed a $220M oversubscribed Fund 1 on the heels of announcing a lead investment into Zarminali Pediatrics' $110M Series A on 1/21

TridentCare acquired DispatchHealth's imaging business unit, absorbing the mobile X-ray and ultrasound operation that spans 16 states. The deal consolidates portable diagnostic services in home, post-acute, and correctional settings. DispatchHealth continues to narrow its focus as it navigates the acute care-at-home economics. The divestiture comes a little under a year after the major hospital at home merger between Dispatch and Medically Home.

A new bipartisan healthcare proposal has emerged in the 11th hour and includes telehealth waiver extension (why is this not permanent yet?), hospital at home extension, nearly $5B for FQHCs, and add Medicare coverage for cancer detection screening. Still on the table includes PBM reform (rebate elimination) and ACA subsidies (increasingly unlikely).

CHS sells Crestwood Medical Center to Huntsville Hospital for $450M as portfolio right-sizing continues.

Prime Healthcare entered an asset purchase agreement for Franciscan Health Olympia Fields, the 214-bed hospital south of Chicago bringing its total footprint to 45 hospitals in 14 states.

MedPAC votes to recommend a 7% cut to home health payments. |

|

|

Notable Announcements from January |

Rock Health's end of year digital health funding overview noted that startups raised $14.2B across 482 deals in 2025 (35% YoY increase), with funding concentrated among larger rounds and AI-heavy companies. Shadow AI is becoming a real governance headache for health systems. Clinicians are using unauthorized AI tools for documentation and decision support, forcing CISOs and CMIOs to accelerate oversight frameworks. The gap between clinician demand and IT-approved solutions is widening. |

Epic v. Health Gorilla: a New Fight Begins. Brendan Keeler's breakdown of Epic's latest lawsuit. Grass is green. Vizient State of the Industry 2026 — Comprehensive overview of the reset facing hospitals and health systems. Covers cost pressures, demographic shifts, innovation acceleration, and the operational resilience required for 2026 and beyond. Vizient's annual report is consistently one of the better industry-wide frameworks. |

McKinsey Perspectives on Healthcare Industry Trends. Good outlook for providers, payors, health services, private capital, and pharmacy services. Trilliant Health: Revenue Impacts of Medicare Inpatient Only List Elimination: An interesting analysis models the revenue implications as 285 procedures move to HOPDs and ASCs. - Based on 2024 Medicare volume, total reimbursement for the 285 removed procedures would be $9.3B in a fully inpatient scenario and $4.0B in a fully outpatient scenario, with each 20-percentage point shift toward outpatient delivery reducing Medicare reimbursement by approximately $1.1B.

Kaufman Hall: Hospital and Health System M&A in Review 2025. Another one from the Vizient family, Kaufman Hall notes 2 trends that drove 2025 M&A: persistent financial challenges concentrated in smaller independents, and policy uncertainty around the new administration. Hospital M&A continues to shrink and be driven by portfolio realignment and bankruptcy rather than strategic interest or opportunity, with new facility growth coming from de novo builds. Continued movement away from independence among mid-sized systems in the $500M–$750M revenue range. |

Pray for us southerners as a potentially catastrophic winter storm approaches Dallas. We literally do not know what to do when it gets cold, so feel free to share any tips, or cold-weather recipes (we're already making chili and wonton soup)! Sending you good thoughts wherever you reside, fam. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 51,500+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments