Happy Tuesday, Hospitalogists, Today, I'm sharing a timely breakdown of the state of healthcare finance with Herd Midkiff and Kyle Kirkpatrick, partners at JTaylor. I'm also reminding you about next month's special virtual event, Scaling Primary Care with Agentic AI. 77% of health system execs plan to expand their primary care footprint and expect AI to be central to how that plays out. I'm hosting a session 4/28 that gets into exactly how to think about that: the strategy, use cases, and how to evaluate what's actually worth building toward. Join me? Grateful to Lumeris for partnering with me on this one. Enjoy! |

Was this email forwarded to you? |

|

|

The Squeeze Is Here: Inside the Forces Reshaping Hospital Finance in 2026 |

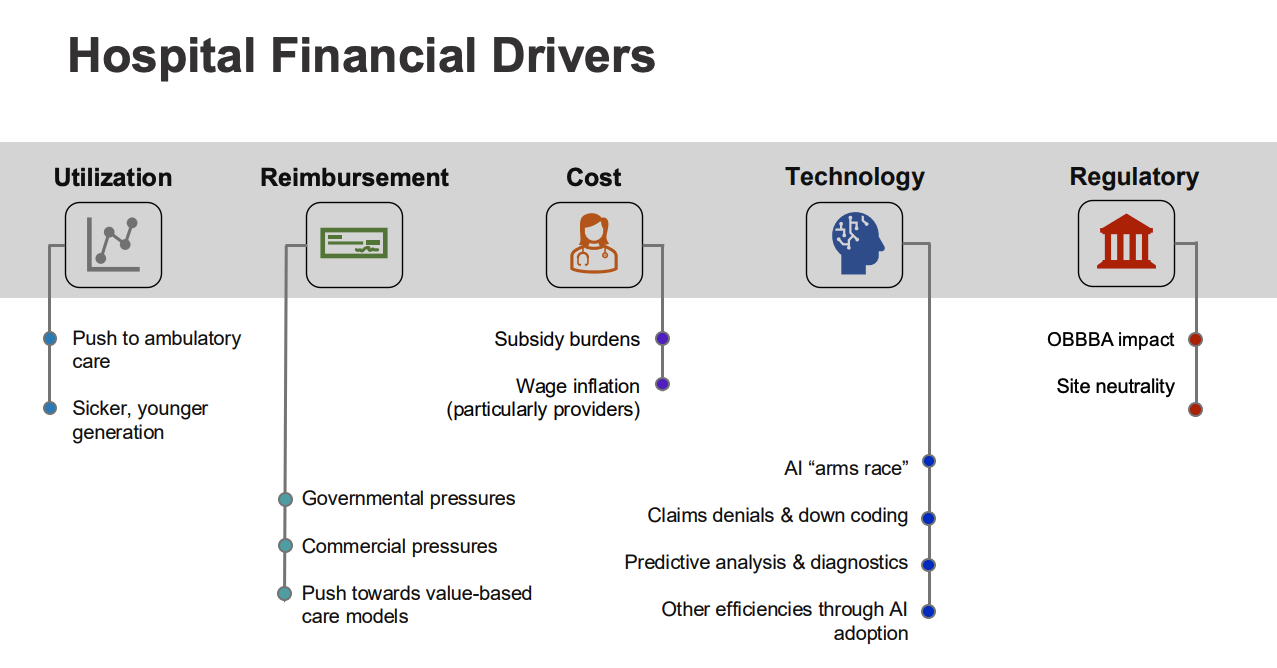

I hosted a community roundtable this week with Herd Midkiff and Kyle Kirkpatrick, both partners at JTaylor, a Fort Worth based consulting firm that works on valuation and transaction matters across the hospital sector. Herd and a colleague recently gave a presentation at the ACHE Congress on the current state of healthcare finance. They skinnied it down for our group, and the discussion that followed was too good not to write up. The full presentation deck is uploaded to the Hospitalogy community content library if you want to dig into the slides yourself. But here's my take on the big themes, plus some of the back and forth from the group. The through line across everything Herd and Kyle presented is one you already feel if you're running a hospital right now: the traditional margin model is under pressure from basically every direction simultaneously. Payor mix deterioration. Physician subsidy inflation. An AI arms race between providers and payors. OBBBA fallout. Site neutrality creep. And a widening bifurcation between the haves and have nots in the hospital world. Let me walk through it. (Download the slides here) |

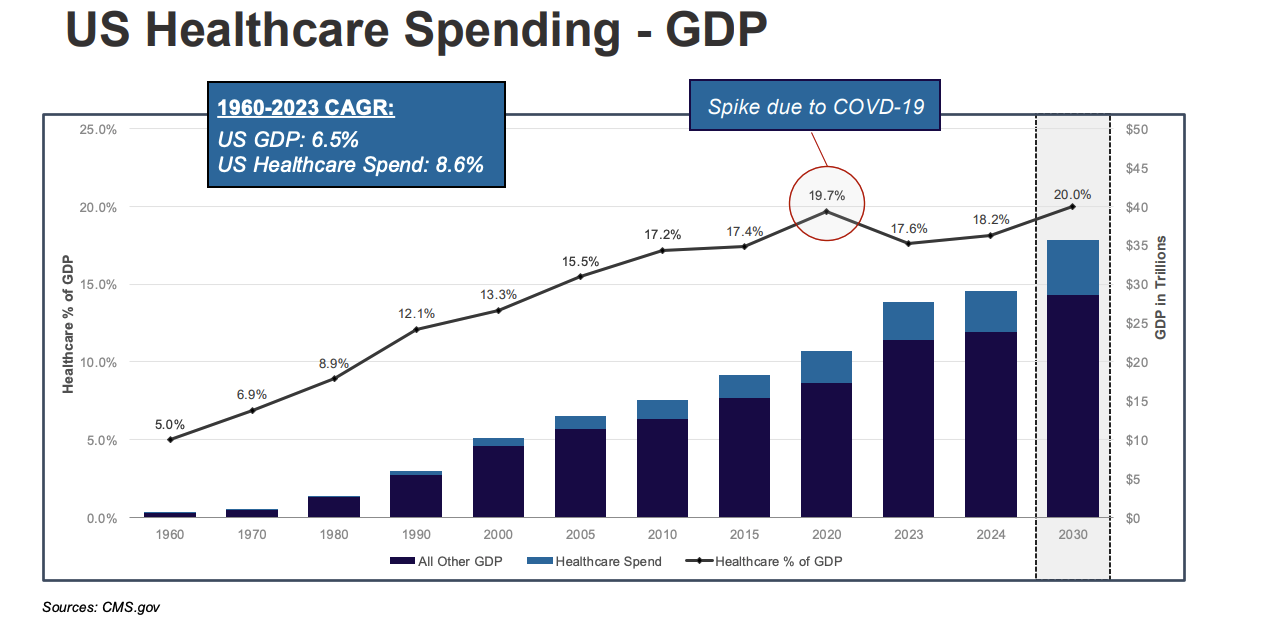

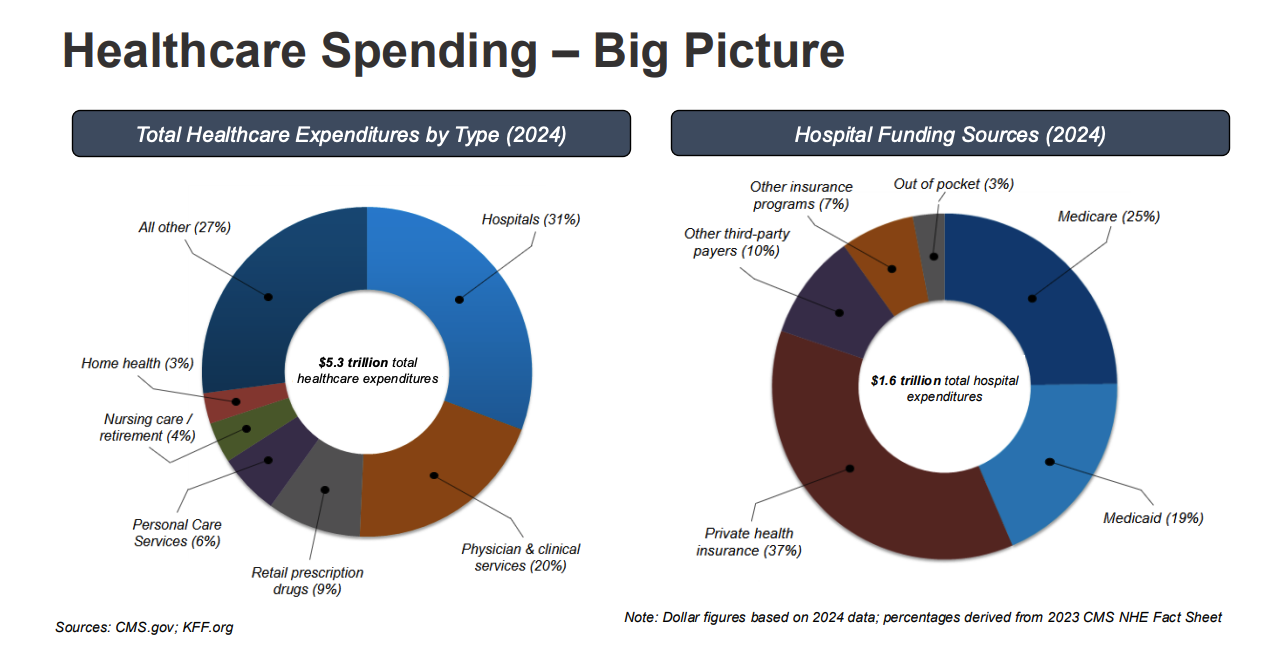

Healthcare spending is approaching 20% of GDP. We're at roughly $5.3T in total national health expenditures, and hospitals account for about $1.6T. The rate of increase flattened briefly post ACA (remember when the goal was to "bend the cost curve"?), spiked during COVID, came back down, and is now climbing again. |

Herd's framing here was straightforward: healthcare affordability is going to become a defining political issue. If not this cycle, then the next presidential election. When you combine healthcare costs with housing, food, and energy, those are the four big affordability rocks that drive voter behavior. Congress will respond at some point, and hospitals are going to be in the crosshairs. |

On hospital funding, the composition matters more than the total. Medicare and Medicaid together account for about 44% of hospital revenue. Private health insurance covers roughly 37%. And that 37% is where hospitals actually make their margin. |

Payor Mix Deterioration and the MA Problem |

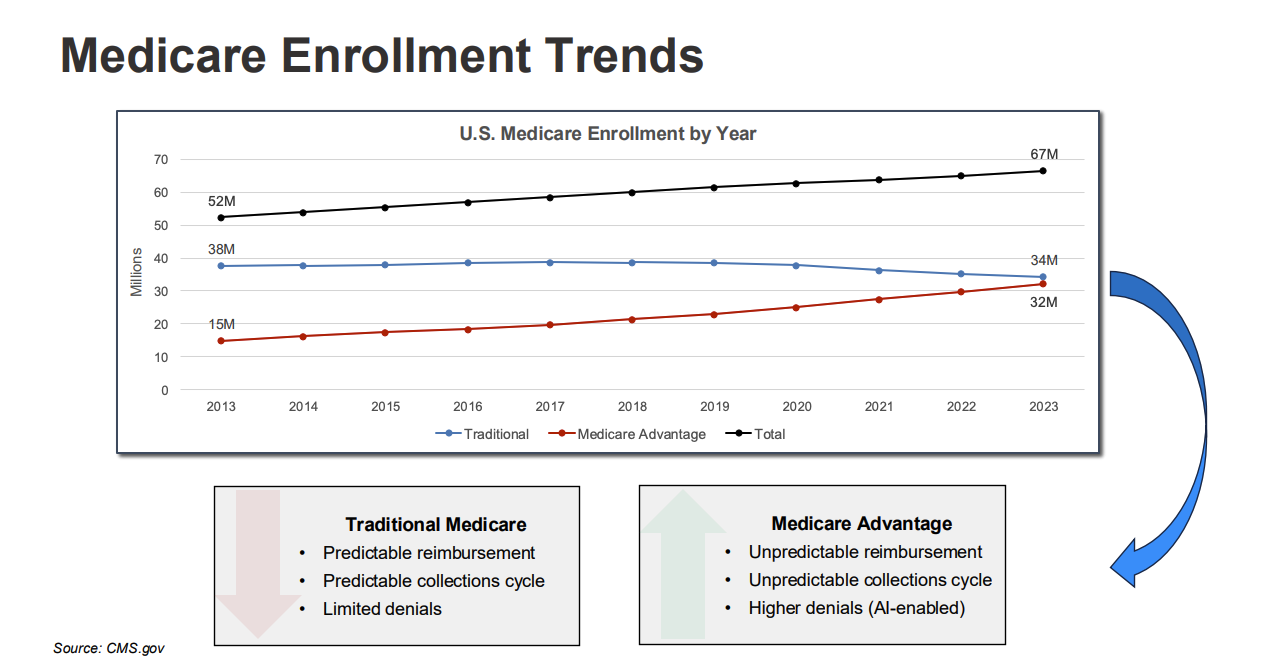

About 10,000 people age into Medicare every day. Total Medicare enrollment went from 52M in 2013 to 67M in 2023. But here's the part Herd highlighted: all of that growth came from Medicare Advantage. Traditional Medicare enrollment actually declined slightly (38M to 34M), while MA doubled from 15M to 32M. |

This matters enormously for operations. Traditional Medicare was predictable. You billed, they paid, collections were clean, denials were limited. MA operates like commercial managed care with pre auths, denials, and AI enabled claims management. Hospitals typically realize 85 to 90 cents on the Medicare dollar from MA plans, largely because of denial activity.

And the MA insurers themselves are struggling. Government funding was essentially held flat last year (sub 1% increase), which hammered their stocks. When MA plans get squeezed, they squeeze providers harder. More denials. More pre auth friction. More downward pressure on what hospitals actually collect.

Layer on the Medicare trust fund dynamics (the latest trustee report projected the hospital services trust fund runs out in about seven years, three years earlier than prior estimates), and the government's role only grows from here. As the Medicare population expands, the government has more leverage and more incentive to push site neutrality, tighten reimbursement, and explore prior authorization in traditional Medicare (which CMS is already piloting in a handful of states as of January).

I also flagged for the group that D SNP plans are now driving the lion's share of MA enrollment growth. Something like 800K of 1M in total MA growth was attributable to D SNPs. |

ASC Expansion and Site of Service Shifts |

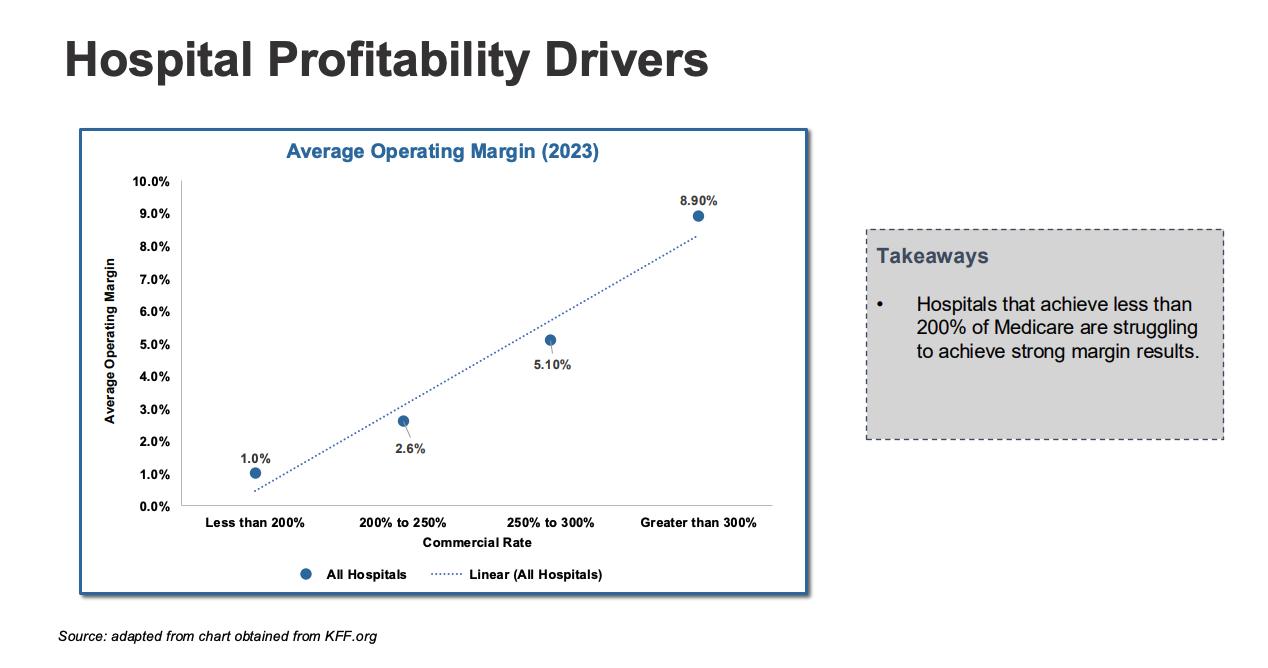

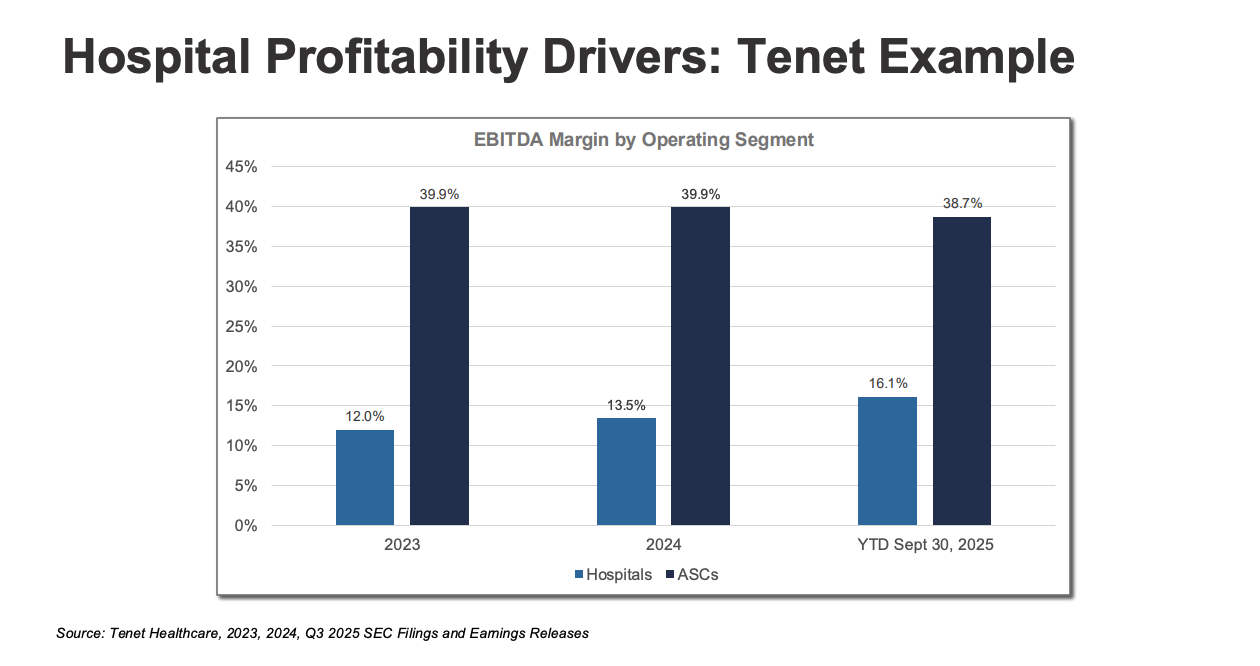

One of the meatiest parts of the discussion. Herd walked through what he called the "perfect storm" driving volume out of hospitals and into ASCs. Payors like ASCs because they're roughly 40% cheaper. Technology allows higher acuity procedures in outpatient settings. Patients prefer the convenience. And CMS added 547 new procedures to the ASC Covered Procedure List in 2026 alone. Advisory Board data projects outpatient volume growth of 10% over the next four years and nearly 19% over the next decade, while inpatient volume stays essentially flat. On a net basis, over 1,000 new Medicare certified ASCs were added between 2019 and 2024 (roughly 7,500 to 8,500). The major platforms are all scaling aggressively: USPI at ~530, SCA Health at ~320, AMSURG at ~250, HCA at ~125, Surgery Partners at ~150. Some estimates suggest up to $50B in hospital volumes could migrate to freestanding platforms. Herd and Kyle's point was that the systems doing well financially all have well thought out ambulatory strategies. They're keeping margin within the system by investing in ASCs, freestanding EDs, and urgent care. The ones struggling haven't built those capabilities and are watching volume walk out the door. Kyle added important nuance on regulation. In non CON states like Texas, you want to build an ASC, go build one. Capital markets sort out whether it succeeds. In traditional CON states, the hospital lobby still exercises significant influence. The pace of ASC expansion varies enormously by geography. Tenet is the public company case study. Their USPI segment runs roughly 39% EBITDA margins versus 12 to 16% on the hospital side. The strategic logic of pivoting toward ambulatory is pretty hard to argue with when the margin differential is that stark. |

I asked the group where inpatient growth is still insulated. Herd pointed to the "sicker, younger generation" phenomenon. Colorectal cancer rates in patients aged 20 to 49 grew 3.2% annually from 1998 to 2019. Stroke prevalence in adults 18 to 44 increased 14.6% from 2011 to 2022. Obesity in the same age group climbed 25%. The traditional utilization bell curve is flattening. Inpatient demand for complex, high acuity cases isn't going away. You can't do brain surgery in an ASC. Yet. |

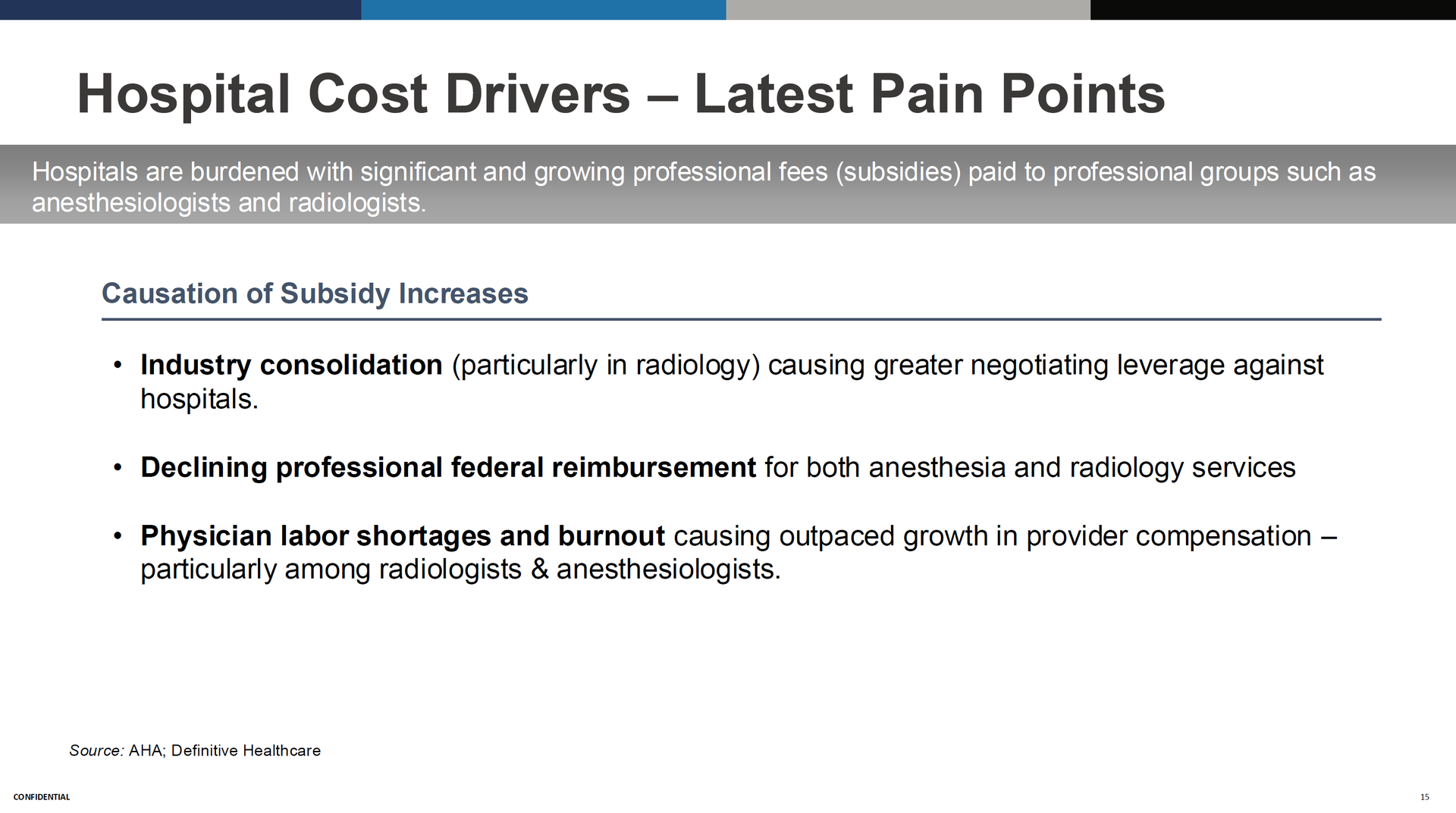

A Physician Subsidy Crisis |

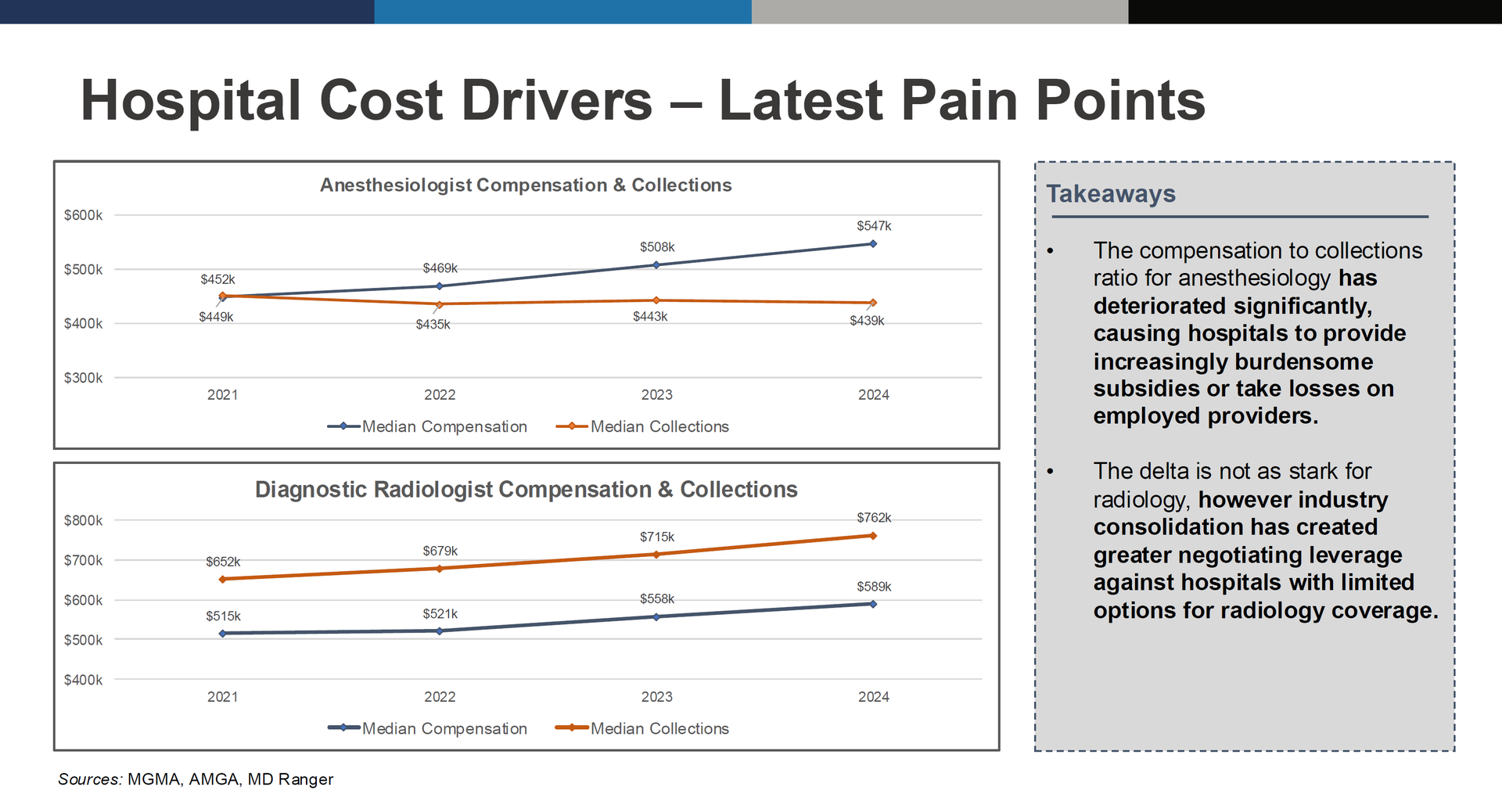

This generated some of the most spirited conversation. Herd walked through MGMA and AMGA data showing a widening gap between physician compensation and collections, particularly in anesthesiology, radiology, and hospital medicine. Anesthesiology data is the most dramatic. In 2021, median compensation and median collections were roughly even (both around $450K). By 2024, compensation climbed to $547K while collections dropped to $439K. That gap is showing up as hospitals writing increasingly large subsidy checks to keep their anesthesia groups in the building. |

There are a few different drivers of professional fees inflation: industry consolidation (especially radiology) giving groups more negotiating leverage against hospitals, declining Medicare professional reimbursement, and physician labor shortages pushing up compensation. Kyle noted it takes roughly 2.2 new physicians to replace the productivity of a single retiring veteran, which compounds the workforce pressure.

Hospitalists show a similar pattern. The compensation to collections ratio went from 136% in 2021 to 143% in 2024. Every percentage point of that gap is dollars the hospital absorbs. You can see pretty readily the growing chasm in comp / collections ratios among radiologists and anesthesiologists: |

I flagged CHS and Ardent as two public companies worth watching on the subsidy front. Both are dealing with double digit inflation in professional subsidies, and it's a meaningful margin drag.

Kyle raised an interesting cultural dimension. The conversations around leverage models (CRNAs in anesthesia, APPs more broadly) are contentious. He described visiting a hospital still on paper records running an anesthesia only model, and the group basically pounced on the guy. Those operators exist. But the economics are going to force the conversation whether leadership wants to have it or not. |

Herd framed the dynamic well: providers are using AI to optimize coding, documentation, and collections, while payors are using AI to optimize denials, down coding, and claims management. Bot wars.

Kyle broke down AI adoption into three cohorts: patient engagement, clinical (ambient documentation, CDI), and rev cycle. On the clinical side, the ambient listening tools (Abridge, Nuance, etc.) are the most mature. They genuinely improve provider quality of life by reducing documentation burden.

But here's where it gets spicy. I brought up that payors have started publishing studies calling out hospitals known to have adopted ambient documentation and CDI tools, comparing billing rates and acuity levels before and after adoption. The payor argument is upcoding. The provider argument is that the tools simply capture clinical acuity that was always there but never properly documented.

Kyle pushed back on the upcoding narrative, and I think he's directionally right. We've been talking about improved clinical documentation for decades. The difference now is the tools actually work. But the payor side isn't going to concede easily, and their denial engines are only getting more sophisticated.

Aaron, one of our community members, raised a critical point about EHR integration being the real bottleneck. You can have an incredible AI tool, but if it doesn't bolt into Epic cleanly, it's useless. And Epic has been accelerating its own AI capabilities, which creates an interesting competitive dynamic. Epic could fast track past a lot of point solutions simply because it's already integrated. I saw a demo from Athena a few weeks ago at a conference in Florida, and their AI module was genuinely impressive. Click a button, toggle into AI mode, interact with a summarized medical record, toggle back to the data. We're getting there.

Kyle also noted that hospital boards (including multi billion dollar systems) are telling their C suites to just go spend money on AI. The pressure to do something is enormous. The best operators are trying to balance urgency with good stewardship. Fail fast makes sense in theory, but bolting things into an EHR is not exactly a quick experiment. |

OBBBA, Coverage Losses, and the Uninsured Trajectory |

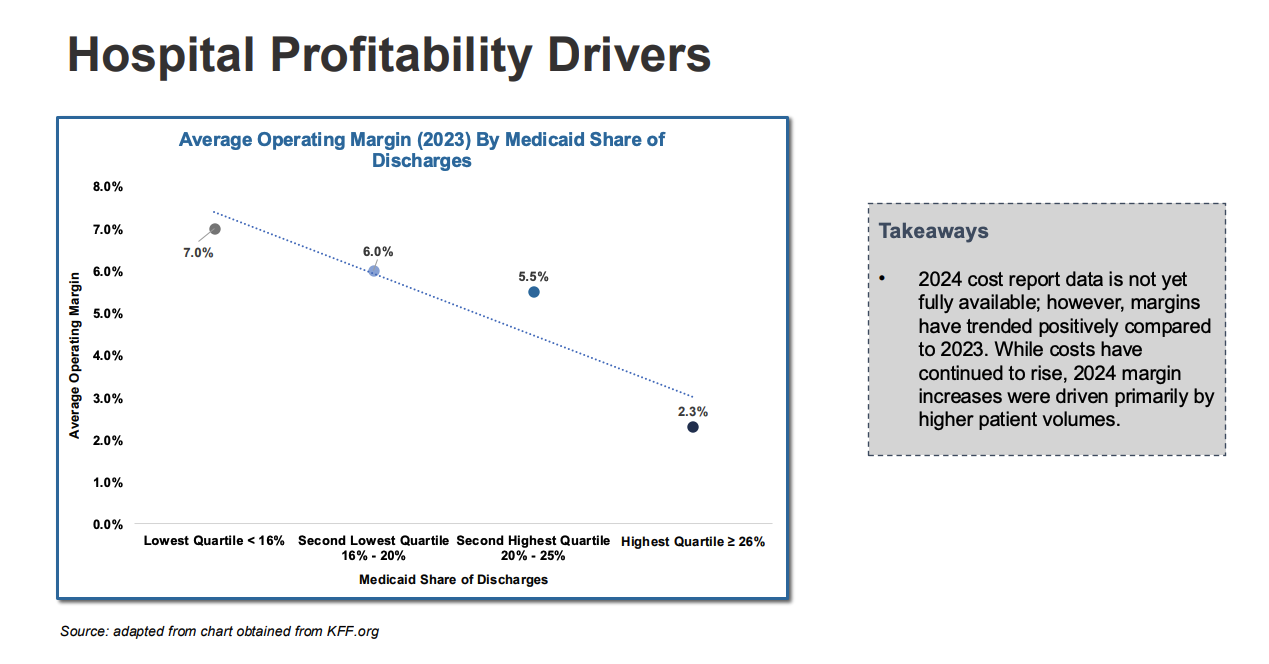

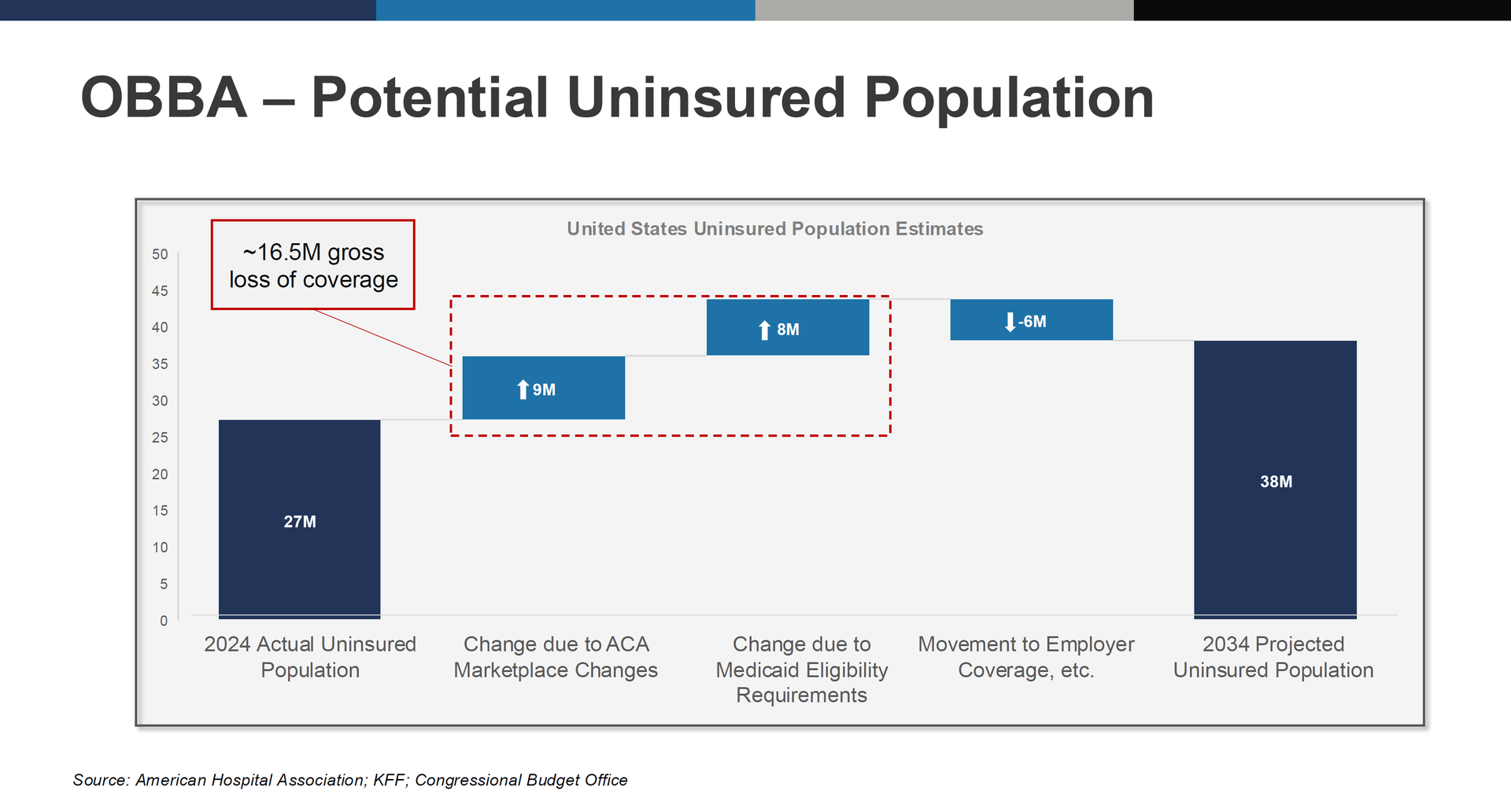

The One Big Beautiful Bill introduced several changes that could meaningfully shift hospital payor mix over the next decade. Shortened ACA enrollment windows. Tightened Medicaid eligibility verification and annual recertification requirements. Expiration of enhanced premium tax credits for exchange plans. CBO and KFF estimates suggest roughly 9M could lose ACA marketplace coverage, another 8M could lose Medicaid eligibility, for a gross coverage loss of about 16.5M. Some of those people move into employer coverage (estimated 6M offset), but the net effect is the uninsured population potentially growing from 27M today to 38M by 2034. For operators, the math is simple: more uninsured patients means more charity care and bad debt. The Medicaid changes hit safety net hospitals hardest. Herd's presentation data showed a clear inverse relationship between Medicaid share and operating margin. Hospitals in the lowest Medicaid quartile (under 16% of discharges) averaged 7% operating margin. Highest quartile (26%+) averaged 2.3%. Herd also flagged the OBBBA's cap on state directed payments, which currently allow states to require managed Medicaid plans to pay enhanced rates (typically 110 to 120% of Medicare). Post OBBBA, those payments get capped at 100% of Medicare starting around 2028. For hospitals in states that have been aggressive with SDPs, that's a real revenue hit. |

Kyle raised the affordability dimension too. As healthcare costs grow relative to GDP, some younger, healthier people are going to opt out of coverage entirely. I'm healthy until I'm not. I'm not paying $1,000 a month for a premium. That dynamic doesn't bode well for risk pools or public health broadly. |

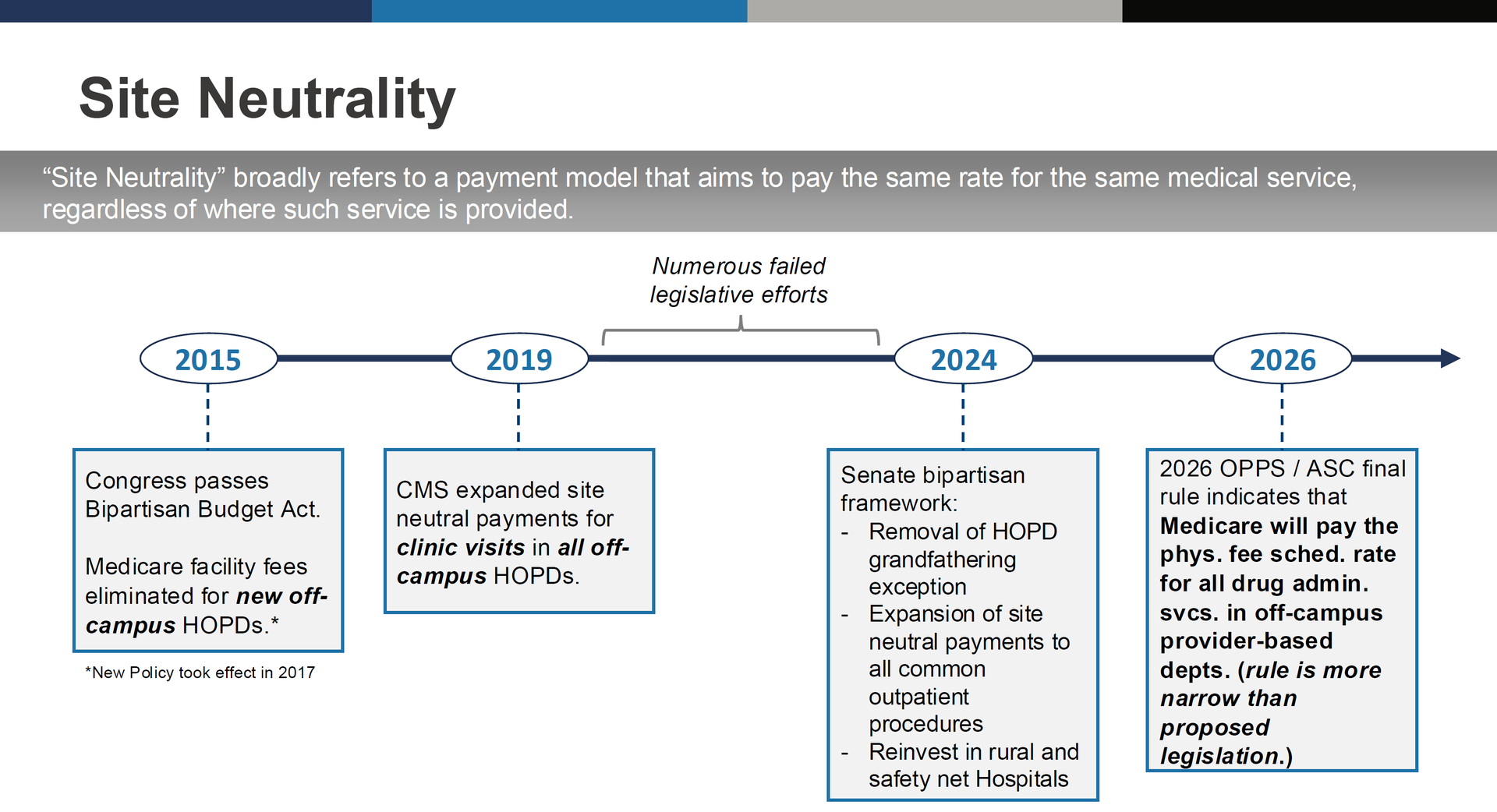

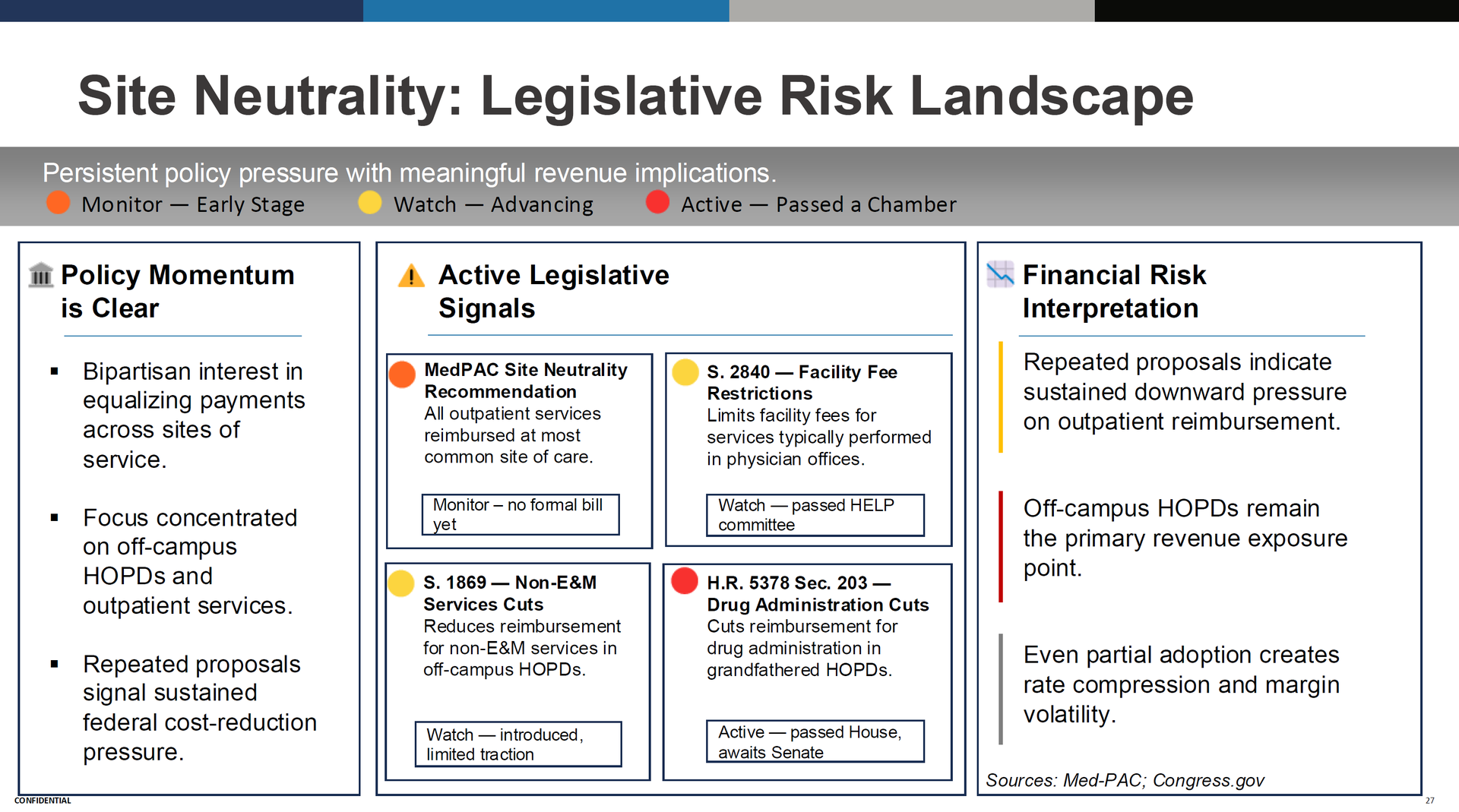

Site Neutrality and Price Transparency |

Site neutrality keeps inching forward. The 2026 OPPS final rule applied site neutral pricing to drug administration services in off campus provider based departments. S. 2840 (facility fee restrictions) passed the HELP committee. H.R. 5378 Section 203 (drug administration cuts) passed the House. MedPAC continues to recommend broader reforms. The direction of travel is clear even if the pace is slow. |

On price transparency, Kyle made a point I think is exactly right: the data is not being used by consumers. Nobody is shopping for heart surgery based on a transparency file. But it is being used strategically in managed care negotiations. JTaylor uses price transparency data daily to help clients benchmark their commercial rates and negotiate contracts. Herd expects the data to improve over time and eventually create market level rate convergence, but we're probably five to ten years out from that having a direct impact. |

Where Does This Leave Us? |

The traditional hospital margin model (lose money on government payors, make it up on commercial) is getting squeezed from both sides. Government is getting bigger, paying less, and adding friction. Commercial is under pressure from price transparency, site neutrality, and employer affordability concerns.

Herd's view is that the energy goes into innovation. CINs. Direct to employer contracting. Ambulatory platform expansion. AI driven efficiency. The technology exists now to solve problems that have been talked about for 25 years. Kyle mentioned Mark Cuban's pharmacy disruption as an example of the kind of model breaking that's possible. I know for a fact Cuban has been working behind the scenes on regional direct contracting mechanisms and publishing everything contractually. Will it work? No idea. But it's fun to watch someone experiment who just doesn't care about the incumbents. |

Most health systems subsidize primary care. They lose money on it. And they accept that as the cost of doing business. But what if primary care is actually your highest-leverage growth asset — the acquisition channel for lifetime patient value, downstream subspecialty referrals, and higher-margin surgical care? The math: grow your PCP panels 20% through AI-enabled access and the downstream capture economics dwarf the investment. Stop treating primary care as a subsidy or loss leader and start treating it as a strategic asset with an AI layer that scales access without scaling real estate and headcount. See how Tom drives health system ROI. |

|

|

- Read: "Healthcare is at an inflection point and leaders are reflecting on a simple question as they plan for the next few years: is the future of this industry bright or dark?" See what emerges from the collective thinking of 96 healthcare leaders in this Becker's Hospital Review article.

- Breakdown: Organizations struggle with VBC when they don't have the infrastructure to manage financial risk. My article shares how Arbital Health's AI platform provides actuarial-grade insights into contracts, cost trends, and population risk.*

- Roundtable: Join us for the April Hospitalogy Roundtable for Plus Members, Friday, April 24, at 1pm EDT.

*This resource is brought to you by one of my brand partners who help make this newsletter possible! |

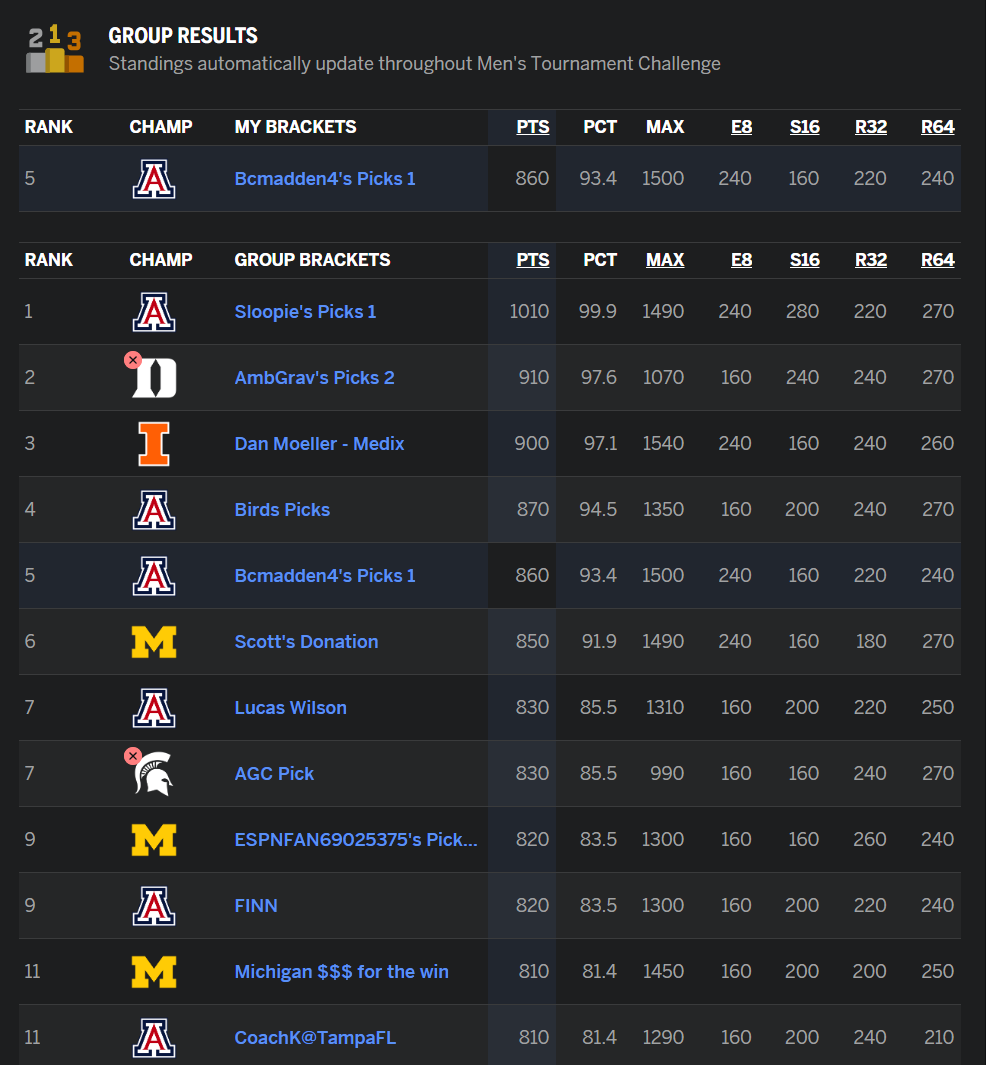

Hospitalogy bracket challenge update now that the final four is set! We have someone in the top 99.9% percentile of all brackets…see guys, I knew you were smart! Shout out to Sloopie, whoever you are you're incredible. But look at this…from the depths of below…a phoenix rises. I am 5th in the Hospitalogy bracket challenge, and in the top 93% tile of all brackets. Currently according to ESPN's prediction, Dan Moeller with Medix is projected to win the challenge IF Illinois takes it home. For me to win, I need UConn and Arizona to make the title game. Let's gooooo. |

|

|

That's all for this Tuesday. I would love to know your thoughts! Just hit reply to this email.

– Blake |

|

|

I'm building a community of leaders in strategy, finance, and ops at hospitals and health systems to help us connect, learn, and grow together. |

|

|

Get your brand in front of 67,700+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|

No comments:

Post a Comment